Sep'18

The IUP Journal of Financial Risk Management

Archives

A Study of the Efficiency of Chili Futures Market in India

Puja Sharma

Research Scholar,

Manipal University Jaipur – Ajmer Express Highway,

Jaipur, Rajasthan, India;

and is the corresponding author.

E-mail: puja2487@gmail.com

Tanushree Sharma

Associate Professor,

Manipal University Jaipur – Ajmer Express Highway,

Jaipur, Rajasthan, India.

E-mail: tanu24feb@gmail.com

Chili is the largest spice exported from India and occupies the first position in terms of value. Chili futures was launched on NCDEX on March 11, 2005. There has been a drastic fall in the prices of different varieties of red chilli in 2017 in Andhra Pradesh and the rest of the country. The recent changes in futures trading of chili contract have led to concerns for the stakeholders. The present paper examines the price discovery and efficiency of chili futures market using econometric models like Johansen's cointegration, vector error correction model, Wald test, impulse response and variance decomposition on data on daily closing spot and futures prices of chili obtained from NCDEX for the period from 2006 to 2016. The results indicate that both the markets are cointegrated and error correction is taking place in both the markets. The Granger causality test result also confirms this. However, Wald test results reveal short-term causality flowing from futures to spot prices for chili. The study observes long-run comovement between spot and futures prices which indicates futures contracts can serve as a useful hedging instrument.

Introduction

The world area and production of chili are around 1.5 million hectares and 7 million tons respectively. India, China, Pakistan, and Indonesia are major chili growing countries. Trade in chili accounts for 16% of the total spice trade in the world. India accounts for about 1.2 million tons of production of chili annually and it exports 20% of its total production. India is the largest exporter of chilies due to its superior quality. The major chili producing states are Andhra Pradesh, Telangana and Madhya Pradesh. It was estimated that in the year 2017-18, production of chili would be 1.367 million tons. There have been fluctuations in chili prices in the last few years.

Agricultural commodity price volatility is an ongoing concern. Price movements may have important implications for allocation of resources for consumers' and producers' welfare. Chili is the largest spice exported from India and occupies the first position in terms of value. The chili market is affected by seasonal price fluctuation. Chili futures was launched on NCDEX on March 11, 2005. With the help of futures platform, producers can hedge the price risk. The study examines the price discovery and efficiency of chili futures market using econometric models.

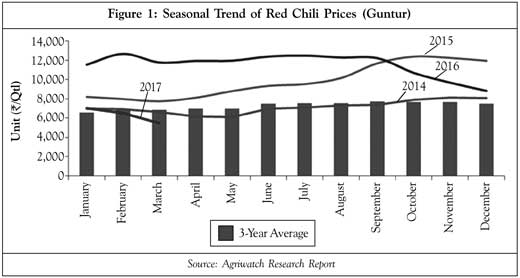

Figure 1 depicts the price of chili in Guntur market. It shows the fluctuation in the price of chili. It is observed that price fluctuated for three consecutive years. This clearly shows that price keeps changing across the years.

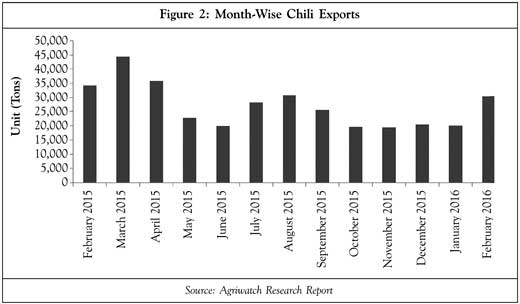

Figure 2 depicts the export quantity of chili. It clearly shows that export quantity has reduced as compared to that in the previous year due to high spot prices. Further it is observed that exports of chili grew in March 2015 as compared to the previous month. The export market for chilies is affected by its overall production in the country, world demand

