Sep'18

The IUP Journal of Financial Risk Management

Archives

Price Discovery and Volatility Spillovers: Evidence from Non-Agricultural Commodity Market in India

Ruchika Kaura

Assistant Professor,

Atma Ram Sanatan Dharma College,

University of Delhi, Dhaula Kuan; Research Scholar,

Indira Gandhi National Open University,

Maidan Garhi, New Delhi, India.

E-mail: ruchikakaura@gmail.com

Nawal Kishor

Professor,

School of Management Studies,

Indira Gandhi National Open University,

Maidan Garhi, New Delhi 110068, India.

E-mail: nkishor@ignou.ac.in

Namita Rajput

Principal,

OSD, Sri Aurobindo College (Evening),

University of Delhi,

Malviya Nagar, New Delhi 110017, India;

and is the corresponding author.

E-mail: namitarajput27@gmail.com

Commodity futures market has grown considerably in India over the past few years. The study aims to investigate the issue of price discovery and volatility spillovers in the context of non-agricultural sector of Indian commodity market using econometric models. The study uses the futures and spot price data of nine highly traded non-agricultural commodities of Multi Commodity Exchange of India Limited. The results prove that all commodities futures and spot prices are cointegrated. There exists bidirectional error correction in all commodities spot and futures market, and futures market leads in price discovery over the spot market. Only in the case of commodity gold, spot market leads the futures market. The results of GARCH test prove that there are bidirectional spillover effects in the case of most of the commodities, and spillovers from futures returns to spot returns are more prominent than the other way round. The results imply that futures market in India is playing its role in improving pricing efficiency and also influences the spot market volatility.

Introduction

Commodity futures market was an uncommon phenomenon in India until the early 1980s. Its development was almost sluggish owing to numerous government regulations and other binding factors. However, the economic liberalization during the 1990s led to the revival of these markets and significant and apt government policies helped in their impulsive and spectacular growth in the country. At present, commodity market is attaining astonishing expansion in terms of range of commodities offered, trading volume, technological upgradation and transparency. The regulatory reforms have also supported the development of commodity markets in the country with the Forward Market Commission (FMC) earlier and Securities Exchange Board of India (SEBI) at present acting as market regulators. Commodity markets are immensely beneficial for the economic development of the country and play an effective role in price risk management, price discovery and price stabilization of the commodities to benefit the producers, traders, processors and other stakeholders.

The topic of price discovery and volatility spillover concerning spot-futures commodities market has been a matter of great interest for all. The foremost benefit of commodity futures trading is that these markets enable the price discovery of the commodities. These markets are the means for speculative activities and also provide a platform for implementing and evaluating hedging and trading strategies and helping in risk management (McMillan and Speight, 2001). The futures price is as an adaptation of opinions relating to demand and supply conditions in future based on the available information at the time the price is recorded (Fortenbery and Zapata, 1997). In efficient market system, new information is impounded at the same time into cash and futures markets (Zhong et al., 2004). But in reality, the introduction of new information in the market may lead one market to register its impact faster than the second market, resulting in price differences between the markets. In general, futures market may react to the new information faster than the physical market due to lower transaction cost and more liquidity. Measuring the lead-lag relationships of the markets and identifying the dominant/leading markets in the pricing process is crucial as it helps to recognize arbitrage opportunities and strategies to lessen risk (Koontz et al., 1990). The present study therefore focuses on the price discovery issue as the first aspect as this is the most significant function of commodity futures market.

Volatility is the second aspect which the present study seeks to explore. Volatility denotes risk and uncertainty and is regarded as a negative sentiment in the market. A highly volatile market is featured with quick price fluctuations and lowers the stakeholders' confidence and participation in the market. It deters the economic growth and prompts the government to intervene in the market. Commodity prices are unstable and volatile. Reasons can be numerous such as unpredictable natural calamities, domestic and global policies, industry structural changes, upturn or slump in equity market, sudden rise or fall in export, import, exchange rates, etc. Therefore, the empirical modeling of commodities market volatility and its spillover to the other markets is very important because it creates ambiguity and risk to the parties concerned such as the producers, consumers and others. The study seeks to explore the volatility spillover impacts of futures market over spot market and vice versa to examine the inter-relationship between the spot and futures prices.

Earlier studies in the context of commodities derivatives market are either related to the developed countries, or in India these are related to agricultural commodities. Studies focusing on futures-spot interactions of non-agricultural commodities taken together are very limited. So, the present study attempts to analyze the issues of cointegration, causality and volatility in the context of non-agricultural commodities which include futures and spot price interactions of bullion, metals and energy. This study contributes to the present literature by providing innovative insights about the Indian non-agricultural commodities market and provides evidences on price discovery and volatility spillover analysis. The study covers nine non-agricultural commodities and also a longer study period in comparison to the earlier studies.

The study is based on a sample of nine non-agricultural commodities which are highly traded on Multi Commodity Exchange of India Limited (MCX). The commodities selected for study are bullion and metal commodities, i.e., gold, silver, aluminum, copper, lead, nickel, zinc and energy commodities, i.e., crude oil and natural gas. These commodities are selected on the basis of their high frequency of trading on the exchange.

