Sep'18

The IUP Journal of Financial Risk Management

Archives

The Effect of Brexit on Indian Stock Market: An Empirical Study

E Madhavi

Associate Professor,

Department of Business Administration,

CMR College of Engineering and Technology,

Medchal Road, Hyderabad 501401, Telangana, India;

and is the corresponding author.

E-mail: emadhavi@cmrcet.org

N Rajender Reddy

Assistant Professor,

Department of Business Administration,

CMR College of Engineering and Technology,

Medchal Road, Hyderabad 501401, Telangana, India.

E-mail: rajender031@cmrcet.org

The effect of Brexit was hard on many economies. Emerging economies like India suffered hugely as many of its industries were greatly affected. Analysis of stock returns in such eventful scenarios helps us to take measures to mitigate the risks to a large extent with the help of forecasting for the safety of investors and businesses. The present event study analyzes the effect of Brexit on Indian stock market for pre-, during and post-Brexit periods. The data of Nifty 50 and seven sectoral indices returns were selected based on highly impacted sectors based on the correlation test done on all the sectors of Nifty. Autoregressive Conditional Heteroskedastic (ARCH) and Generalized Autoregressive Conditional Heteroskedastic (GARCH) models were used for the analysis, and the test results for the last four years (983 observations) indicate that there is significant impact of Brexit on Indian stock market.

Introduction

India is one of the most profitable markets in emerging economies for foreign investors and is attracting a lot of attention globally in recent days. Any major change across the globe would certainly impact Indian economy and the Indian stock market as it is more globalized. The millennial, different investor groups along with Indian businesses and financial institutions constantly gear up to reap the benefits of their investments with their active involvement in securities, commodities and bullion markets in both Indian and foreign exchanges on a daily basis.

Great Britain opted and existed out of European Union (EU) in June, 2016, which is named as Brexit. For Indian businesses, Great Britain is the doorway to the EU, which hosts many businesses across globe that avail the benefits of trade and financial services due to various bilateral agreements and negotiations between EU and other countries. With Brexit, this benefit will be taken away to an extent and may result in a few companies relocating their businesses elsewhere based on their marketing strategies, which in turn will affect their investments and businesses financially.

UK is 18th among India's top 25 trading partners and India's exports to the UK were to the tune of $5.3 bn in 2014-15.1 UK's exit from EU suddenly created global financial instability that rocked the global stock markets and took the world by surprise. Experts across the globe opined that this separation would haunt many economies for years to come. Like every other economy that suffered due to Brexit, India, an emerging economy too suffered. All industries, especially automobile, pharma, IT and energy, got directly hit, and NASSCOM predicted that the effect of Brexit on Indian IT sector would be to the tune of $108 bn in the short term. Indian IT companies may need to establish separate offices and hire different teams for the UK and the EU after the fallout, putting heavy expenditure burden on IT companies in the near term. The Indian bullion market too was greatly affected as Brexit forced many to sell their risky assets and rush towards safe investment options like gold. Gold prices in India breached 32,000 mark per 10-gram level.

On a positive note, in the longer run, Brexit could help strengthen India-UK economic relationship as the UK seeks to compensate for loss of preferential access to EU markets. Likewise, Indian businesses can benefit from European markets in the long run, but initially there would be a lot of financial burden on Indian companies as new offices are to be established at various strategic places throughout Europe.

When volatility is interpreted as uncertainty, it becomes the primary focus for many investment decisions and portfolio management as risk needs to be mitigated so as to bring very little or no effect on the investor's portfolio or investments. Without volatility superior returns cannot be earned, since a risk-free security offers meager returns. Understanding how volatility evolves with time is crucial for decision-making process in both investment and financial decisions for businesses and individuals alike. Too much volatility is a strong symptom of inefficient markets, and the higher the volatility, the higher is the risk. For a risk-averse investor, low volatility is preferred mostly as it decreases unnecessary risk of their investments. The portfolio and fund managers have to rightly balance these aspects to extract maximum returns for the portfolios they manage; else, they lose their high net worth clientele.

