Feb'24

The IUP Journal of Bank Management

Archives

Financing Options for Rural MSMEs: An Evaluation of Regional Rural Banks

V S Kaveri

Retired Professor, NIBM, Kondwe Khurd, Pune 411048, Maharashtra, India. E-mail: vskaveri@gmail.com

Currently, there are more than 6 lakh micro, small and medium enterprises (MSMEs) in rural India, creating more than 10 crore jobs. These enterprises were the hardest hit during the Covid-19 pandemic, experiencing loss of production, income, and employment generation. But thanks to the relief measures taken by both the Government of India and Reserve Bank of India, and the consequent revival of the economy, they are back on their feet. Since credit is the critical input for stepping up their business activities, it is necessary for them to choose appropriate financial options. Unfortunately, even today, for most of them, predatory moneylenders remain their major financial option. Hence, this calls for strengthening institutional credit to promote and develop rural MSMEs. Among the lending institutions, Regional Rural Banks (RRBs) need a special mention, since they mostly operate in rural areas. But RRBs perceive high credit risk in lending to rural MSMEs and are hesitant to lend liberally. This calls for a detailed study of the financing options available to rural MSMEs and evaluation of RRBs to provide need-based, timely and hassle-free credit. In this backdrop, the paper analyzes issues associated with lending to rural MSMEs by RRBs based on secondary data, and offers suggestions.

Introduction

Regional Rural Banks (RRBs), as part of "Multi-Agency Approach in Rural Areas in India", came into being in 1975 as recommended by the Working Group set up by the Reserve Bank of India (RBI), to promote financial inclusion and meet the credit needs of small and marginal farmers, agricultural laborers, artisans and weaker sections of the society.1 Further, these banks are expected to create an alternative channel to cooperative credit structure with a view to ensuring sufficient institutional credit in rural areas. These are regulated and supervised by the National Bank for Agriculture and Rural Development (NABARD) under the RRB Act, 1976. These banks are envisaged to be State-sponsored, regionally-based, rural-oriented and an integral segment of the Indian banking system. Further, they mobilize resources and deploy the same locally. RRBs are jointly owned by Government of India, state governments and sponsoring Scheduled Commercial Banks (SCBs) with equity contribution in the ratio of 50:15:35, respectively. Over the years, the number of RRBs went up to reach 196 in 2004-05. But, thereafter, the process of amalgamation was initiated as part of revival of ailing RRBs. Consequently, as per the publication of Department of Financial Services (DFS), Ministry of Finance, Government of India (GOI), in 2022-23, the number of RRBs had come down to 43 with 21,892 branches, 29.7 crore deposit accounts and 2.7 crore loan accounts. Though the number of branches of RRBs form just 14% of the total number of branches in the banking system in the country, they account for 30% of the total number of rural branches. In fact, 92% of branches of RRBs are located in rural areas, and many of them are in far remote areas. Further, the share of current account and savings account deposits of their total deposits is as high as 54.5%, when the same for public sector banks, private sector banks and small finance banks remains at 43.8%, 47.5% and 40.5%, respectively. In rural areas, the share of deposit accounts of RRBs is about 26% of total deposit accounts. Regarding lending activities, as stated earlier, 90% of their total loans are provided to priority sector. Within this sector, agriculture and micro, small and medium enterprises (MSMEs) have been the main sub-sectors. Among MSMEs, microenterprises (MEs) operate mainly in rural areas and, therefore, the same are called rural MSMEs. More importantly, as against the overall rural credit-deposit (CD) ratio of 64% for all the banks in the banking system, the same is as high as 75% for RRBs. Therefore, for RRBs, these MSMEs are the major customers in rural areas, next only to farmers.2

Rural MSMEs suffered a lot during the pandemic when Indian economy was in a bad shape, experiencing a steep decline in production, income, and employment. Fortunately, post pandemic, as per the publication of RBI, Indian economy has been marching ahead in maintaining higher and increasing level of GDP of around 7%.3 To avail the benefits of the revival of Indian economy post pandemic, both GOI and NABARD took several measures to make RRBs financially stronger, enabling them to lend more to agriculture and rural MSMEs.4 The measures included: (i) In 2022-23, huge capital worth of 10,890 cr was infused into RRB to meet the regulatory requirement of 9% capital to risk-weighted assets ratio (CRAR), promote financial inclusion among rural community and assist in credit expansion, business diversification, non-performing assets (NPAs) reduction, cost rationalization, technology adoption, improvement in corporate governance and meeting the recent hike in the pension liability; (ii) In order to facilitate comprehensive monitoring of the performance of RRBs, including performance under their viability plans, DFS, GOI, in association with NABARD, developed a dashboard, called 'RRB-Darpan'; (iii) Those RRBs fulfilling certain indicative criteria have been permitted to approach the capital market for raising resources after approval of all concerned regulators and GOI;5 (iv) Keeping in view the growing need to promote digital banking in rural areas, RBI has relaxed certain criteria for these banks to be eligible to provide Internet banking.6 But given the increasing demand for diverse financial instruments from rural communities, it is necessary for RRBs to collaborate with the fintechs, advisory players, input/offtake players, etc. There is also a need to embark on enabling digital tools ecosystem within built capabilities (like learning management systems, input pricing catalog and equipment rental schemes, climate and government alerts, storage availability, mandi price technologies, etc.), and expand the reach of product offering and service delivery to the last mile; (v) During 2021-22, the GOI constituted three committees for: (a) recruitment, promotion, and outsourcing in RRBs, and appointment of chairpersons and officers of the sponsor banks on deputation to RRBs, (b) bifurcation of assets and liabilities of merging and merged RRBs, and (c) revision in risk weights of RRBs and the determination of the pros and cons of bringing stronger RRBs under Basel III norms; (vi) NABARD provides continuous guidance and technical assistance to the ailing banks under 'RRBs in Focus' program, provided at least one of the three criteria, namely, CRAR of less than 10%, gross NPAs of more than 10%, or negative return on assets for the last two consecutive years, is satisfied; (vii) RRBs have been advised to prepare the board approved Viability Plan with SMART (specific, measurable, achievable, relevant and time-bound) indicators. In this regard, a workshop was organized by RBI in 2021-22 wherein the metrics were finalized and adopted under the Viability Plan, besides guiding RRBs on preparation of the Viability Plan.7 Lastly, for the long-term sustainability of RRBs, efforts have been put in by NABARD for effective risk management practices in banks through policy directions, training, handholding and exposure visits for improving systems and processes.