Overview of Non-Agricultural Commodities

Non-agricultural commodities (bullion, metal and energy) are different in nature from agricultural commodities in terms of their storability as these are non-perishable. Also, these are less impacted by weather changes. So, the prices of these commodities are less volatile in short term in comparison to agricultural commodities. Their prices are affected more by global changes like political and economic events, interest rate changes, etc. Energy commodity market in India is complex, dynamic and increasingly global. Of the various energy forms, Brent crude oil, crude oil and natural gas together constitute more than 50% of the total primary energy consumption in India. These commodities are subject to sudden supply disruptions and price volatility. Bullion commodities, also known as precious metals, are mainly gold and silver, apart from platinum and palladium. According to World Gold Council, investments in gold are the most important contributor towards industry growth. Gold prices are extremely unstable, influenced by huge flows of speculative money. Metal commodities, also known as base metals, include commodities like aluminum, copper, lead, nickel, zinc, etc. India's penetration levels in metal commodities are substantially lower, when compared to not only mature markets, but also countries like China. The metals sector is quite competitive, and presents attractive growth opportunities as well.

The paper is organized as follows: it presents a review of related literature, followed by the objectives and description of data and research methodology used in the study to achieve the objectives. Subsequently, it presents and discusses the empirical results, and finally, conclusion is offered.

Literature Review

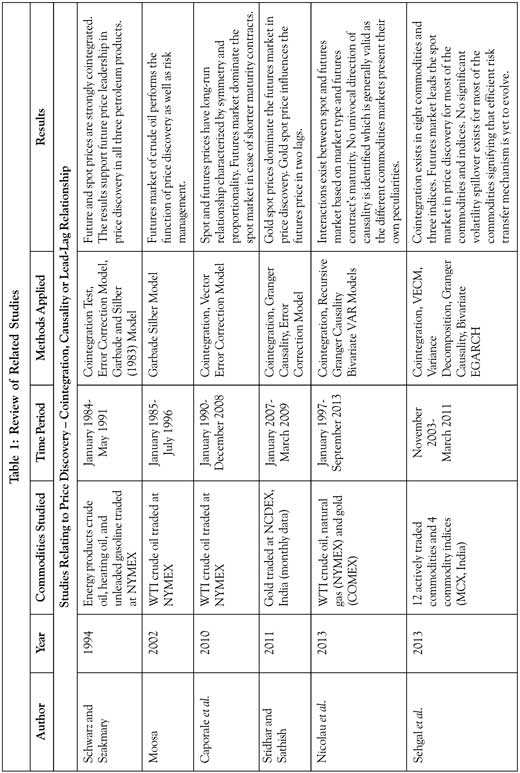

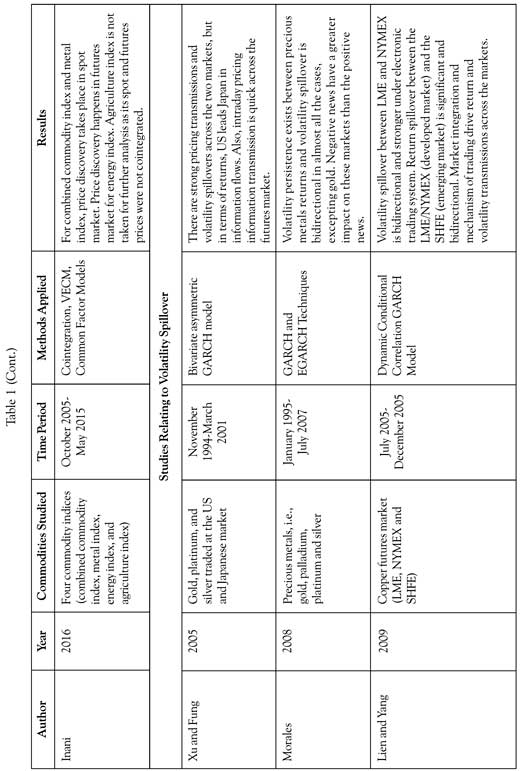

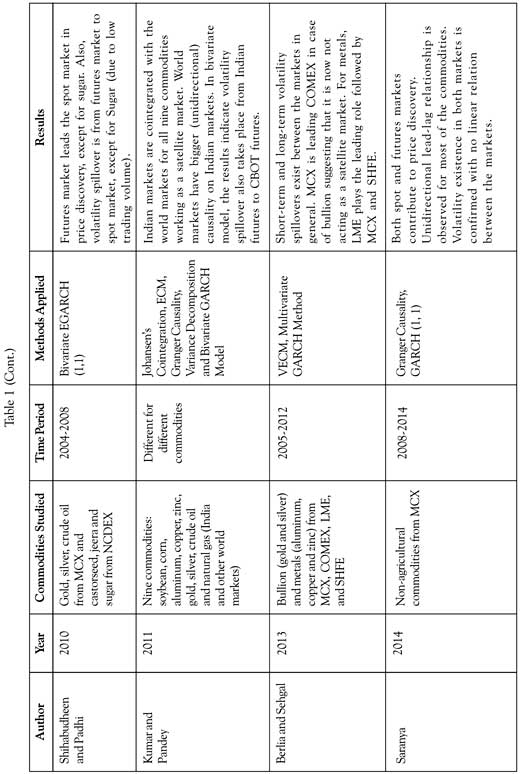

The issues of price discovery and volatility relationship of futures and spot markets are topics of enthusiasm for academicians, practitioners, and regulators. But most of the studies concerning these issues focus on agricultural commodities only. So, an attempt was made to focus on bullion, metal and energy commodities and analyze the studies relating to price discovery and volatility spillover in the context. Table 1 presents the details of the review conducted.

Objective

Based on the literature review, the present study aims to:

- Examine the price discovery dynamics, i.e., cointegration, causality and lead-lag relationships of spot-futures prices for select non-agricultural commodities.

- Examine the volatility spillover of returns in futures and spot market for these commodities.