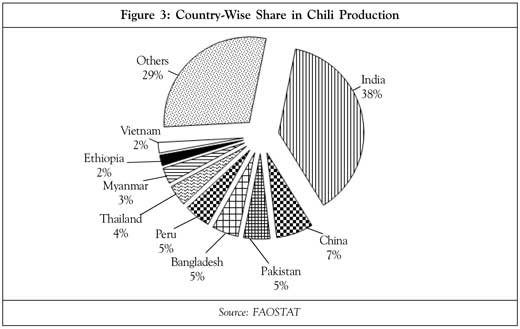

(see Figure 3) and cold storage stocks, while price fluctuates due to changes in season and hedging among varieties of chili. Export demand reduced with the harvest in China. During February 2016, chili export was higher than that of the previous month. The export rate of chili was constant between October 2015 and January 2016. Very slight changes were observed in the respective months. In the year 2015-16, chili exports were 24.21% by value of the total exports of spices from India. The major export destinations are Malaysia, Thailand, Vietnam and Sri Lanka. Chili has been selected for the study due to high fluctuation in its prices during the last few years. The present study seeks to find out the reason for price volatility of chili, i.e., whether the fluctuation occurs due to speculation or not.

Literature Review

Naik and Kumar (2001) used the cointegration theory for assessing the efficiency of major commodity futures market. They concluded that a major reason for the poor performance of Indian futures market could be the lack of adequate participation of hedgers in these markets. Naik and Kumar (2002) concluded that agricultural commodity futures market has not fully developed as a competent mechanism of price discovery and risk management. They found some aspects such as poor management, logistics and infrastructure to blame for the deficient market. Ahuja (2006) concluded that the Indian commodity market has made progress since 2003 with increased number of modern commodity exchanges, transparency and trading activity. Bhattacharya (2007) stated that significant risk-return features and diversification potential have made commodities popular as an asset class. Ranganathan and Ananthakumar (2014) studied the efficiency of soybean in futures trading market. Using QARCH-M-ECM model and cointegration test, they concluded that soybean is impartial in the long run and inefficient for the short-run market. Sayee (2014) studied the functioning of agricultural commodity futures market. Using Johansen's cointegration test, Granger causality and Vector Error Correction Model (VECM), he found that price discovery between spot and futures markets depends upon the nature of commodity, maturity time and liquidity in the market. Sharma (2014) investigated the relationship between potato spot and futures prices. Using Johansen cointegration test, impulse and variance decomposition, she showed that there was no cointegration relationship among the variables. A variance decomposition result indicated a small percentage of changes in spot market is explained by futures market.

Sharma and Malhotra (2015) studied the impact of futures trading activity on the volatility of guar seed spot market prices. The study examined the volatility of spot prices before and after the introduction of futures trading and relationship between futures trading activity and spot price volatility by taking data on NCDEX from 2004 to 2011. Analysis of data was done using GARCH model and Granger causality test. It was observed that there is a positive and significant relationship between futures trading volume and spot returns volatility, and causality is also observed from Unexpected Traded Volume (UTV) to spot volatility. Sharma and Malhotra (2015) used VECM to examine the casual relationship between spot and futures prices for the commodities such as chana, soybean, soya refined oil, guar gum, potato and pepper. She had also used Wald test to measure short-run and long-run causality among the commodities. She concluded that causal relationship is found between chana and pepper. Unidirectional causality was found for soybean and soya oil.