Despite the above developmental measures, RRBs are yet to step up their CD ratio and improve the loan asset quality when the level of gross NPAs is high and increasing. More importantly, rural MSMEs are still not able to receive adequate, timely and hassle-free credit from RRBs. In this backdrop, the paper attempts to understand the financing options for rural MSMEs by evaluating the performance of RRBs based on the analysis of the secondary data. The next section deals with financing options for rural MSMEs, followed by a discussion on rural MSME financing by RRBs. Subsequently, performance review of rural MSME financing is assessed, and lastly, the paper offers policy recommendations and conclusion.

Financing Options for Rural MSMEs

As per the GOI notification of June 26, 2020, ME being part of the MSME sector, is defined as "an enterprise where investment in plant and machinery or equipment does not exceed one crore rupees and, turnover is not more than five crores rupees." With this definition, the government has done away with the difference between manufacturing and services as in the past.8 As per the GOI publication, there were as many as 634 lakh unincorporated and non-agriculture rural MSMEs in the country, which accounted for more than 99% of total enterprises in the MSME sector. More importantly, while MSME sector created as many as 11.10 crore jobs, MEs alone provided employment to 10.77 crore unemployed youth, i.e., 97% of total employment was generated by MEs.9 Rural MSMEs are known for assisting in industrialization of rural and backward areas for reducing regional imbalances, and 96% of them are in the unorganized sector, and they are run by a single person. Further, two-thirds of rural MSMEs are owned by the socially-backward groups, which needs a special mention. Lastly, they produce a large number of products which are the raw materials for small and medium enterprises. In view of their increasing importance in the economy, they deserve adequate, timely and hassle-free institutional credit.

There are two financing options for rural MSMEs: (i) internal financing option; and (ii) external financing option. Regarding internal financing option, each enterprise is expected to bring in minimum capital when operations start and maintain minimum equity comprising capital, reserves and surplus. In case of new entrepreneurs, particularly technically qualified entrepreneurs, it may become difficult to bring in minimum capital and, therefore, they shall receive equity support from National Equity Fund, specially set up by GOI for MSMEs. Internal sources of funds, mainly equity, are supplemented by external sources of funds, which include non-institutional borrowings and institutional borrowings. Among non-institutional lenders, money lenders are more active in financing rural MSMEs. The last census of MSMEs was conducted in 2015-16, which found that about 95% of the MEs had no access to institutional finance. Even today, money lenders play an important role in rural areas in meeting short-term credit.10 Generally, those rural MSMEs which are not in a position to meet the requirements of lending institutions, approach money lenders. Such requirements of the lending institutions include audited financial statements, minimum capital, collaterals, etc. In this regard, there is a dire need to promote financial inclusion, which aims at bringing in such rural entrepreneurs under the fold of institutional lenders, which include scheduled commercial banks (SCBs), public sector banks (PSBs), private sector banks (Pvt Bks), and small finance banks (SFBs), state finance corporations (SFCs), cooperative banks, Small Industries Development Bank of India (SIDBI), NABARD, microfinance institutions (MFIs), and lastly RRBs. This paper is confined to the role played by RRBs in financing rural MSMEs.

RRBs provide credit to the rural MSMEs in the form of direct credit, which is provided after appraisal of the project proposal and acceptance of the entrepreneur on the one hand and fulfillment of terms and conditions, on the other. Direct credit of RRBs includes fund-based credit (term loan for purchase of fixed assets and working capital finance for meeting operating cost) and non-fund-based credit provided in the form of guarantee and letter of credit. Generally, RRBs provide a composite loan to the newly set up rural MSMEs, which covers requirements of both working capital credit and term credit. In case of indirect credit, there are intermediaries between the lending institution and the entrepreneur. These intermediaries include: self-help groups (SHGs), non-banking finance companies (NBFCs), non-government organizations (NGOs), microfinance institutions (MFIs), etc. Further, refinance is provided by Small Industries Development Bank of India (SIDBI) and NABARD to banks for credit extended to rural MSMEs. In addition, subsidy and equity support are also provided by the government under various schemes. Lastly, to encourage lending institutions to lend more, RBI considers credit to MSMEs as part of the priority sector lending. Since RRBs operate mainly in rural areas, this calls for a detailed discussion on the role played by RRBs in financing rural MSMEs.

Rural MSME Financing by RRBs

Direct Credit by RRBs to Rural MSMEs

Fund-Based Facilities

Regular overdraft facility: RRBs allow regular overdraft facility on the current account of rural MSMEs against the security of stock (raw materials, stock in process, finished stock, book debt, etc.) for meeting their working capital requirements on a regular basis. The period of overdraft is one year, which is expected to be renewed every year after the review of the conduct of the overdraft account and satisfactory performance of the enterprise. Usually, a margin of 25-50% is stipulated depending upon the purpose and nature of security.

Temporary overdraft: In case of emergency, RRBs also allow temporary overdraft (TOD). This is given for a short period, say, one week, and carries a slightly higher rate of interest.

Open cash credit (OCC): This is similar to regular overdraft credit facility for meeting the working capital requirements. In case of overdraft facility, it is essential for rural MSMEs to open a current account first. But this requirement is not necessary in case of OCC, which is sanctioned against the stock and book debt on a regular basis. Usually, a margin of 25-30% is insisted on the value of stock and book debt, and these two together form chargeable current assets (CCAs). Taking into account the value of CCAs, drawing power (CCA - Margin money) is calculated. The borrower can operate the OCC account within the sanctioned limit or permitted drawing power, which is the most popular type of finance for rural MSMEs. For reviewing the OCC limit, actual and projected financial statements are needed to assess financial strength and working capital requirements.

Term loan: RRBs allow medium-term loan (3-5 years) and long-term loan (more than 5 years) for acquiring fixed assets such as plant and machinery, implements, house property, furniture and fixture, etc. These loans are repayable in suitable installments based on the future income generated by the rural MSMEs during the loan period. Interest is charged on the balance outstanding after the installments are remitted, which is called 'diminishing balance' method. Fixed assets purchased out of the term loan are mortgaged in favor of the bank. Usually, a margin of 15-25% of the value of assets is insisted upon the borrower. The loan amount should be less than the asset value which is restricted to 75% of the value of the asset.

Bills or cheques purchased/discounted: This facility is extended by RRBs as post-sale finance. Generally, rural MSMEs make most of their sale on credit basis and allow credit of normally a period of 15-60 days. Till such time, their money is blocked in the business by way of book debts or trade debtors. RRBs finance such borrowers by extending bills/cheques by discounting facility, which is liquidated automatically on the due date.