Data and Methodology

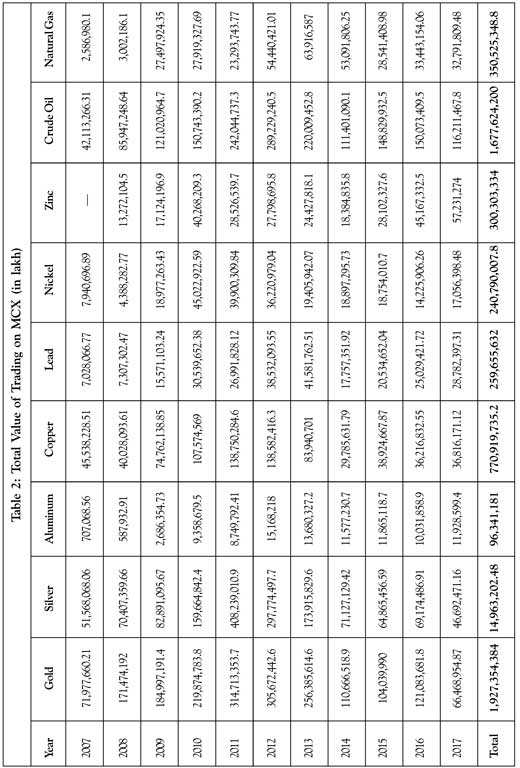

The study uses data of nine non-agricultural commodities traded on MCX comprising two bullion commodities: gold and silver, five metal commodities: aluminum, copper, lead, nickel and zinc, and two energy commodities: crude oil and natural gas. The reason for focusing only on these commodities is that currently these commodities are being most actively traded on MCX platform and also the trading value of these commodities on MCX is very high as presented in Table 2.

The data for this study is collected from the official website of MCX, which is the leading player of commodity futures trading in India. MCX is India's first listed commodity futures exchange that offers online trading across many commodity segments, viz., bullion, metals, energy and agri commodities. It is India's leading commodity exchange with over 89% market share in terms of the value of commodity futures contracts traded in FY 2017.

The data comprises daily closing spot and futures prices of these commodities collected from the website of MCX. The study covers fairly longer time period in comparison to prior studies. The data period ranges from January 2007 to July 2017 for all commodities, except for Zinc whose data ranges from January 2008 to July 2017 due to availability of data for this period only.

Tests of Price Discovery and Causality

Price discovery is the most significant function of any financial market. It describes the process of information production and exchange across the markets. Price discovery refers to the dynamic process of incorporation of new information into the market prices. The process focuses on whether new information impacts spot market or futures market first. As a preliminary investigation, basic descriptive statistics of the time series data are examined to have an initial insight about data characteristics, i.e., measures of central tendency, measures of variability, kurtosis and skewness. This initial analysis helps to understand the data in a meaningful manner to allow easy interpretations. Another step in preliminary investigations in case of time series data is the testing for stationarity. For this purpose, Augmented Dickey-Fuller (ADF) and Phillips and Perron (PP) tests have been applied. These tests take the existence of a unit root as the null hypothesis as against the alternative of stationarity. If the null hypothesis is rejected, then the series is assumed to be stationary.

If the spot-futures price series are integrated to the same order, cointegration techniques can be used to know the existence of cointegration and long-run relationship between the price pairs. A long-run relationship explains the comovement of the variables over long time. Johansen's (1991) cointegration test is used in the study to test the cointegration between futures and spot markets. The test is more sensitive to the lag length employed. It is pertinent to mention that in our study, Schwarz Criterion (SC) has been used to determine the optimal lag length. The intent of its estimation is to ensure that no serial correlation is present in the residuals.

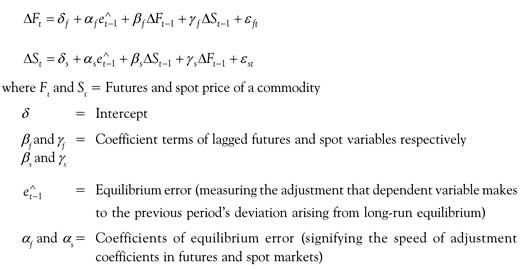

If there exists cointegration between the price pairs, the Vector Error Correction Method (VECM) can be employed to know which market dominates in price discovery. In general, a long-run equilibrium relationship exists between two economic variables. In the short-run, a disequilibrium may arise, but it is corrected in the next period with the error correction mechanism, thus, integrating the short-run and long-run behavior. VECM provides a measurement of the relative magnitude of adjustment occurring between the two variables in an effort to reach the equilibrium. Hence, the Error Correction Model (ECM) is:

The coefficients of the equilibrium error, af and as claim significant implication in an ECM as they act as evidence of direction of casual relation and shows the speed at which discrepancy from equilibrium is corrected or minimized. The model is an ECM if at least one coefficient is non-zero.

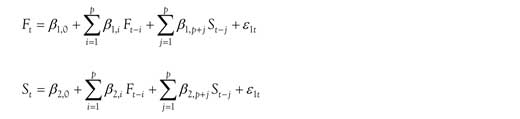

Further, Granger causality test has been deployed on the futures-spot prices series of the commodities to find the causal relationship in the short run. Granger (1969) gave a bivariate framework where standard F-test determines the short-term causal relationship between two variables. A variable x Granger-causes another variable y if past values of x help in the prediction of the present level of y given all other suitable information. The statement 'x Granger-causes y', only means the precedence of information content and not the effect or result. The study uses Granger causality test estimating the following two regression equations:

where p is the number of lags used for the variable and the error terms e are white noise. These equations test the existence of short-term relationship between the variables F and S. Further, if there is cointegration in futures and spot prices, causality must exist in either direction, unidirectional or bidirectional.