Ali and Gupta (2011) empirically examined the efficiency of futures markets for 12 agricultural commodities traded in the commodity exchanges using Johansen's cointegration approach. They suggest that there is a long-term relationship between futures and spot prices for agricultural commodities like maize, chickpea, black lentil, pepper, castor seed, soybean and sugar. The analysis of short-term relationship by causality test indicates that futures market has stronger ability to predict subsequent spot prices for chickpea, castor seed, soybean and sugar as compared to maize, black lentil and pepper. Kumar et al. (2014) used VECM and bivariate exponential GARCH model to analyze the price discovery and volatility spillovers in Indian spot-futures commodity market. The VECM shows that agriculture futures price index, energy futures price index and aggregate commodity index effectively serve the price discovery function in the spot market, implying that there is a flow of information from futures to spot commodity markets, but the reverse causality does not exist. There is no cointegrating relationship between metal futures price index and metal spot price index. Jain and Arora (2014) made an effort to investigate the volatility in commodity prices. Their study focused on finding out the relationship between futures and spot prices of a selected agricultural commodity, pepper, by applying cointegration test using secondary data for the period of five years. The study found that there is cointegration between futures and spot prices for the selected time period. Ahmad and Sehgal (2015) examined the destabilization effect in the case of India's agricultural commodity market for the sample period of January 1, 2009 to May 31, 2013.

Data and Methodology

The data employed in this study includes daily closing spot and futures prices of chili from 2006 to 2016. The data was collected from NCDEX, which is a leading commodity exchange in India. A total of 2,523 observations were examined for the study. The analysis of data was done by using log of daily closing spot and futures prices. The first differences of spot and futures log prices were taken to calculate price returns.

The series is non-stationary with time-varying mean and variance. But time series data that is non-stationary cannot give proper results. Therefore, the data has to be changed to stationary.

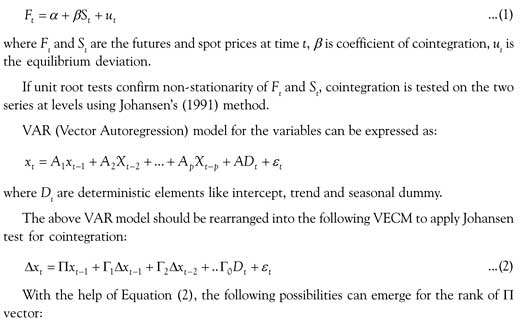

For testing data stationarity, Augmented Dickey-Fuller (ADF) test is used in the paper. If the combination of two non-stationary series is stationary, then they are said to be cointegrated.

Cointegration between spot and futures prices is given by:

- When Rank P = 0, then no cointegration is found among the variables.

- When Rank P = 2, it indicates spot and futures prices are stationary.

- When Rank P = 1, one cointegrating relation is found between the two series.

Results and Discussion

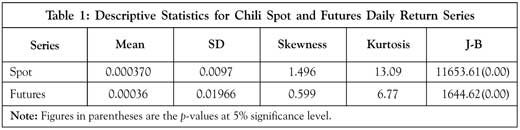

The statistical features of chili spot and futures return series are understood with the help of statistics like mean, standard deviation, skewness, kurtosis and Jarque-Bera (J-B) that are given in Table 1. The average of daily spot and futures prices is positive. The standard deviation is higher for futures as compared to spot. The spot and futures series are not highly skewed. The kurtosis which measures peakedness is higher than the normal value of 3 for both the series, but spot return series has higher kurtosis of 13.09, implying that the deviations are larger in spot market. J-B test statistic used to test the normality has a probability of zero at 5% significance level in both the series, indicating that futures and spot return series are not normally distributed.

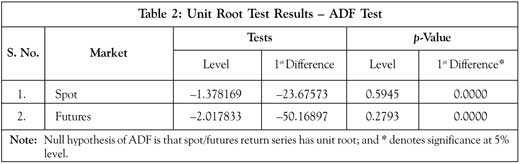

Before examining the long-term relationship between spot and futures prices, unit root test is conducted (Table 2). The results indicate that both series are not stationary at levels, but their first differences are stationary. The results are the same if the test is run with both intercept and trend. The condition for cointegration test is satisfied which sets the stage for testing long-run relation between spot and futures prices.

