Sep'18

The IUP Journal of Financial Risk Management

Archives

The Impact of Basel III Norms on Profitability: An Empirical Study of Indian Public Sector Banks

Krishan K Boora

Assistant Professor,

Department of Management Studies,

BPS Women University,

Sonepat 131305, Haryana, India;

and is the corresponding author.

E-mail: krishanboora@gmail.com

Kavita

Research Scholar,

Department of Management Studies,

BPS Women University,

Sonepat 131305, Haryana, India.

E-mail: kavitajangra384@gmail.com

With the deteriorating asset quality and financial health of banking institutions and the recent upsurge of bank failures due to global financial crisis, it is vindicated that bank profitability needs an increased investigation from industry analysts and scholars. The recent global financial crisis contemplated the significance of banks' profitability for the stability of economy as well as banking sector, reflecting the need to maintain it under surveillance all the time. Poor financial performance of banks has negative repercussion on economy which can lead to economic failures and crises. Banking crisis can lead to financial crisis which in turn leads to economic crisis. That is why Basel III norms have emerged as stringent regulations to foster a healthy and sound banking system. Banks all over the world are facing several problems in implementing Basel III norms due to lack of adequate funds, increasing NPAs, pressure on Return on Assets (ROA) and Return on Equity (ROE). It is possible that Indian public sector banks have been undergoing pressure after implementing the capital regulations. Hence, the present study intends to examine the financial performance of Indian public sector banks and investigate the impact of Basel III on profitability of banks. The study uses ROA and ROE as profitability indicators of 21 Indian public sector banks for a period of 10 years (2007-2017). Conclusively, the study can be useful for bankers, decision makers and particularly for the investors looking for profitable opportunities in Indian banking sector.

Introduction

The financial resilience of banking sector always remains a major concern. A sound banking system is that system which enjoys efficiency in operations, strong liquidity position and continuous path of profitable avenues. All these factors enable banks to survive in dynamic environment and walk in line with the market changes. Public sector banks are dominant players that play a significant role in Indian economy. In the wake of severe financial crises and frauds plaguing the Indian banking sector, the analysis of profitability of banks is essential because higher profitability and sound financial performance of banks are the keys to absorbing the unexpected consequences and losses arising on account of crisis.

The severe crisis in East Asia and in the US has also underlined the need for a stable financial system. The proper compliance of banking reforms determines the stability of financial sector. The banks have been regulated by enacting laws and some regulations from time to time. In this regard, Basel III as a global regulatory framework was released in December, 2010 for making banks and banking system more resilient. The Basel III norms intend to increase the quality and quantity of capital maintained by banks as good quality of capital would make banking sector more efficient and stronger. Basel III comprises two sets of reforms: global capital and liquidity which would ensure long-term stability in banking sector. Moreover, Basel III standards are expected to amend the potentiality of banks to absorb the losses incurred due to economic and financial crises. Basel III norms would bring about a revolutionary change in the Indian banking industry. The implementation of these norms will make Indian banks stable and less susceptible to risk and crisis. The financial soundness of banks can be improved by the proper implementation of Basel III. Thus, implementation of Basel III is highly important for the Indian public sector banks and better implementation of these norms will allow banks to acquire the benefits of endless opportunities.

While implementing Basel III, banks will surely face several challenges such as decline in profitability, requirement of additional funds, higher cost of implementation and burden on lending practices. In this case, financial health of bank is of prime importance because of stability of banking industry. Implementation of Basel III capital regulations will make an impact on the financial performance of Indian banks. To survive in the environment of regulatory pressure is the biggest challenge for Indian banks.

It is necessary to check the financial status of Indian public sector banks. It is possible that Indian public sector banks are undergoing a pressure after implementing capital regulations. As we know, the capital regulations under Basel III are stringent and need additional funds to comply, therefore banks will face difficulty in obtaining funds to comply with Basel III. The increasing borrowing cost may create bankruptcy if banks do not have sufficient profits. All these issues will directly affect the financial performance of banks, resulting in decline in profitability and operating efficiency. On the other hand, public sector banks in India possess higher government stake; so, no more options are available to raise funds. The decreasing asset quality, declining profitability, (Return on Assets, ROA and Return on Equity, ROE), increasing Non-Performing Assets (NPAs) and poor performance of public banks indicate the chances of bankruptcy. Under these circumstances, the moot question is how public sector banks will survive for long as they have more chances to become insolvent.

Implementing Basel III norms can be a financial burden for banks. The high cost to meet capital norms and cost to borrow funds may decline the profitability; and other reasons are heavy investment cost in upgrading technology and validating credit rating models. Therefore, implementing Basel III can be a financial burden for small banks because weaker banks have to raise overall capital due to low profits, and immediate stress on banks may lead to close down of their operations. There can be negative impact of implementing Basel III on bank lending and interest rate because banks have to increase interest rate due to increase in external borrowings. Thus, keeping the above issues in mind, it is desirable to check the financial position of banks and identify those banks which are operating under stress due to the pressure of maintaining high Capital Adequacy Ratio (CAR). To maintain the level of CAR, banks are facing the problem of low profitability. The present study attempts to find out the financially sound banks that will contribute positively and the financially weaker banks facing negative impact of Basel III.

The analysis of profitability is essential to know the financial status of banks. The financial analysis predicts the financial health of banks which determines the financial soundness. After the introduction of Basel III capital regulations, banks all over the world are facing several problems in Basel III implementation due to lack of adequate funds, increasing NPAs, and pressure on ROA and ROE. Moreover, the financial health of banks plays a significant role in implementing financial regulations as poor financial performance of banks may lead to bankruptcy.