Volatility Analysis – GARCH Model

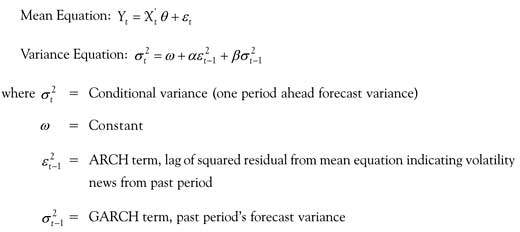

Volatility, quantified by variance of returns, is generally used as a risk measure of financial assets. To model a financial time series, Autoregressive Conditional Heteroskedasticity (ARCH) model was developed by Engle (1982) which exhibits time-varying conditional variance. Later, the model was extended by Bollerslev (1986) and Taylor (1986) to Generalized ARCH (GARCH) model for estimating stochastic volatility in which the conditional variance depends upon lagged square residuals (ARCH term) from the mean equation and its own lagged values, i.e., previous period forecast variance (GARCH term). This model is used on stationary series so the spot and futures price series are converted into respective return series by applying the formula:

-

R=log(Pt)-log(Pt-1)

GARCH(1, 1) Model

It implies the presence of first order GARCH term (denoted by first number) and a first order ARCH term (denoted by second number). The GARCH(1, 1) model is described by two equations:

GARCH (q, p) Model

It implies higher order GARCH models where q or p or both are greater than 1. It is described by the following variance equation:

Appropriate order GARCH model is fitted for different commodities based on minimization of Akaike Information Criterion (AIC) and SC and the fitted model is further tested for the presence of any ARCH effects by applying ARCH-LM (ARCH-Lagrange Multiplier) test. This is the test for checking presence of serial correlation in the residuals of fitted GARCH model.

Results and Discussion

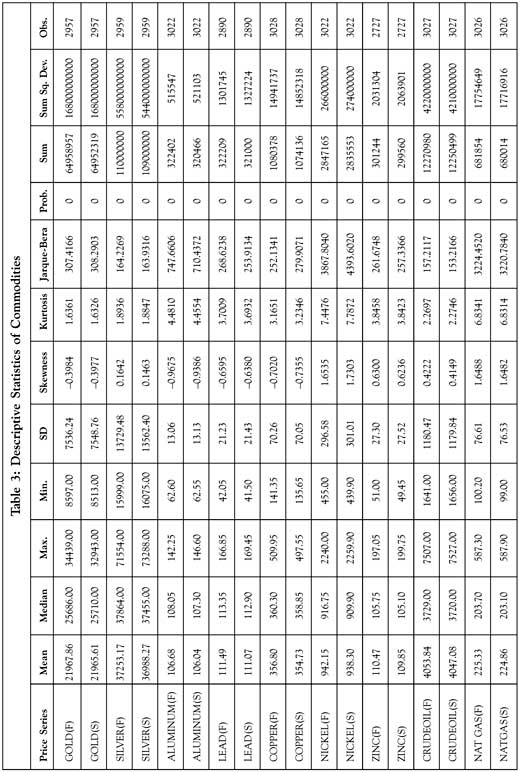

To begin with the preliminary investigation, the descriptive statistics of the futures and spot price series of the commodities are presented in Table 3.

For the period under study, the mean price of futures series is greater than the mean price of spot price series. Standard Deviation, a measure of variation, shows that its value is more for spot price series than the futures price series in case of most of the commodities. For commodities, silver, copper, crude oil and natural gas futures price is more volatile as its value is greater than the spot series value. For other commodities, spot price is more volatile than the futures price. The skewness, a measure of asymmetry of the distribution around mean, shows that the price series of gold, aluminum, lead and copper are negatively skewed, while that of other commodities is positively skewed. The kurtosis, which helps to know the normal or abnormal shape of a distribution, shows that commodities like gold, silver and crude oil have platykurtic distribution (k<3), whereas the other commodities have leptokurtic distribution (k>3). Jarque-Bera test statistic measures the difference of the skewness and kurtosis of the data series from the normal distribution. The very small probability values defy the assumption of normality of the data. Thus, the data is non-normal with high standard deviation, skewness and kurtosis.

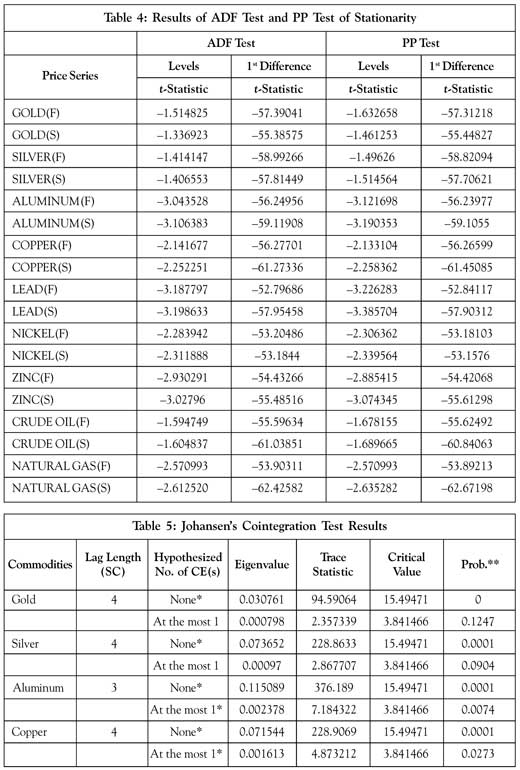

To begin the empirical investigations, ADF test and PP test are employed to test the stationarity of the spot and futures price series of the commodities and the results are presented in Table 4.