Event studies help us track the volatility of stock markets both for positive and negative effects in detail. Modeling such scenarios helps us to understand volatility's persistence and clustering around such an event. This one-time effect of Brexit has driven the researcher to do research on the event study to observe the volatility in Indian stock markets. In the past, modeling and forecasting of volatility was based on assumption that volatility is constant overtime. But with advancement and development in technology and R&D, the financial econometricians developed time-varying models to capture the most essential or vital facts about stock returns such as asymmetrical, symmetrical volatility, volatility clustering and leptokurtosis. Measuring volatility remains a big challenge, as markets are driven not only by the firm-level corporate changes but also by the global cues of coming events/news that happen around the world which may cast good or bad effects on stock prices.

In econometrics, Autoregressive Conditional Heteroskedastic (ARCH) and Generalized Autoregressive Conditional Heteroskedastic (GARCH) models were first introduced by Robert F Engle in 1982. Since then, these models have become important tools in the analysis of time series data, especially in financial applications and are very useful in research study to analyze and forecast volatility. Forecasts from these models can be applied in option pricing, hedging and portfolio selection to monitor if the event triggers a contagion or contraction in the markets.

Event studies help us to understand and analyze unique situations that happen not only in domestic market but also globally causing effect or ripple effects on our stock market. The review of literature gives us hints on how markets perform during such volatile and unstable situations. Though there are many theories and assumptions for such scenarios, this one-time effect of Brexit is a good event study due to its uniqueness, due to which global markets tumbled and a lot of financial instability was felt across the world and still remains an unresolved or disputed situation. Such an event had caused a great impact on Indian economy too and hence it is apt to study the areas (sectors/industries) that took major hit. Such a study gives us an idea about those sectors that escaped unscathed. The present study aims to model and estimate daily volatility of stock returns of seven sectoral indices listed on National Stock Exchange of India Limited (NSE) with respect to CNX Nifty with data taken from pre- during and post-Brexit for understanding the majorly hit sectors with evidence from this event.

Literature Review

Modeling the stock market volatility both in developing and emerging economies has become primary importance for financial and asset management institutions. Many researchers investigated the performance of ARCH and GARCH models to explain volatility in stocks, derivatives, commodities, bullion and indices from its invention and conception across the global economies. The literature quoted here is mainly for referential purpose in studying the event, especially using econometric models given to us by the respective original contributors/researchers which served better than the long previously existing methods such as averages, moving averages, etc. Later on, research works done by other researchers in such event studies are given and updated.

Engle (1982) published a paper introducing a new class of stochastic processes named ARCH processes in order to estimate the means and variances of inflation in UK. Traditional econometric models has been assuming a constant one-period forecast variances till then. ARCH processes have zero mean and are serially uncorrelated processes with non-constant variances conditional on past but constant unconditional variances. A regression model was introduced with disturbances, following an ARCH process, using maximum likelihood estimators, and described with a simple scoring iteration formulation. To test if disturbances follow ARCH process, Engle employed Lagrange multiplier procedure based on autocorrelation of squared OLS residuals. He found the results from ARCH effect to be significant and estimated variances that substantially increased during chaotic times in the early 1970s.

Bollerslev (1986) introduced GARCH (1, 1) model to overcome the limitations of ARCH model which was based on past sample variance. GARCH model also uses a weighted average of past squared residuals but it has declining weights which never go completely to zero. It gives us parsimonious models which are easy to estimate and even in its simplest form, has proven surprisingly successful in predicting conditional variances introducing lagged conditional variances. He concludes that the most widely used GARCH specification asserts that the best predictor of the variance in the next period is a weighted average of the long-run average variance, the variance predicted for this period and the new information of this period would be the most recent squared residual. Such an updating rule is a simple description of adaptive or learning behavior and can be thought of as Bayesian updating.