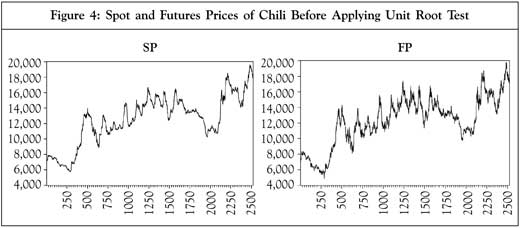

Figures 4 and 5 reflect graphically the trend of daily spot and futures price. Figure 4 shows the data of spot and futures price of chili which is not stationary for the respective time period. For further generalization and forecasting, the data has to be made stationary. So, the data is made stationary by taking first difference of spot and futures log returns series.

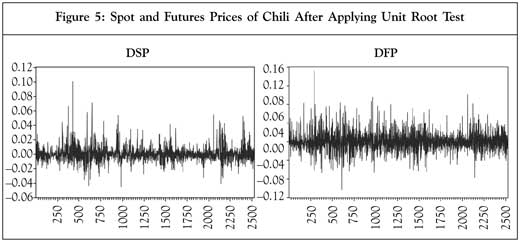

Figure 5 shows the data of futures and spot price which is converted into stationary with the help of unit root test. After the first difference, the data becomes stationary.

Cointegration Test

Cointegration model is used to check whether there is long-run relationship among the variables, i.e., spot and futures prices of chili. There are 2,523 observations having a lag of 4. In the Johansen's procedure for testing long-run relationship, the eigenvalues are arranged in descending order and the rank of cointegration matrix is analyzed using trace and max which are maximum-likelihood ratio-based statistics.

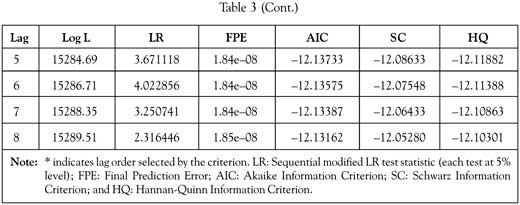

The results of cointegration test are based on trace statistics and maximum eigenvalues test. We have to find out whether there is cointegration among variables or not. For this lag 4 is selected based on the results presented in Table 3. The lower the value, the better the model. So, in this, the maximum number of times lag 4 is recommended. Now that means three criteria are asking for lag 4. So, we take 4 lag to run the model. It means that optimum lag would be 4, and we shall use this lag 4 to run the Johansen cointegration test and VECM.

The results of cointegration have been reported in Table 4 and are based on the third model which is used when there is stochastic trend in the series. The results of cointegration test show that there is at least one cointegrating equation so we can run VECM. The value of

t-statistics in all the cases is more than the critical value, so we reject the null hypothesis. So, there is at least one cointegrating equation. Hence, it proved that there is long-run relationship among the variables. According to trace statistics, all the variables are cointegrated and the same is the case as in the case of maximum eigenvalue. So, when variables are found cointegrated, we can run VECM model. This has an important implication that the chili spot and futures prices have a stable long-run relationship and convergence often takes place on the expiry of the contract. For futures markets to serve the purpose of hedging price risk, long-run comovement is an important input.

Short-Run Dynamics – VECM and Granger Causality

In the short run, there maybe deviation and it is necessary to adjust those deviations. For these adjustments of deviations VECM is required. VECM helps to analyze such temporary deviations. It also helps to find out the long-run relationship between the two series. VECM is necessary to analyze the responses of the variables. Lag selection is done before running the VECM. The number of lags of the futures and spot prices, which is required to run the model, is selected. For this study, lag 4 is selected to run the error correction model.