Others: Rural MSMEs may approach RRBs to meet emergency financial needs. In that case, they can avail loan against fixed deposits with RRBs, if any. Usually, 90% of the current value of deposit is given as loan. On maturity, the loan is adjusted and the balance amount will be paid to the borrower. Banks charge extra interest that is added to the interest rate on fixed deposit against which the loan is raised. Similarly, rural MSMEs shall raise a loan against security of gold ornaments/jewels, if any, to meet emergency financial needs. Generally, a margin of 30% is kept on the market value of jewels. Banks have a standard per gram rate for sanctioning the loan, which is reviewed from time to time depending upon the market conditions.

Non-Fund-Based Facilities

Guarantee: Rural MSMEs shall undertake the supply contract of goods and services. The beneficiary of such facilities may not have full confidence in rural MSMEs and insist on bank guarantee. The beneficiary requests the RRB to furnish a guarantee. In such cases, though the bank's funds are not involved currently, this may fall back on the same in future upon default by such suppliers. These are termed contingent liabilities. RRBs earn commission by extending such guarantee facilities to rural MSME suppliers of goods and services.

Letter of credit (LC): Rural MSMEs are also engaged in exporting goods and, therefore, RRBs allow credit to the buyer (importer). When the exporter (rural MSME) does not have full confidence in the client (importer), the former may insist on the latter to open LC in his favor. On such occasions, the RRB on behalf of the importer gives an undertaking to the exporter stating that in case the importer fails to pay, it will make the payment to the exporter. All international transactions are executed on LC terms only. Banks earn commission on LCs opened on behalf of their clients. There could be a domestic LC facility also.

Indirect Finance by RRBs to Rural MSMEs

This includes loans provided by RRBs to those persons in the decentralized sector involved in assisting in the supply of inputs and marketing of outputs of rural MSMEs; and loans sanctioned by RRBs to cooperatives of producers in the decentralized sector supplying goods to rural MSMEs.

Loans Offered by RRBs to MFIs for On-Lending to Rural MSMEs

To implement the above credit products, RRBs formulate a Loan Policy which talks about their bank lending philosophy and internal control/risk control. It is a reference point to both the banker and the borrower. This contains: (i) size of credit depending upon lendable resources, stipulated CD ratio and business plan; (ii) direction of credit: allocation of lendable resources to various sectors to spread risk, risk and return combination, flexibility in approach but within the tolerance limit, geographical coverage, etc.; (iii) composition of credit: funded and non-funded and their composition; (iv) quality of credit: rating of borrowers, asset classification (standard, substandard, doubtful and loss); and (v) credit administration: procedures for managing loan portfolio which covers appraisal, pricing, lending powers, maximum maturity of loans, reporting system, documentation, disbursement, supervision, monitoring, recovery, internal control and loan review. All lending activities should be carried out as per the Loan Policy. In addition, in terms of RBI Circular on Lenders' Liability, December 9, 2002, RRBs are expected to observe sound lending practices with special reference to rural MSMEs. The major sound lending practices include: (i) loan application form should be simple and in a regional language; (ii) a checklist of data/information requirements should be provided to the borrower while giving the loan application form. Further, bank's terms and conditions including rate of interest and bank charges should be explained while sanctioning the loan; (iii) time limit for loan sanction should be informed to the borrower who can plan his funds management accordingly; (iv) receipt should be issued upon the submission of the loan application form by the borrower; (v) letter of sanction should be comprehensive and the borrower's suggestions regarding terms and conditions, if any, shall be incorporated; (vi) reason for rejection of loan application should be indicated; (vii) pre-sanction inspection should be done and, interviewing a borrower is must to defend his case; (viii) joint appraisal is called for in case of multiple lending institutions being involved in financing the rural MSMEs; (ix) documents should be simple; (x) promoter's contribution should be deposited before disbursement; (x) post-disbursement inspection is a must within a month from the date of loan disbursement; (xii) in case of genuine financial difficulties, ad hoc credit sanction shall be offered; (xiii) in case of genuine financial difficulties, loan compromise is preferred to legal action; and (xiv) legal action should be initiated if the borrower is a willful defaulter.

Performance Review of Rural MSME Financing by RRBs

Keeping in mind the unique features of RRBs and the recent initiatives of GOI and NABARD, it is attempted to review the performance of these banks by carrying out financial analysis for two years, 2020-21 and 2021-22, on the one hand and a comparative study of RRBs with rural financial institutions (RFIs) and Indian banking sector (IBS), on the other.

Financial Analysis

It is attempted to assess the performance of RRBs based on the latest data relating to balance sheet and profit performance and financial indicators as furnished in the Annual Report, Department of Financial Services, Ministry of Finance, GOI, for the post-pandemic period covering 2020-21 and 2021-22. Accordingly, the following are the observations:

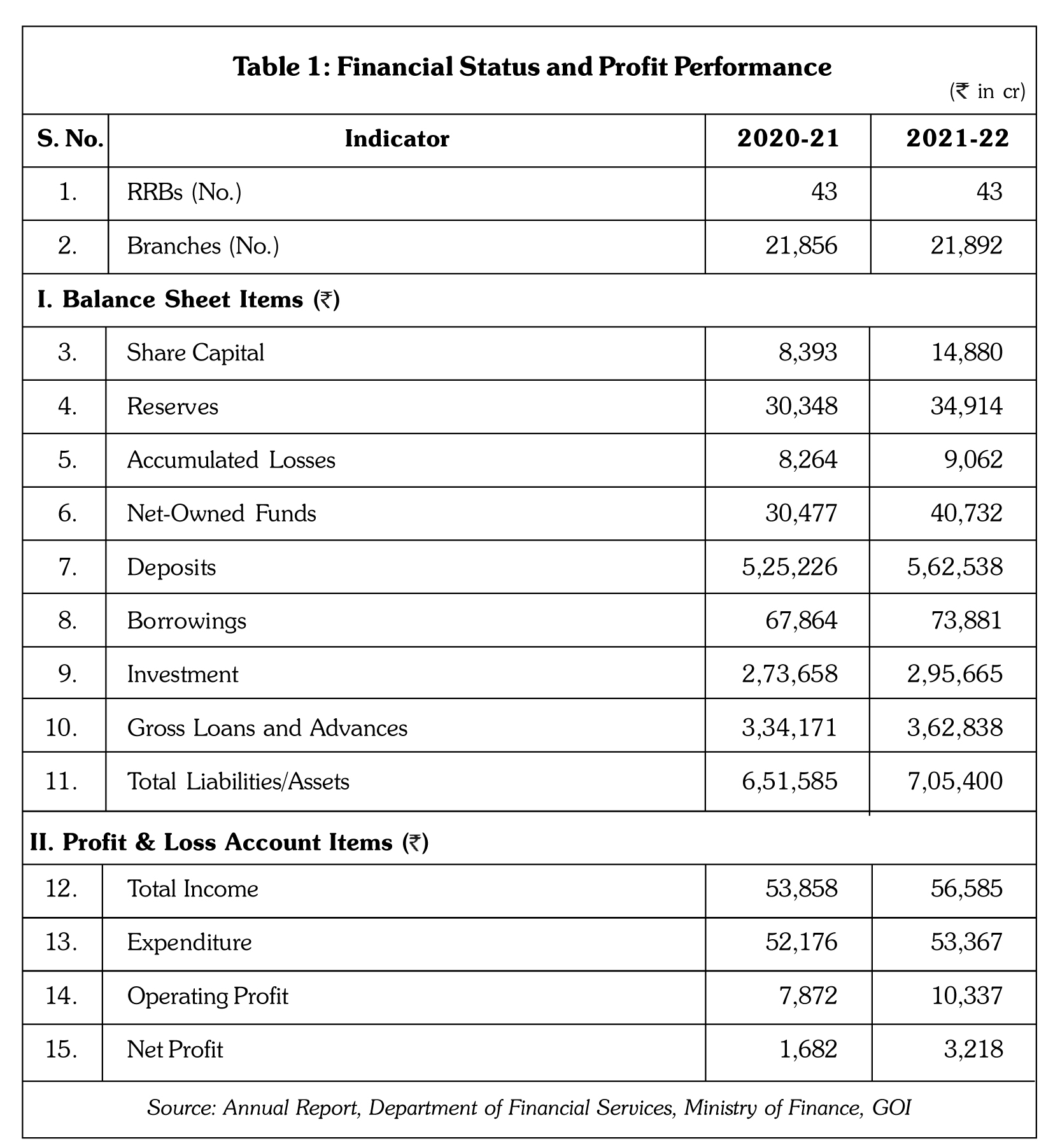

- As per Table 1, due to the amalgamation of RRBs, the number of banks came down to 43 as of March end, 2021. Since RRBs took sufficient time to come out of the adverse impact of Covid-19, they could open just 36 new branches in 2021-22. This, in turn, initiated the process of business expansion.

- In Table 1, changes in the major items of Balance Sheet and Profit & Loss Account in 2021-22 over the previous year are presented. Regarding the size of Balance Sheet (Total Liabilities/Total Assets), the same expanded by 8.2% in 2021-22 over the previous year figures. About the changes in the major items of Balance Sheet, share capital witnessed a steep rise of 77% due to fresh capital infused by as much as 10,890 cr in 2021-22. During the same period, reserves also moved up by 14.9%, and losses increased by 9.6%. Net-owned funds remained at a comfortable level of 40,732 cr in 2021-22 as against 30,477 cr in 2020-21, a rise of 32%. This impressive growth in net-owned funds helped RRBs to expand their business size, raise borrowings and manage risk without much difficulty. Further, deposits, a major source of funds, formed 80% of total liabilities and maintained an increase of 7.10% in 2021-22 over the previous year figures. RRBs continued to borrow, which went up by 9.21% in 2021-22 as against the 2020-21 data, though the amount is much lesser than deposits. On the assets side, investment and gross loans and advances are the two major items which witnessed a rise of 8.0% and 8.6% in 2021-22 over the previous figures, respectively. Regarding Profit & Loss Account, while total income showed a rise of 5.1% in 2021-22 over the previous year figures, total expenditure witnessed just 2.3% growth in the same year. Consequently, in 2021-22, both operating profit and net profit moved upwards and remained at 2,465 cr and 1,536 cr, respectively. But RRBs suffered from lower productivity of resources. In other words, though the Balance Sheet size expanded by 8.2% during the period, total income rose by just 5.1%. Similarly, while banks witnessed an increase of 32% in Net-Owned Funds during the period, they could not lend more since loans and advances moved up by just 8.6%. Thus, RRBs have to step up their lending since they are more comfortable with regard to capital adequacy.