The output of both the tests show that value of t-statistic at first difference (return series) for all commodities turn out to be much higher than the critical value (–3.96482) at 1% significance level. It shows that the price pairs are non-stationary at levels, but at first difference, all the price series are stationary; that is the behavior of most of the time series data. Thus, the price pairs of all the commodities are non-stationary and they are integrated to the order of one, i.e., I(1).

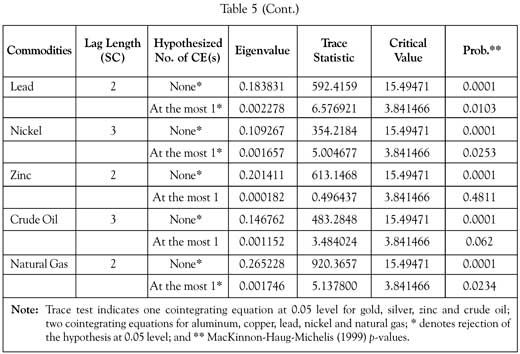

If the time series come out to be non-stationary, cointegration test can be used to know the presence of constant long-run relationship between the price pairs. The presence of cointegration between the price pairs exposes the extent to which two markets have moved together towards long-run equilibrium. The lag length as per the SC and the output of Johansen's cointegration test are reported in Table 5.

The results show that at least one cointegration exists between spot and futures prices of all the commodities under study. Thus, the results confirm long-run equilibrium relationship in the spot and futures market for all the commodities. Even though the markets do not move in sync in short term, in the long term these disturbances get corrected and markets get

in synchronization. The results of the study are consistent with the previous studies such as Schwarz and Szakmary (1994), Srinivasan and Deo (2009), Caporale et al. (2010), Sridhar and Sathish (2011), Srinivasan (2012), and Sehgal et al. (2013).

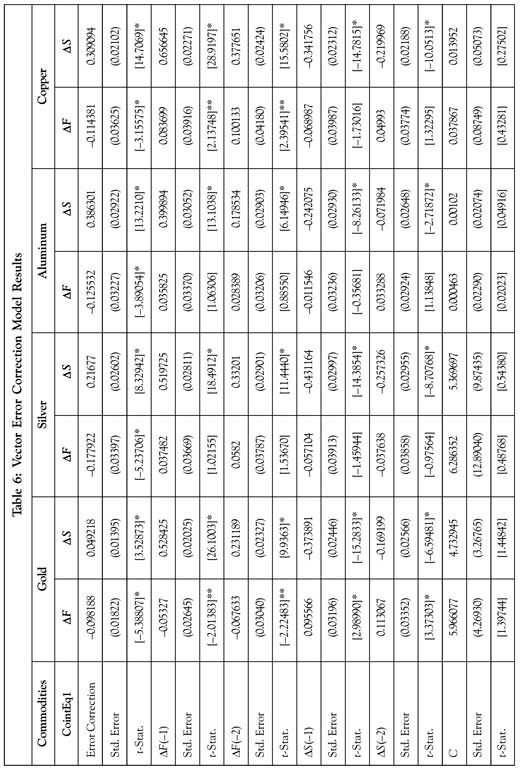

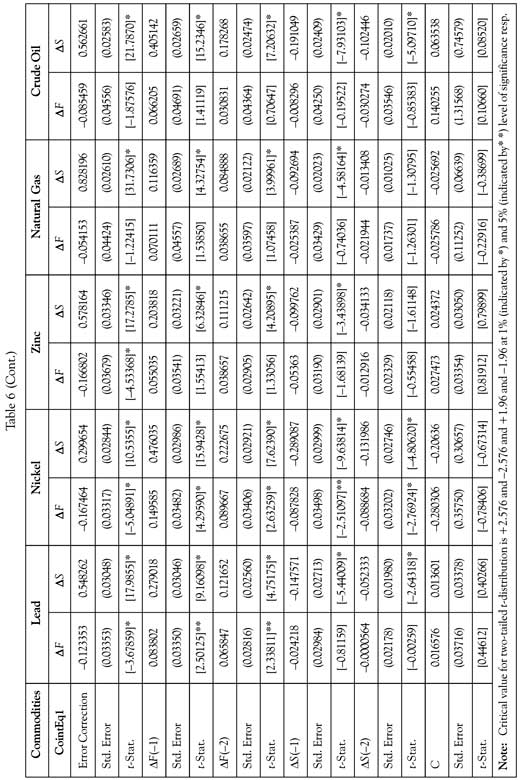

If the price series are non-stationary at levels and are cointegrated, VECM is most suitable to capture the relationship between futures and spot prices. In the process of price discovery, the market which incorporates new information faster, is said to be more efficient than the other market. Thus, it is the leading market which makes greater contribution towards price discovery. The VECM estimates the Error Correction Terms (ECTs) and the coefficients of ECTs provide insight into the adjustment process of the markets to reach the equilibrium. The results of VECM are presented in Table 6.

The results show that in case of bullion and metal commodities, error correction coefficients are statistically significant in both the equations of spot and futures markets with correct signs, suggesting a bidirectional error correction in all these commodities under study. This shows that both futures and spot markets of these commodities will make adjustments to restore the equilibrium during the subsequent period once the price relationship of these markets moves away from the long-run equilibrium. Firstly, in case of commodity gold, at 1% level of significance, 1-day and 2-day lagged futures price has significant impact on spot price change (0.52% at first lag and 0.23% at second lag). But, 1-day and 2-day lagged spot price change is only significant for futures price change to the extent of 0.095% and 0.11%. The ECT shows that the adjustment extent of gold futures price is more (0.098) than the spot price (0.049). Thus, in case of gold, explanatory power of spot prices is more

than the futures prices. In case of other metal commodities, like silver, aluminum, copper, lead, nickel and zinc, the ECT of spot price is greater than the futures price indicating that spot market makes greater adjustment in the process of reaching the equilibrium. Also, 1-day and 2-day lagged futures price change has significant impact on spot price change, but 1-day and 2-day lagged spot price change does not impact futures price change significantly, except in case of commodity nickel where lagged spot price change also significantly influences futures price change but to a lesser extent. Thus, the results indicate that in case of all these metal commodities, futures market plays a dominant role in spot price change. In gold, spot market has stronger impact on futures price change implying that spot market of gold is also informationally efficient in India. As gold traders trade more frequently in the spot market, information transmission among gold traders in spot market happens efficiently. These results are in conformity with the previous research (Sridhar and Sathish, 2011; Srinivasan and Ibrahim, 2012; and Joshy and Ganesh, 2015).