Nelson (1991) extended the ARCH model's framework and, as an improvement over GARCH model, named it as EARCH (Exponential ARCH) to describe the behavior of return volatilities. He concluded that EARCH model allows the same degree of simplicity and flexibility in representing conditional variances as ARIMA models allowed in representing conditional means. With this EARCH (q, p) model, Nelson corrected the three drawbacks of GARCH model—(1) allowing correlation between returns and volatility, an important feature of stock market change, (2) eliminating the need for imposing parameter restrictions, and (3) allowing direct interpretation of 'persistence' shocks to volatility. Nelson opined that further research should be done in extending his EARCH model to fit multivariate version for a satisfactory study of asymptotic distribution of maximum likelihood parameter estimates.

Glosten et al. (1993) in their study introduced GJR (TARCH) model to adjust the primary restrictions of GARCH-M which enforce a symmetric response of volatility to positive and negative shocks. They concluded that there is a positive but significant relation between the conditional mean and conditional volatility of the excess return on stocks when the standard GARCH-M framework is used to model the stochastic volatility of stock returns.

Engle and Ng (1993) made a study on news impact curves which measure how new information is incorporated into volatility estimates. They tested various existing ARCH models and estimated a nonparametric model using daily Japanese stock return data. They introduced new diagnostic tests and concluded from their test results GJR (TARCH) model, given by Glosten, Jagannathan and Runkle, to be the best parametric model and also opined that though EGARCH model captures most of the asymmetry in volatility due to news, the variability of conditional variance from it is too high.

Batra (2004) in his paper examined the time-varying pattern of stock return volatility in India over the period 1979-2003 using monthly stock returns and asymmetric GARCH methodology. He examined the sudden shifts in volatility and the possibility of coincidence of these sudden shifts with significant economic and political events both of domestic and global origin. He then analyzed stock market cycles for variation in amplitude, duration and volatility of the bull and bear phases over the reference period which shows bull phases to be longer, amplitude of bull phases to be higher and the volatility in bull phases also to be higher. The gains during expansions are larger than the losses during the bear phases of the stock market cycles. The bull phase is more stable in the post-liberalization phase as compared to its pre-liberalization character. The results of his analysis showed that the stock market cycles have reduced in the recent past and volatility has declined in the post-liberalization phase for both the bull and bear phases of the stock market cycle.

Banerjee and Sarkar (2006) in their paper attempted to model the volatility in the daily return of NSE using high frequency intra-day data covering a period from June 2000 through January 2004. They showed that the Indian stock market experiences volatility clustering and hence concluded that GARCH-type models predict the market volatility better than simple volatility models, like historical average, moving average, etc., and also observed that the asymmetric GARCH models provide better fit than the symmetric GARCH model, confirming the presence of leverage effect. Their test results showed that the change in volume of trade in the market directly affects the volatility of asset returns and the presence of Foreign Institutional Investors (FII) in the Indian stock market does not increase the overall market volatility.

Goudarzi and Ramanarayanan (2010) examined the effects of good and bad news on volatility in the Indian stock markets using asymmetric ARCH models during the global financial crisis of 2008-09. They used BSE 500 stock index as a proxy to the Indian stock market to study the asymmetric volatility over 10-year period. The two commonly used asymmetric volatility models, i.e., EGARCH and TGARCH models, were used in their study. They found that BSE 500 returns series reacted both to the good and bad news asymmetrically. The leverage effect, which was present and observed by them, would only conclude that the negative innovation (news) has a greater impact on volatility than positive innovation (news). This stylized fact observed by them only indicates that the sign of the innovation has a significant influence on the volatility of returns and the arrival of bad news in the market would result in the volatility to increase more than good news. Therefore, they concluded that the bad news in the Indian stock market increases volatility more than good news.

Emenike and Aleke (2012) in their paper examined the volatility of stock market to negative and positive news using daily closing prices of the Nigerian Stock Exchange. By applying EGARCH (1, 1) and GJR stock return series from January 1996 to December 2011, they found evidence to support asymmetric effects in the Nigerian stock market returns but with no leverage effect. However, the estimates from EGARCH model showed positive and significant asymmetric volatility coefficient. Likewise, the test results from the GJR-GARCH model showed negative and significant asymmetric volatility coefficient supporting the existence of positive asymmetric volatility. On the whole, they observed that their stock market returns showed higher and more volatility in near future for positive news as compared to the effect of negative news with same magnitude.