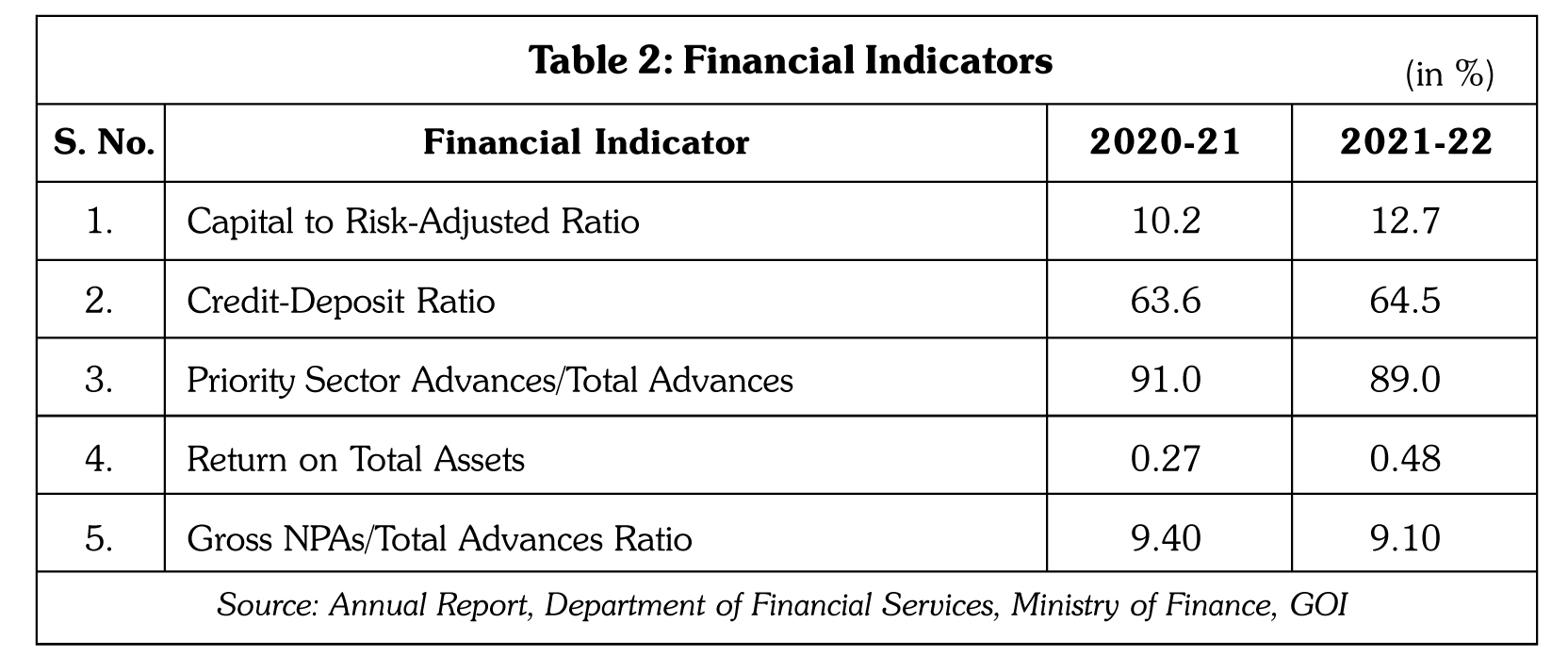

For a better understanding of financial status and profit performance, certain financial indicators need to be looked into, which are stated in Table 2. Due to the substantial infusion of capital in RRBs, CRAR went up from 10.2% in 2020-21 to 12.7% in 2021-22. But RRBs took a longer time for revival of their financial health, though CRAR was as high 12.7. This is evident from the CD ratio, which went up marginally from 63.6% in 2020-21 to 64.5% in 2021-22. Further, these banks experienced an impressive improvement in their profitability position when Return on Total Assets (Net Profit/Total Working Funds) increased from 0.27% in 2020-21 to 0.48% in 2021-22. Lastly, though Gross NPA ratio declined marginally from 9.4% in 2020-21 to 9.1% in 2021-22, its level is very high as compared to other lending institutions, mainly SCBs. To extend analytical exercise further, it would be worthwhile to compare the financial indicators of RRBs with: (1) RFIs, and (2) IBS separately.

Performance Review - RRBs in Comparison with RFIs and IBS

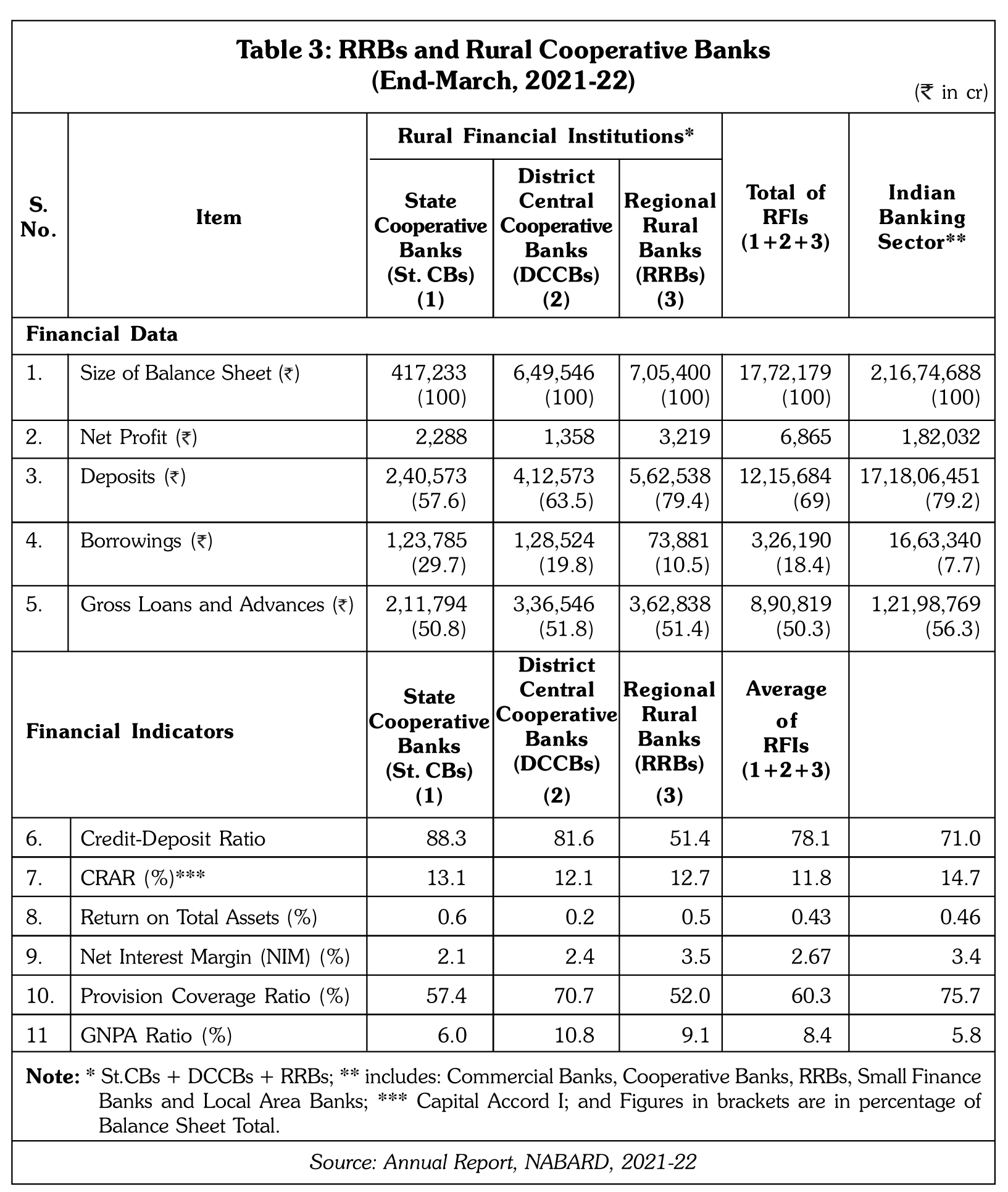

For the assessment of the financial position and operational performance of RRBs in comparison with RFIs and IBS, the publications of NABARD and Department of Financial Services, Ministry of Finance, GOI, for the year 2021-22, were considered.11, 12 RFIs comprise: (i) rural cooperative banks (RCBs), and (ii) RRBs. RCBs are further classified into: (i) state cooperative banks (St.CBs), and (ii) district central cooperative banks (DCCBs). Similarly, IBS consists of all lending institutions including: commercial banks, cooperative banks, RRBs, small finance banks and local area banks. Since RRBs play the role of financial intermediation in agriculture and rural MSMEs, it is appropriate to compare RRBs with RFIs. Similarly, RRBs being part of IBS, it would be relevant to compare the former with the latter. From the data furnished in Table 3, as of end-March 2022, the following observations are made:

- RRBs are larger by size since their share of total resources i.e., total liabilities with total resources of RFIs is 40%. But in the case of IBS, the same is as low as 3.25%. However, the contribution of RRBs in promoting financial inclusion in the country is worth noting because 90% of total advances of RRBs are provided to the priority sector.