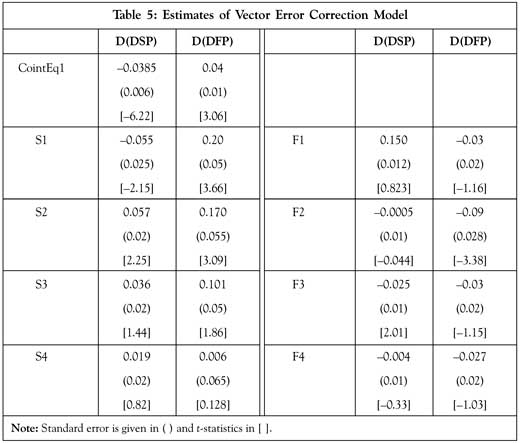

After identifying a cointegrated equation between spot and futures prices, a VECM is estimated. Table 5 indicates that error correction is not significant, which shows that the

model is in equilibrium state. The coefficient of error correction terms is negative and the series move downward to the equilibrium. Since the error correction term in futures equation is greater than that in the spot equation, it implies that the spot price reacts rapidly and leads to price discovery. Error correction terms for both spot and futures price series are significant in the long term. We find bidirectional causality among spot and futures price in the long term. This implies that in case of chili, both spot and futures market respond to restore the equilibrium whenever there is some price discrepancy.

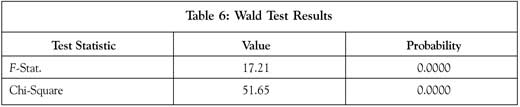

To check whether future price causes spot price or not, Wald test is used. The results are presented in Table 6. We know that if the p (value) is less than 0.05, we reject the null hypothesis that there is no short-term causality from futures price to spot price. Thus, results reveal that there is short-term causality flowing from futures to spot price.

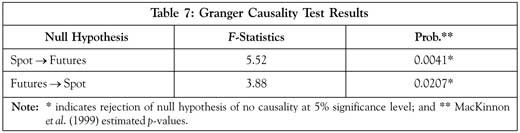

The dynamic relationship between spot price volatility and futures trading activity is ascertained by running Granger causality test. From Table 7 it is clear that spot price and futures price have causal influence on each other. The results of Granger causality test reported in Table 7 indicates that the null hypothesis is rejected at 5% significance level.

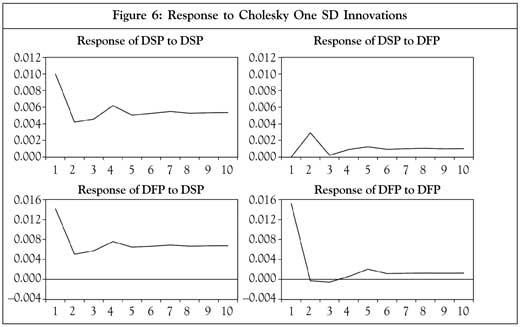

Impulse Response

To examine the coefficients of VECM, impulse response function and variance decomposition are used to show the impact of changes in the value of one variable on another. These techniques are used to find out the effect of shock on the variables. Spot returns reflect greater response to shocks in futures which requires a few days to settle down (Figure 6). However, futures response to shock in spot returns is very minimal.

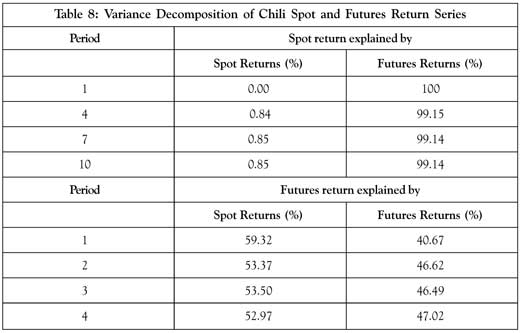

Variance Decomposition

Next, we examine the chili spot and futures returns using variance decomposition. This model helps to know what proportion of variation exists in both spot and futures returns, i.e., whether spot returns variate due to its shock against futures returns shock or vice versa. Table 8 shows the percentage variation in chili futures returns. It is observed from Table 8 that spot

price is explained by futures price (99.14%). Hence, it can be inferred that futures price leads spot price in chili.