In the case of two energy commodities, i.e., crude oil and natural gas, the short-term ECT is significant for spot price only and not for futures prices signifying that spot market makes more adjustment in the short term. Also, 1-day and 2-day lagged futures price change has significant impact on spot price change, whereas 1-day and 2-day lagged spot price change has no significant impact on futures price change. Thus, in crude oil and natural gas, futures market has a very dominant role in spot market change.

Thus, for most of the commodities, futures market plays a leading role in the process of price discovery as it has significant impact on spot price change. These results are in conformity with the theory and also seems rational because futures market has structural advantages over the spot market in terms of low transaction cost, high liquidity, easy leverage position, low margin, etc. thereby, attracting larger traders to participate in the market. So, when some shock or new information arrives in the market, futures market reacts first. Thus, futures market discover prices in spot market for these commodities. These results are in conformity with those of the previous studies (Mahalik et al., 2009; Shihabudheen and Padhi, 2010; Sehgal et al., 2013; Shakeel and Purnakar, 2014; Sharma, 2015; Singh, 2015; and Sridhar et al., 2016).

As the next step, Granger causality test is used to know the short-run causality relationship between futures and spot prices of the commodities. The results of Granger causality tests are reported in Table 7. The results of Granger causality test show bidirectional causality in the spot and futures prices for all the commodities. The value of F-statistic exhibits that futures Granger-causes spot with much stronger impact than the other way round. The results support the fact that futures market of these commodities strongly influence their spot markets and thus, futures market discovering the prices of these commodities and commodity market in India is informationally efficient. These results are also corroborate to those of previous studies (Ryoo and Smith, 2004; Ali and Gupta, 2011; Sehgal et al., 2013; Shakeel and Purnakar, 2014; and Sridhar et al., 2016).

Volatility Analysis – GARCH Model

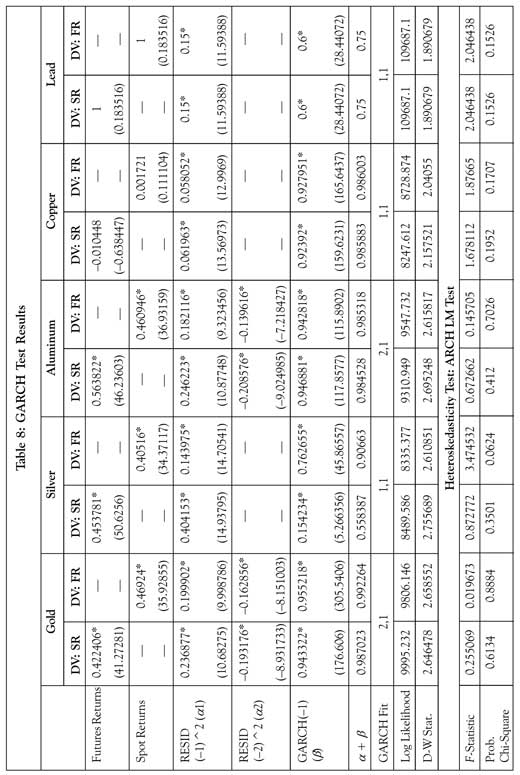

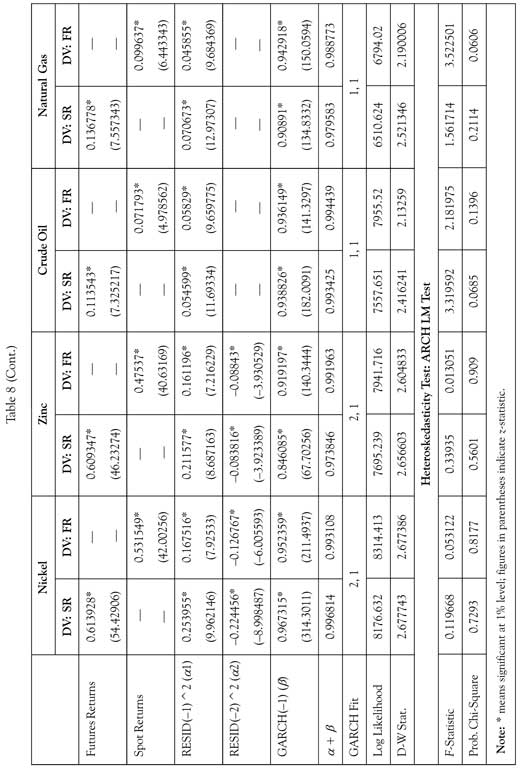

GARCH model was fitted on the basis of minimization of AIC and SC to examine the nature and extent of volatility spillovers across the futures-spot markets. The results of GARCH (q, p) test applied to all nine commodities are presented in Table 8.