- All lending institutions under RFIs group, viz., St.CBs, DCCBs and RRBs, together reported Net Profit of 6,865 cr in 2021-22. Among these, RRBs are better placed in terms of profitability, where their Return on Total Assets of 0.5% was higher than that of 0.43% of the RFIs group. This is due to higher Net Interest Margin (NIM) which remained at 3.5% for RRBs as against 2.67% for RFIs group. But Provision Coverage Ratio (PCR) is lower in respect of RRBs due to more provisions needed against NPAs. When the profitability position of RRBs is compared with that of IBS, the former is marginally better placed than the latter. But PCR of IBS were as high as 75.7% as against the same of RRBs at just 52% due to accumulated losses.

- RRBs are more efficient in deposit mobilization than St.CBs and DCCBs under RFIs group. This is evident from the study of share of deposits in total liabilities of RRBs which was as high as 79% as against 69% for RFIs group. In respect of deposits as percentage of total liabilities of IBS, it is similar to that of RRBs. Further, RRBs borrowed less because they did not lend more. Borrowing as a percentage of total liabilities for RRBs is just 10.5, when the same remained at 18.4 for RFIs group. Regarding the percentage share of deposits to total liabilities of IBS, it is as high as that of RRBs.

- While RRBs are aggressive in deposit mobilization, like other lending institutions in the RFIs group, they are hesitant to lend more when their share of loans and advances in total liabilities remained at just 51.4%. Further, CD ratio of RRBs was as low as 51.4% in 2021-22, while the same for RFIs group and IBS remained at 78.1% and 71.0%, respectively. Due to lower loan asset quality, RRBs could not step up their lending. Hence, gross NPAs as a percentage of gross loans and advances of RRBs was as high 9.1 as against the same of 8.4 for the RFIs group. Ironically, this percentage was as low as 5.8 for IBS, which reconfirms that RRBs did not lend more due to high NPA ratio.

- Relatively speaking, RRBs are more comfortable in terms of capital adequacy in terms of CRAR-Basel I due to huge capital infusion made in 2021-22. Their CRAR stood at 12.7% as against the minimum CRAR of 9.0%. Further, CRAR of RRBs is higher than DCCBs. And, CRAR of the RFI group is 11.8%. But in comparison with CRAR of IBS at 14.7%, the CRAR of RRBs is much lower. Thus, despite higher CRAR, RRBs were found to be slow in lending due to lower loan asset quality.

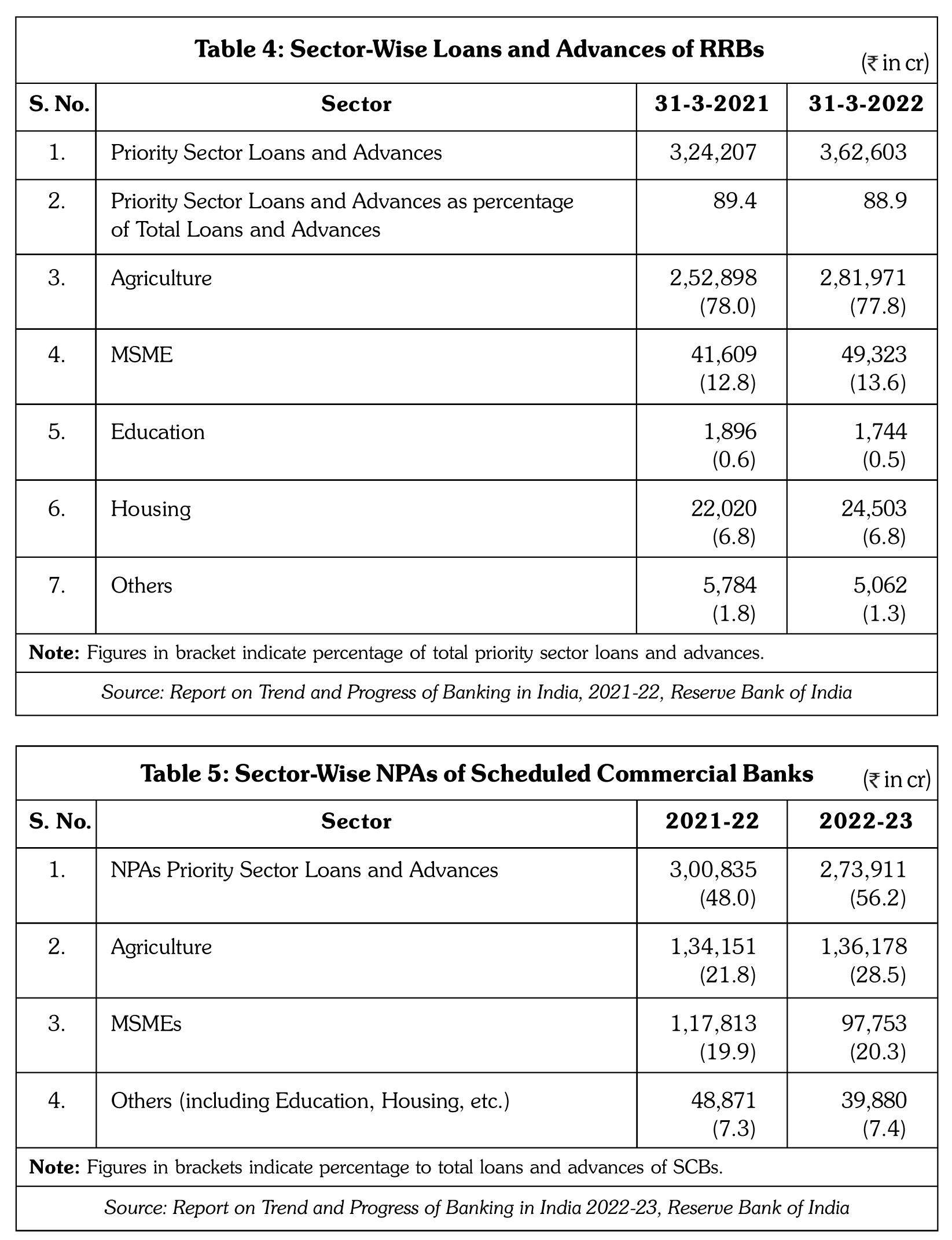

- As seen from Table 4, priority sector loans and advances of RRBs went up from 3,24,207 cr in 2020-21 to 3,62,603 cr in 2021-22, a rise of 11.8%. In these two years, priority sector loans and advances as percentage of total loans and advances of RRBs remained at around 90.