Conclusion

Chili futures contract was introduced on NCDEX in March 2005. This helps farmers, exporters and traders to fulfill the hedging needs. At the same time, this also helps them to assist the spot market participants in making pricing decisions. Exporters insure themselves against price risk as there is increase in the export demand. The speculators can easily enter or exit the market as the contract is highly liquid in nature. Therefore, the present study is an effort to examine the efficiency and price discovery of chili futures market using econometric models such as Johansen's cointegration, Granger causality, VECM, impulse response and variance decomposition. The period covered for the study starts from the launch of chili futures trading contracts in 2006 through 2016. The study observes long-run comovement between spot and futures prices, which indicates futures contracts can serve as a useful hedging instrument. Error correction terms for both spot and futures price series are significant in the long term . We found bidirectional causality among spot and futures price in the long term for chili. Error correction takes place in both the markets to restore equilibrium. The Granger causality result also indicates casual relationship between the variables. However, short-term causality flowing from futures to spot price in chili is also observed.

References

- Ahmad Wasim and Sehgal Sanjay (2015), "The Investigation of Destabilization Effect in India's Agriculture Commodity Futures Market", Journal of Financial Economic Policy, Vol. 7, No. 2, pp. 122-139.

- Ahuja Narender L (2006), "Commodity Derivatives Market in India: Development, Regulation and Future Prospective", International Research Journal of Finance and Economics, Vol. 2, No. 1, pp. 153-162.

- Ali Jabir and Gupta Bardhan Kriti (2011), "Efficiency in Agricultural Commodity Futures Markets in India", Agricultural Finance Review, Vol. 71, No. 2, pp. 162-178.

- Bhattacharya Himdari (2007), "Commodity Derivatives Market in India", Economic and Political Weekly, Money Banking and Finance, Vol. 42, No. 13, pp. 1151-1162.

- Jain Mamta and Arora Rakhi (2014), "An Analytical Study of Price Volatility of Selected Agricultural Commodity (Black Pepper) Traded on NCDEX", Intercontinental Journal of Finance Research Review, Vol. 2, No. 10, pp. 2321-2354.

- Johansen S (1991), "Estimation and Hypothesis Testing of Co-Integrating Vectors in Gaussian Vector Autoregressive Models", Econometrica, Vol. 59, No. 6, pp. 1551-1580.

- Kumar Mantu Mahalik, Debashis Acharya and Suresh Babu M (2014), "Price Discovery and Volatility Spillovers in Futures and Spot Commodity Markets: Some Empirical Evidence from India", Quantitative Approaches to Public Policy – Conference in Honor of Professor T Krishna Kumar.

- MacKinnon J G, Haug A A and Michelis L (1999), "Numerical Distribution Functions of Likelihood Ratio Tests for Cointegration", Journal of Applied Econometrics, Vol. 14, No. 5, pp. 563-577.

- Naik Gopal and Kumar Jain Sudhir (2001), "Efficiency and Unbiasedness of Indian Commodity Futures Market", Indian Journal of Agricultural Economics, Vol. 656, No. 2, pp. 185-197.

- Naik Gopal and Kumar Jain Sudhir (2002), "Indian Agricultural Commodity Futures Market: A Performance Survey", Economic and Political Weekly, Vol. 37, No. 30, pp. 3167-3173.

- Ranganathan Thiagu and Ananthakumar Usha (2014), "Market Efficiency in Indian Soybean Futures Markets", International Journal of Emerging Markets, Vol. 9, No. 4, pp. 520-534.

- Sayee Prasanna G R (2014), "Performance Evaluation of Agricultural Commodity Futures Market in India", The IUP Journal of Applied Finance, Vol. 20, No. 1, pp. 34-45.

- Sharma Tanushree (2014), "Lead Lag Relationship and Price Behavior in Potato", International Journal of Business Quantitative Economics and Applied Management Research, Vol. 1, No. 7, pp. 91-104.

- Sharma Dinesh and Malhotra Meenakshi (2015), "Impact of Futures Trading on Volatility of Spot Market: A Case of Guar Seed", Agricultural Finance Review, Vol. 75, No. 3, pp. 416-431.