Shveta and Anita (2014) empirically examined the relationship between the crisis and stock returns volatility in the Indian banking sector using CNX Bank stock index as a proxy to stock prices of Indian commercial banks. They collected the time series data of closing stock prices for nine years and used GARCH model to capture the impact of crisis on stock volatility of banks. The results of their study revealed a high persistence of volatility and significant negative association between stock returns and their volatility during both sub-periods of crisis. They concluded that the crisis has a significant impact on the stock volatility of the Indian banking sector and that stock returns volatility has significantly changed during the pre- and post-crisis periods.

Saurabh and Tripathi (2016) empirically investigated the volatility pattern of Indian stock market based on the 15-year time series data from April 2001 to March 2016 using both symmetric and asymmetric models of GARCH and found these models to be apt as per Akaike Information Criterion (AIC), Schwarz Information Criterion (SIC) and log likelihood ratios. Their study also provided evidence for the existence of a positive and insignificant risk premium as per GARCH-M (1, 1) model. The asymmetric leverage effect captured by the parameter of EGARCH (1, 1) and TGARCH (1, 1) models showed that negative shocks have a significant effect on conditional variance (volatility).

Objective

The present study aims to analyze the volatility caused due to Brexit on stock returns of various sectors listed on Indian NSE.

Data and Methodology

The research was done using secondary data relating to closing prices of CNX Nifty index along with seven other sectoral indices such as CNX Bank, CNX IT, CNX FMCG, CNX Auto, CNX Energy, CNX Metal and CNX Pharma. The data of these sectors were extracted from the NSE and returns for each sector were calculated and used. Each of these sectoral/thematic indices covers top 10 companies of India, which are computed on free-float market capitalization method by NSE. The stock returns used in the current study are not the actual closing prices of various sectoral indices but they are the log normal values consisting of 983 daily observations for data pertaining to pre-, during and post-Brexit starting from June 1, 2014 to May 26, 2018.

The CNX Nifty return was taken as dependent variable and seven sectoral indices returns were taken as independent variables. These seven sectors' data were chosen based on the correlation test done on all sectors of Nifty. The returns from these eight indices were analyzed using GARCH (1, 1) model for forecasting volatility caused due to Brexit.

Results and Discussion

The regression tests and tests of heteroskedasticity were run using GARCH (1, 1) model to test serial correlation, ARCH effects and histogram normality test on all the three distributions—normal, Student's t and Generalized Error Distributions (GED). It is found that normal distribution is more relevant to the current study out of the three distributions based on various criteria and hence the test results of the same are discussed in detail.

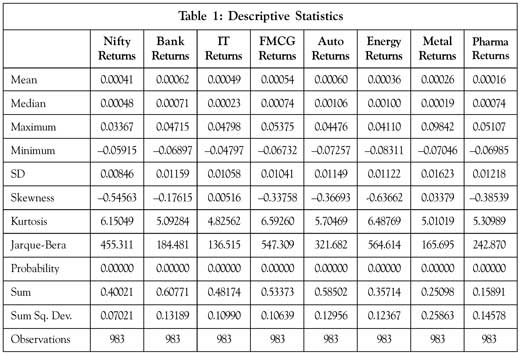

The average Nifty returns in this sample is 0.00041 with CNX Pharma having lowest mean value (0.00016), followed by CNX Metal (0.00026) reflecting that these two are most affected in this study period and CNX FMCG has least standard deviation (0.0104) after Nifty returns (Table 1). For CNX Bank and CNX Auto returns, the mean value is highest (0.00062, 0.00060) and CNX Metal returns has highest standard deviation (0.01623). Though the kurtosis values all reflect positive kurtosis, it can be observed that for all sectors the values are not normally distributed, showing 'peakedness' (univariate normal distribution

value is 3), meaning there exists volatility and it is not normal. Variance measures how spread out the data are about their mean and as can be observed from Table 1 there is not much spread of data from mean.