Within the priority sector, the share of loans and advances to agriculture was as high as around 80%. After agriculture sector, RRBs preferred MSME sector and housing sector for lending. Though the data relating to NPAs in agriculture sector of RRBs is not available, some indication is available from the sector-wise NPA data of SCBs, as stated in Table 5. Accordingly, nearly half of the total NPAs of SCBs are in the priority sector. Similarly, NPAs in agriculture sector of the SCBs amount to 41.7% of total NPAs in the priority sector. Next to agriculture, NPAs in the MSME sector as a percentage of total NPAs in the priority sector stood at 20.3 in 2022-23. These observations also hold good in the case of RRBs whose 90% of the total loans and advances are provided to the priority sector. And, the share of loan and advances to agriculture sector in total loans and advances remained as high as 77.5% in 2021-22. In general, agriculture sector often suffers from external factors such as natural calamities, increasing cost of operations, lower minimum support price announced by the government from time to time, shortage of labor, increasing debt burden, etc. Consequently, NPAs in agriculture loans and advances are on the rise. But in respect to MSMEs, next to agriculture, it is relatively possible to step up lending and check growth in NPAs by focusing on internal factors by adopting sound lending practices relating to credit appraisal, monitoring and loan recovery. Towards this end, the present paper confines to MSMEs, mainly rural MSMEs, and offers suggestions to ensure the sound lending practices relating to (i) credit appraisal, (ii) credit monitoring, and (iii) loan recovery.

Recommendations

Credit Appraisal

It is important that credit appraisal should aim at ensuring a need-based credit to small enterprises, for which officers in RRBs have to develop a fair understanding of the borrower's business activities, not only financial aspects but also technical and commercial aspects. For this purpose, they should be in touch with changes in the market to ascertain the performance of comparable units in the local and nearby areas and their impact on holding of the level of current assets, terms of trade, capacity utilization and profit performance. Further, officers' credit appraisal skills have to be upgraded to assess viability of the project and credibility of the borrower. In this regard, efforts should be put in to collect more qualitative information for credit appraisal, besides holding a discussion with the borrower in detail by developing a checklist of questions to be asked in the very first meeting with the same. Adequate weightage should be assigned to assessment of the 'person behind the show', for which branches have to collect information from various sources. In the case of loans to be sanctioned at head office level, the role of the branch and the head office in processing of the credit proposal should be clearly spelt out. In the same way, borrowers are also suggested to take up certain initiatives to ensure need-based finance. To elaborate, it is observed that in the absence of the required statements/information from the borrowers, banks have no option except to adopt a conservative approach in credit sanction. Hence, it is expected that projections made by the borrowers should be in line with the past trend and logically convincing. In genuine cases, banks shall allow some deviation, provided the reasons given by the borrowers in preparing the projected statements are acceptable. In addition, there should be sufficient transparency in the presentation of financial statements by them. This would help the banks to assess the need-based finance. Above all, the borrowers have to satisfy the RRBs in regard to their plan to seek bank finance to meet the genuine credit needs of working capital and investment in fixed assets.

In a competitive environment, it is also important to reduce the time involved in credit sanction. In this regard, banks are advised to explain their data/information requirements to the borrowers right at the time of issuing a loan application form. Similarly, it is essential for the borrowers to submit all the required information to the bank in one installment and not piecemeal. Further, banks need to complete their appraisal in one sitting so that the borrower need not be called for discussion time and again. And, coordination between the RRB and the other local lending institutions should also be ensured in such a way that there is joint appraisal and reasonable division of work. In addition, it is often observed that even viable projects sanctioned by banks are set aside for disbursement because of the inability of the promoter to bring in his contribution in the form of equity. As the time gap between the date of loan application and the date of sanction increases, many developments may take place at the promoter's end, whereby he may invest his savings elsewhere. It often happens that banks do not get information about deposits/loans received from friends and relatives which may be a source of the promoter's contribution. Finally, response to the National Equity Fund, which aims at supplementing the promoter's capital, calls for a wider publicity. Further, it is generally perceived in RRBs that loan to rural MSMEs is more risky since it does not offer adequate collaterals. This calls for a change in the mindset of officers in RRBs and they should understand that the loan repayment depends on income generation and not collaterals received. It is also observed that a few borrowers manage to raise multiple loans from different lending institutions against the same asset. Hence, the government has set up Central Registry of Securitization of Assets India (CERSAI) for immoveable assets. Similarly, movable assets such as stock of goods form the main type of security that shall be hypothecated/pledged to obtain working capital finance. CERSAI, in coordination with the government and RBI, has also created the movable asset registry. Further, appreciating the difficulties of rural MSMEs, RBI has asked the banks not to insist on collaterals in case of loans up to 1 cr. Also, Credit Guarantee Fund Trust for Micro and Small Enterprises (CGTMSE) has been set up to encourage the banks to extend credit based on the viability of the proposal rather than insisting on security or surety. Recently, the guarantee cover for MSMEs has been extended to 2 cr.13 And, small enterprises should also be told about the security requirements of the bank, if any, right in the first meeting with them so that they may get sufficient time to arrange collaterals. Lastly, many of the small enterprises do not have the required documents for availing bank credit. These include: audited financial statements, project proposal, list of creditors, overdue receivables, etc. In the absence of such documents, small entrepreneurs are forced to seek funds from informal sources. Lastly, considering the information requirements of RRBs, the borrowers should create an MIS suitably, for which the entrepreneurs need to be educated on maintenance of books of accounts and periodical statements to be submitted to the bank. Now, with computer facilities, this may not be an uphill task.