If the coefficient of futures returns (spot returns) in the mean equation is significant for a commodity, it means spot returns (futures returns) will increase due to increase in futures returns (spot returns). Table 8 shows that for seven commodities—gold, silver, aluminum, nickel, zinc, crude oil and natural gas—spot returns and futures returns coefficients are positive and significant at 1% level. The results imply that spot returns increased the futures returns and futures returns increased the spot returns, i.e., volatility spillover effects are bidirectional. Excepting gold, the spillover coefficient from futures returns to spot returns is greater than the coefficient from spot returns to futures returns. For example, in case of silver, the spillover coefficient from futures returns to spot returns is 0.453781 whereas coefficient from spot returns to futures returns is 0.40516. It means futures market is exporting its volatility to spot market more than in the reverse direction. In case of commodity gold, coefficient of spot returns (0.46924) is more than futures returns (0.422406). Thus, the volatility spillover effects are more from spot market to futures market in case of gold. These results are consistent with the price discovery results discussed earlier in this paper. In case of commodities, copper and lead, the direction of volatility spillover cannot be identified. The ARCH coefficients (a) and GARCH coefficients (b) for all commodities are highly significant for both futures and spot returns. It suggests that volatility of current day depends on previous day's information of volatility and previous day's squared residuals. The sum of coefficients is close to 1 for spot and futures returns for most of the commodities which indicates volatility persistence during the study period. Thus, today's volatility shocks will influence the expectation of volatility many days in the futures, i.e., volatility shocks die slowly. These results are consistent with those of the previous studies such as Mahalik et al. (2009), Shihabudheen and Padhi (2010), and Sehgal et al. (2013). The results of ARCH-LM test indicate that the fitted GARCH model has no further ARCH effects.

Conclusion

In this study, the futures-spot dynamics of highly traded non-agricultural commodities of MCX are explored. To examine the first objective of price discovery, Johansen cointegration test, VECM and Granger causality test have been applied. Cointegration test reveals that a long-run equilibrium relationship exists between futures-spot prices of all nine commodities under study. The VECM results indicate a bidirectional error correction in all commodities and the domination of futures market over the spot market in price discovery process in case of eight commodities under study. It is only in case of commodity gold, spot price leads the futures price in price discovery process. Thus, gold's spot market is more informationally efficient in India. The results of Granger causality highlight bidirectional causality in the spot-futures prices of all the commodities with the fact that futures Granger-causes spot with much stronger impact. The results suggest that the commodity futures market in India plays a leading role in the process of price discovery and thus, it is becoming informationally efficient and cost competitive. Indian commodities derivatives markets have grown immensely since the introduction of online trading platforms in 2002-03. As a result of electronic trading, the volume of trade on these markets is high enabling them to expose new information with respect to the price of the commodities quickly. Also, less transaction cost, more liquidity and automation are positive factors for these markets to serve as efficient price discovery vehicle. Whereas, spot markets have low trading volumes, are physical in nature, not automated and are also seasonal in case of some commodities.

To examine the second objective of volatility spillover across futures-spot market, price series are converted into return series and are modeled through GARCH test. The results indicate that there are bidirectional spillover effects in case of seven out of nine commodities and there is volatility persistence throughout the period of study. For six commodities, volatility spillovers from futures returns to spot returns are more prominent than the other way. This result is consistent with the price discovery result. Analysis of volatility spillover provides constructive insights about the information transmission and risk-transfer mechanism across the futures-spot market. As the rate of information flow increases, volatility of both spot and futures market will increase. Both the markets are responsible for causing volatility in the other market and are competent to transfer their impacts to the other. But futures markets are more volatile in comparison to spot markets and they export their volatility to the underlying spot market as well. Thus, it can be concluded that futures market of non-agricultural commodities in India is more efficient as compared to spot market in price discovery and also, influences the spot market volatility.

The study has important implications for those involved in commodities trading. Understanding information flows across markets is useful for hedgers looking for cross-market investment opportunities for hedging their risk. Information about price discovery and volatility spillovers in futures-spot markets of energy and metal commodities can be of great use for firms engaged in mining/processing, trading and marketing of these commodities. Knowledge of futures-spot price movements and directions of returns would help individual investors in taking rational trading decisions. Besides being of academic interest, the findings are useful to financial economists, analysts and policy makers to suggest and formulate policies, regulatory framework and implement control measures to enhance the integrity and stability of the MCX

References

- Ali J and Bardhan Gupta K (2011), "Efficiency in Agricultural Commodity Futures Markets in India: Evidence from Cointegration and Causality Tests", Agricultural Finance Review, Vol. 71, No. 2, pp. 162-178.

- Berlia N and Sehgal S (2013), "Information Transmission Between India and International Commodities Futures Market: An Empirical Study for Bullion and Metals", Research in Applied Economics, Vol. 5, No. 4, pp. 149-175.

- Bollerslev T (1986), "Generalized Autoregressive Conditional Heteroskedasticity", Journal of Econometrics, Vol. 31, No. 3, pp. 307-327.

- Caporale G M, Ciferri D and Girardi A (2010), "Time-Varying Spot and Futures Oil Price Dynamics", CESifo Working Paper Monetary Policy and International Finance, No. 3015.

- Engle R F (1982), "Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation", Econometrica: Journal of the Econometric Society, pp. 987-1007.

- Fortenbery T R and Zapata H O (1997), "An Evaluation of Price Linkages Between Futures and Cash Markets for Cheddar Cheese", Journal of Futures Markets, Vol. 17, No. 3, pp. 279-301.

- Granger C W (1969), "Investigating Causal Relations by Econometric Models and Cross-Spectral Methods", Econometrica: Journal of the Econometric Society, pp. 424-438.