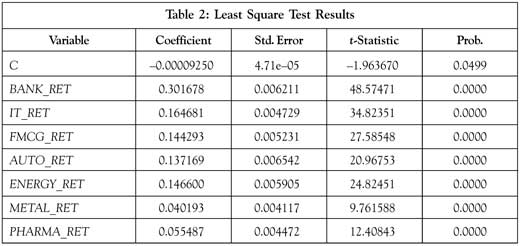

Table 2 presents the p-values from least squares equation. As can be observed, the model is very significant at 99.9% and holds goodness-of-fit. Thus, the experiment is continued using both the variables—stock returns of CNX Nifty and individual returns of seven sectoral indices.

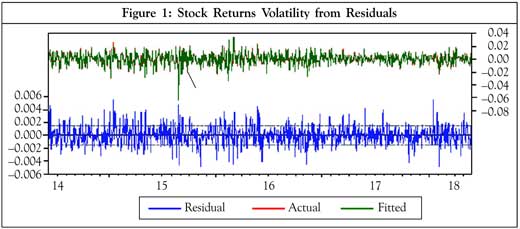

The residuals from the estimation of least squares equation showed in Table 2 is graphically presented as Figure 1 which reflects the volatility of all stock returns with respect to each

other. From the top portion of the graph, we can observe that the actual and fitted values (depicted in green and red lines) are not distinguishable, i.e., almost same.

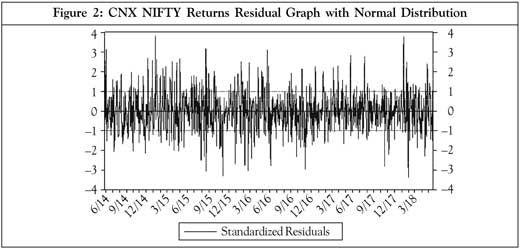

In Figure 2, the volatility of CNX Nifty residuals can be observed in detail. During the period ranging from June 2015 to May 2016, we see heavy volatility and clustering which results from mere fear of uncertainty about the upcoming Brexit in trading circles proving that markets respond to rumors which create panic situation among investors either to sell

stocks thus offloading their positions in order to mitigate the risk of loss due to uncertainty for negative news (which is the case in this study) and buy heavily for positive news.

We see a negative spike during the period ranging from June 2015 to June 2016 in trading volume as the stock prices fell more than expected to gain from the situation by holding the positions. Once the actual Brexit announcement was made on June 26, 2016, which is June (6/16) in Figure 2, volatility clustering is observed for a few days.

Likewise, for the period ranging from September 2016 to September 2017, India experienced the effect of demonetization and again we see comparatively bold spike down in Nifty mainly due to cash crunch experienced by both individuals and investors due to tightening of free cash in the market by various measures taken up by the Government of India as an after-effect of demonetization. Thus, it can be concluded that all such news and events pertaining to government, financial and commodities impact the markets on daily basis, causing small to big volatility shocks in the stock returns of various scrips of the industries which is reflected in respective indices.

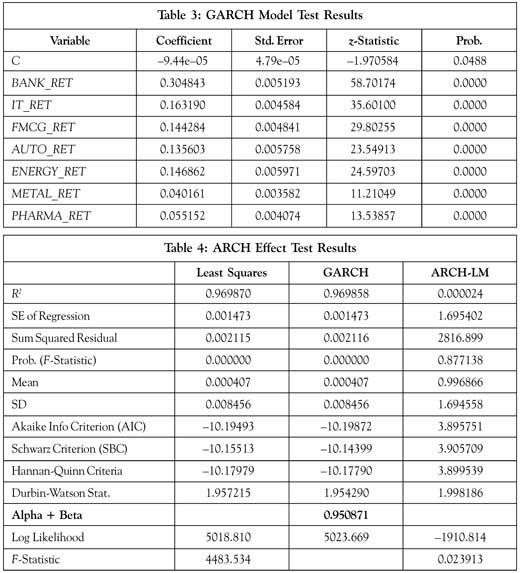

Table 3 gives the GARCH (1, 1) model estimation results for the variables. It is observed from Table 4 that the alpha and beta values are close to 1, indicating that the volatility shocks are quite persistent. The p-values of both the residual and GARCH in variance equation are highly significant at 95%, substantial enough to explain the volatility of CNX Nifty and other seven sectoral indices returns. The Durbin-Watson value tells us

upfront that there is no autocorrelation between the variables and thus the model holds good (Table 4).