Credit Monitoring

In September 2002, RBI suggested a common framework to prevent slippage of loan assets by introducing 'Early Alert System', which is expected to throw certain signals of incipient sickness or irregularities in the conduct of loan account.14 Such signals include: delay in submission of stock statement, return of cheques/bills unpaid, dishonor of guarantee obligation, poor operational performance, diversion of bank funds, nonavailability of the borrower for discussion, disputes among partners, etc. Thereafter, the RRB should assess whether default in payment of loan installments or irregularity in the conduct of cash credit account is due to some inherent weakness, a temporary liquidity or cash flow problem and, accordingly, calibrate its response. Banks have to prepare a list of potential NPAs based on certain signals as stated above. An asset may be transferred to this new category of potential NPAs once the earliest signs of sickness/irregularities are noticed. For preventing action against potential NPAs, certain steps are suggested to branch managers of RRBs which include: (i) identify the potential NPAs when the loan default is for two months, (ii) study the causes to ascertain whether default is due to inherent weaknesses or due to temporary liquidity or cash flow problem and offer contingency help immediately in the form of ad hoc limits if cash flow mismatches are genuine, (iii) ask the borrower to submit the renewal proposal and enhance suitably if limits are found to be inadequate, leading to loan default during the year, (iv) if cheques are drawn on parties not related to business or heavy cash drawal and no corresponding increase in stock, pass cheques for payment after a detailed scrutiny, provided limits are found to be inadequate leading to loan default during the year,

(v) visit the business premise/residence immediately if the stock statement is not submitted and verify the securities, (vi) collect the interest on monthly basis, (vii) visit the factory if the interest or installment is not paid for a long time, (viii) keep the documents updated and handy, (ix) read the local newspaper daily about any adverse developments in the unit, and (x) ascertain the position of accounts with other banks; exchange information about the borrower in the consortium meeting, etc. Among these steps, keeping in touch with rural MSMEs on a regular basis will certainly help to obtain a timely signal of incipient sickness and offer necessary help to take care of temporary cash flow mismatches to arrest the slippage in loan asset quality.

Loan Recovery

RRBs are suggested to make cash recovery by employing timely and effective recovery measures. To start with, a reminder to all borrowers should be sent before the loan installment falls due. The reminder system is the cheapest mode of recovery. Generally, response to the reminder from honest borrowers is encouraging. However, efforts need to be strengthened in sending the reminders to all borrowers in 'standard asset' category on a regular basis. If there is no response to two reminders sent, visits to their business premise or residence have to be organized. And, this system of paying a visit is a more dependable loan recovery measure. During the visit, banks shall not only recover the loan installment but also assess the overall working of the business unit. To ensure regular visits to borrowers, involvement of all staff members in a branch and proper planning is essential. In addition, services of private professional agencies/ recovery agents shall also be utilized to ascertain the whereabouts of a wilful defaulter and take possession of assets charged to the bank upon serving a legal notice. But enough care should be taken in appointing professional agencies/recovery agents after examining their credentials. It is also essential to keep a constant vigil on them to check whether they adopt any unethical practices for loan recovery. Further, nowadays, debt restructuring, one of the recovery measures, is becoming more popular, which aims at making a project financially viable in the near future, provided the same is technically, commercially and managerially viable and also the borrower being honest and cooperative. Under debt restructuring, concessions and reliefs are granted in the form of reduction in the rate of interest, reduction in loan installment amount, sanctioning of additional finance, reducing the promoter's contribution, financing of cash losses until the project breaks even, etc. Debt restructuring calls for changes in the original loan agreement and should be implemented as per the bank policy. During the pandemic, debt restructuring was extended, which provided a major relief to borrowers.

Wherever debt restructuring is not possible in terms of RRB guidelines, loan compromise shall be considered at the borrower's request of accepting a part of outstanding dues as full and final payment or allowing for the noncompliance of certain terms of the loan, after analyzing the alternative courses of action, genuineness and capacity of the borrower to repay. RRBs should have the Board-approved compromise policy. In the recent past, banks have been able to make sufficient recovery through compromise. But care should be taken to ensure that loan compromise shall not provide a wrong signal to good/regular borrowers. For quick and hassle-free loan compromise, banks should approach Lok Adalats, which are known for effecting mediation and counseling between the parties, i.e., bank and borrower, to reduce the burden on the court, especially with regard to small loans. The Legal Services Authorities Act, 1987 gives statutory status to Lok Adalats in this regard. If a compromise is arrived at, the parties to the litigation sign a statement in the presence of the Lok Adalat, which is expected to be filed in the court to obtain a consent decree. Currently, bank-suits involving a claim of up to 20 lakh may be brought before the Lok Adalat. Nowadays, debt recovery tribunals (DRT) also organize Lok Adalats. If loan compromise is not workable, legal action becomes necessary. To start with, recall notice should be sent to a defaulter under certain circumstances such as the borrower being a wilful defaulter, bank liability being significantly uncovered, death of a borrower, dissolution of a partnership firm, siphoning of funds, the borrower refusing to renew the credit limit, etc. Once the notice is served, most of the defaulters may prefer to pay the bank dues to avoid legal action through the courts. Banks shall make loan recovery through the civil court, DRT, and under the DRT Act and SARFAESI Act, wherever applicable. But legal action is suggested only in the case of dishonest borrowers and also where securities are available. Generally, legal action is a time-consuming and expensive process. Therefore, dependence on legal recovery measures should be exceptional. All the more important is to educate the borrowers to impress upon them regarding the benefits of timely loan repayment.

Conclusion

RRBs play an important role in the dispensation of credit to ensure social and economic justice to the poor and vulnerable. Currently, 43 RRBs, with around 22,000 branches in rural and semi-urban areas, have about 30 crore deposit accounts and 3 crore loan accounts. And, around 90% of their total loans are provided to the priority sector. While their core activity is to provide credit to the farm sector, RRBs also extend credit to rural MSMEs to meet their working capital and investment needs. Fortunately, after the pandemic, there has been a good pick up in the economy and, therefore, RRBs are expected to tap the emerging business opportunities to increase their CD ratio by taking the benefit of higher CRAR. They are also expected to reduce credit risk, which is evident from the present higher level of NPAs. To meet these expectations, RRBs are suggested to reshape their lending practices on sound lines by adopting professional approaches and also by observing due diligence in credit in terms of policy guidelines of RBI and NABARD. Such sound lending practices need to be followed relating to credit appraisal, monitoring and loan recovery, for which suggestions are offered in this paper for the consideration of RRBs. In addition, to reduce the element of hesitancy from the minds of branch managers to lend more and check growth in NPAs professionally, they need to be exposed to training. In addition, RRBs are suggested to compile their success stories on sound lending practices and bring the same to the notice of branch managers, which would motivate them to ensure more good quality lending.H