- Inani S K (2016), "Price Discovery in Indian Commodity Market", Int. J. of Business and Emerging Markets, Vol. 8, No. 4, pp. 361-382.

- Johansen S (1991), "Estimation and Hypothesis Testing of Cointegration Vectors in Gaussian Vector Autoregressive Models", Econometrica: Journal of the Econometric Society, pp. 1551-1580.

- Joshy K J and Ganesh L (2015), "An Empirical Analysis of Price Discovery in Spot and Futures Market of Gold in India", Pacific Business Review International, Vol. 7, No. 10, pp. 80-88.

- Koontz S R, Garcia P and Hudson M A (1990), "Dominant-Satellite Relationships Between Live Cattle Cash and Futures Markets", Journal of Futures Markets, Vol. 10, No. 2, pp. 123-136.

- Kumar B and Pandey A (2011), "International Linkages of the Indian Commodity Futures Markets", Modern Economy, Vol. 2, pp. 213-227.

- Lien D and Yang L (2009), "Intraday Return and Volatility Spill-Over Across International Copper Futures Markets", International Journal of Managerial Finance, Vol. 5, No. 1, pp. 135-149.

- Mahalik M K, Acharya D and Babu M S (2009), "Price Discovery and Volatility Spillovers in Futures and Spot Commodity Markets: Some Empirical Evidence from India", IGIDR Proceedings/Project Reports Series (062-10).

- McMillan D G and Speight A E (2001), "Non-Ferrous Metals Price Volatility: A Component Analysis", Resources Policy, Vol. 27, No. 3, pp. 199-207.

- Moosa I A (2002), "Price Discovery and Risk Transfer in the Crude Oil Futures Market: Some Structural Time Series Evidence", Economic Notes, Vol. 31, No. 1, pp. 155-165.

- Morales L (2008), "Volatility Spillovers on Precious Metals Markets: The Effects of the Asian Crisis", European Applied Business Research Conference (EABR), Salzburg, Austria, June 23-25.

- Nicolau M, Palomba G and Traini I (2013), "Are Futures Prices Influenced by Spot Prices or Vice-Versa?: An Analysis of Crude Oil, Natural Gas and Gold Markets", Vol. 394, Dipartimento di scienze economiche e sociali, Università politecnica delle Marche.

- Ryoo H J and Smith G (2004), "The Impact of Stock Index Futures on the Korean Stock Market", Applied Financial Economics, Vol. 14, No. 4, pp. 243-251.

- Saranya V P (2014), "Volatility and Price Discovery Process of Indian Spot and Futures Market for Non-Agricultural Commodities", International Journal in Management and Social Science, Vol. 3, No. 3, pp. 346-354.

- Schwarz T V and Szakmary A C (1994), "Price Discovery in Petroleum Markets: Arbitrage, Cointegration, and the Time Interval of Analysis", Journal of Futures Markets, Vol. 14, No. 2, pp. 147-167.

- Sehgal S, Rajput N and Deisting F (2013), "Price Discovery and Volatility Spillover: Evidence from Indian Commodity Markets", The International Journal of Business and Finance Research, Vol. 7, No. 3, pp. 57-75.

- Shakeel M and Purankar S (2014), "Price Discovery Mechanism of Spot and Futures Market in India: A Case of Selected Agri Commodities", International Research Journal of Business and Management, Vol. 8, No. 8, pp. 50-61.

- Sharma T (2015), "An Empirical Analysis of Commodity Future Market in India", International Journal of Engineering Technology, Management and Applied Sciences, Vol. 3, Special Issue, pp. 11-19.

- Shihabudheen M T and Padhi P (2010), "Price Discovery and Volatility Spillover Effect in Indian Commodity Market", Indian Journal of Agricultural Economics, Vol. 65, No. 1, pp. 101-117.

- Singh G (2015), "Role of Futures Market in Price Discovery: A Study of Indian Commodity Market", The Asian Economic Review, Vol. 57, No. 2, pp. 133-150.

- Sridhar L S and Sathish M (2011), "Price Discovery in Commodity Market: An Empirical Study on the Indian Gold Market", Sugyaan – Management Journal of Siva Sivani Institute of Management, Vol. 3, No. 1, pp. 19-29.

- Sridhar L S, Sumathy M, Sudha N and Charles Ambrose A (2016), "Price Discovery in Commodity Market: An Empirical Study on the Silver Market", Journal of Economics and Finance, Vol. 7, No. 2, pp. 88-95.

- Srinivasan P (2012), "Price Discovery and Volatility Spillovers in Indian Spot-Futures Commodity Market", The IUP Journal of Behavioral Finance, Vol. 9, No. 1, p. 70.

- Srinivasan K and Deo M (2009), "The Temporal Lead Lag and Causality Between Spot and Futures Markets: Evidence from Multi Commodity Exchange of India", International Review of Applied Financial Issues and Economics, Vol. 1, No. 1, pp. 74-82.

- Srinivasan P and Ibrahim P (2012), "Price Discovery and Asymmetric Volatility Spillovers in Indian Spot-Futures Gold Markets", International Journal of Economic Sciences and Applied Research, Vol. 5, No. 3, pp. 65-80.

- Taylor S (1986), Modeling Financial Time Series, Wiley and Sons, New York.

- Xu X E and Fung H G (2005), "Cross-Market Linkages Between US and Japanese Precious Metals Futures Trading", Journal of International Financial Markets, Institutions and Money, Vol. 15, No. 2, pp. 107-124.

- Zhong M, Darrat A F and Otero R (2004), "Price Discovery and Volatility Spillovers in Index Futures Markets: Some Evidence from Mexico", Journal of Banking and Finance, Vol. 28, No. 12, pp. 3037-3054.