The p-value from Ljung-Box test with 26 lags is greater than 95% significance, implying that the null hypothesis cannot be rejected in this scenario. Thus, we accept the data as independently distributed, meaning that there is no serial correlation of the data used in the study. Table 4 gives us the test results of ARCH Lagrange Multiplier (LM) test to check residuals or error terms. Here, we observe that the p-value is significant at 95%, suggesting

that the null hypothesis of this test cannot be rejected. Hence, we accept the null hypothesis that there is no ARCH effect in the remaining variance equation, meaning the squared residuals of the model exhibit no further autocorrelation.

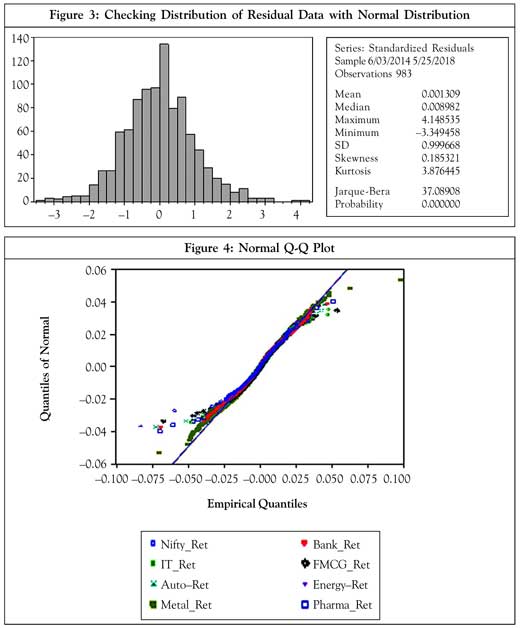

Figure 3 shows the histogram normality test results. It is observed that the p-value is significant, i.e., it is equal and less than 95%, reflecting that the null hypothesis can be rejected, concluding that the residuals are not normally distributed.

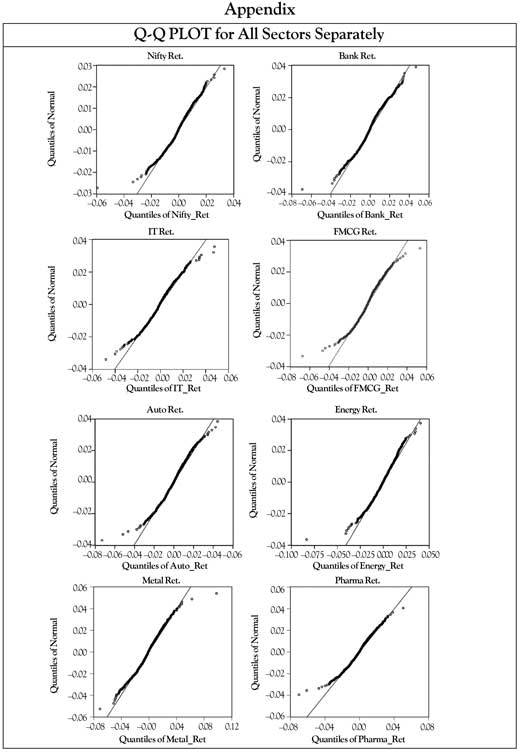

However, from normal Q-Q plot (Figure 4 and the Appendix), we can see that the residuals are normally distributed, and hence for this study this can be considered instead of p-values from the histogram normality test.

Thus, with these results, it can be observed that GARCH (1, 1) model proves to be useful for predicting and forecasting the stock volatility which arises due to both positive and negative news and that the model taken for the current study holds good to showcase the same.

Conclusion

This study analyzed the Brexit effect on Indian stock market as an event study, for which ARCH and GARCH models were used to study the volatility of CNX NIFTY returns along with seven sectoral indices returns. From previous literature, it is observed that financial market volatility is forecastable and hence this event study was taken up. The results from this study were examined for the evidence of volatility due to Brexit along with volatility clustering and persistence in the market returns, which is mainly caused due to the uncertainty created because of pessimism or lack of knowledge of upcoming global news which is going to be announced in future.

The uncertainty due to Brexit triggered panic amongst the day investors, traders, brokers and speculators, thus leading to many offloading their portfolios to mitigate risk to little for fear of eventual loss in their investments or its returns. As observed from the results and volatility graph (Figure 2), once the announcement of Brexit was made, thereon the stock volatility was relatively calm with only slight volatility clustering. Overall, the results from this study provide strong evidence that both positive and negative news have higher effect on volatility of stock markets and it is good to have event studies in place to record and monitor these effects for the benefit of public at large (bankers, industrialists, investors, FIIs, research community and traders). Modeling volatility helps in forecasting and predicting the nature of its effect on stock returns and helps to create fall-back strategies to mitigate risk to a large extent.

Limitations: This study is limited to an event, i.e., to study the effect of Brexit on Indian stock market. During the same period of this study, i.e., 2014-2018 India witnessed much of financial turmoil due to various factors that started incidentally with Brexit followed by demonetization, fall in rupee, increase in interest rates to curb inflation, etc. An event study for a period of 5-month before and after Brexit would not be sufficient to capture and justify the volatility stock markets experienced due to the event. Accordingly, though a broader time spectrum was taken in this study, the main 10-month period was only discussed in detail (refer Figure 2) to emphasize on Brexit and the impact it had on Indian stock market and any discussion beyond this period would not become a part of this study.v

References

- Banerjee A and Sarkar S (2006), "Modelling Daily Volatility of the Indian Stock Market Using Intraday Data", Working Paper No. 588. Retrieved from http://www.iimcal.ac.in/res/upd%5CWPS%20588.pdf

- Batra A (2004), "Stock Return Volatility Patterns in India", Working Paper No. 124. Retrieved from http://www.icrier.org/pdf/wp124.pdf

- Bollerslev Tim (1986), "Generalized Autoregressive Conditional Heteroskedasticity", Journal of Econometrics, Vol. 31, No. 3, pp. 307-327.

- Emenike Kalu O and Aleke Stephen Friday (2012), "Modelling Asymmetric Volatility in the Nigerian Stock Exchange", European Journal of Business and Management, Vol. 4, No. 12, pp. 52-59.

- Engle R and Patton A (2001), "What Good is a Volatility Model?", Quantitative Finance, Vol. 1, No. 2, pp. 237-245.

- Engle F (1982), "Autoregressive Conditional Heteroscedasticity with Estimates of the Variance of United Kingdom Inflation", Econometrica, Vol. 50, No. 4, pp. 987-1007.

- Engle F and Ng Victor K (1993), "Measuring and Testing the Impact of News on Volatility", Journal of Finance, Vol. 48, No. 5, pp. 1749-1778.

- Glosten Lawrence R, Ravi Jagannathan and Runkle David E (1993), "On the Relation Between the Expected Value and the Volatility of the Nominal Excess Return on Stocks", Journal of Finance, Vol. 48, No. 5, pp. 1779-1801.

- Goudarzi H and Ramanarayanan C S (2010), "Modelling and Estimation of Volatility in Indian Stock Market", International Journal of Business and Management, Vol. 5, No. 2, pp. 85-98.

- Nelson Daniel B (1991), "Conditional Heteroskedasticity in Asset Returns: A New Approach", Econometrica, Vol. 59, No. 2, pp. 347-370.

- Saurabh Singh and Tripathi L K (2016), "Modelling Stock Market Return Volatility: Evidence from India", Research Journal of Finance and Accounting, Vol. 7, No. 13, pp. 93-101.

- Ser-Hung Poon and Clive E W J Granger (2003), "Forecasting Volatility in Financial Markets: A Review", Journal of Economic Literature, Vol. XLI, June, pp. 478-539.

- Shveta Singh and Anita Makkar (2014), "Relationship Between Crisis and Stock Volatility: Evidence from Indian Banking Sector", The IUP Journal of Applied Finance, Vol. 20, No. 2, pp. 75-83.