The present study seeks to provide the answers of the following questions: Is implementing Basel III capital regulation positively affecting the profitability of banks? What kind of change (positive/negative) has been observed in the financial performance of banks after implementation of Basel III capital regulations? Is the performance of Indian banks influenced by Basel III?

Literature Review

The measurement of banks' profitability is well-researched and has gained increased attention over the past few years. Kalhoefer and Salem (2008) analyzed the profitability and financial performance of Egyptian banks. The study reported problems in banks' profitability and showed structural weaknesses in both public and private banks. The authors suggested that higher interest rate can increase the revenue and lead to higher profitability.

Kumbirai and Webb (2010) explored the performance of South African banking sector for the period 2005-2009. The results showed significant change in the profitability of banks due to the global financial crisis in 2007. This led to decline in profitability, low liquidity and decreasing asset quality of banks in South Africa.

Alper and Anbar (2011) investigated the determinants of banks' profitability in Turkey for the period 2002-2010. The findings revealed that size of assets and non-interest income had positive and significant impact on profitability of banks, whereas the size of loan had negative impact on profitability. Interest rate affects the profitability of banks positively. The authors suggested that profitability of banks can be improved by increasing the non-interest income and decreasing credit-asset ratio.

Brindadevi (2013) analyzed the profitability of Indian private sector banks by using financial indicators such as interest spread, net profit margin, return on long-term fund, return on net worth and return on asset. The author recommended that measurement of profitability is the most significant measure of success of banking business. A profitable banking business is capable of rewarding its owners with higher return.

Roman and Danuletiu (2013) investigated the factors that affect the profitability of banks in Romania over the period 2003-2011. The results showed that bank-specific variables and external environment are the significant factors which influenced the banks' profitability. The authors concluded that asset quality, banking liquidity and management quality significantly influence profitability. The study suggested that banks should change their specific operations to improve profitability.

Adam (2014) measured the financial performance of Erbil Bank in Iraq for the period 2009-2013. The author used several financial indicators to measure the financial position of bank. The study found that the overall performance of Erbil Bank was satisfactory and improving in terms of asset quality and profitability ratio. The author recommended development of some specific banking operations which can boost the bank's performance and improve its profitability.

Islam (2014) attempted to examine the financial performance of National Bank Limited Bangladesh for the period 2008-2013 and identified the differences in performance of banks over two periods (2008-2010 and 2011-2013). The author concluded that the performance of banks depends on the ability of top management in preparing strategic plans and the proper implementation of its strategies. The study suggested specific areas for banks to work on that can improve their performance and ensure sustainable growth.

Titko et al. (2015) explored the drivers of bank profitability in Latvia and Lithuania over the period 2008-2014. The performance of banks was measured by using financial and non-financial indicators. The authors concluded that profitability is driven by asset quality, efficient management and sound banking operations.

Mensah and Fred (2015) measured the profitability of banks in Ghana over the period 2006-2011. The study used ROA and size of firm as dependent variable, and leverage ratio, credit risk ratio, profitability ratio, and liquidity ratio as independent variables. The findings revealed that 60.74% of the variation in the profitability of the banks was explained by the independent variables such as the liquidity level, leverage and credit risk.

Menicucci and Paolucci (2016) explored the relationship between bank-specific factors and profitability in European banking sector covering 28 European banks for the period 2006-2015. The study showed that CAR and bank size have positive impact on bank profitability and banks with higher deposit ratio tend to be more profitable. The authors suggested that special attention should be given to bank-specific factors in order to boost the profitability.

Mehta and Bhavani (2017) measured the impact of specific variables on profitability of banks in UAE. The study was conducted on 19 banks for a period of eight years (2006-2013). The results indicated that maintaining a high CAR and improving asset quality are the variables that directly impact the profitability of banks. The authors concluded that profitability of banks can be increased by engaging in non-traditional sources of revenue. Apart from that, the authors recommended a profitability-enhancing model which can be used by banks to enhance their performance.

Hallunovi (2017) explored the factors that affect the profitability of banks in Albania. A survey was conducted on banks in Albania for the period 2009-2014. The results of the study demonstrated the positive relationship between bank size and profitability that is statistically significant at 1% level of significance. The study concluded that credit risk has negative relation with profitability, whereas inflation and exchange rate have positive relation with profitability (ROA/ROE).

Nuhiu et al. (2017) attempted to measure the determinants of profitability of banks which affect the financial performance of commercial banks in Kosovo. The authors used various financial indicators such as Return on Average Equity (ROAE), Return on Average Assets (ROAA) and Net Interest Margin (NIM). The study concluded that internal factors such as asset quality, capital adequacy and management efficiency affect the profitability of banks in Kosovo.

Islam and Hasan (2017) attempted to investigate the determinants of profitability of 15 private banks in Bangladesh for the period 2005-2015. The study focused on the internal factors that affected bank profitability. The results depicted that non-performing loan and operating expenses had significant impact on banks' profitability because higher non-performing loans lead to less profit. The authors concluded that high non-performing loans are a threat to profitability of banks.

Maiti and Jana (2017) attempted to identify the determinants of performance of Indian banks including nationalized banks, State Bank of India and its associates, new private sector banks, old private sector banks and foreign banks. The study explored the impact of various internal factors on profitability. The findings showed that NIM, non-interest income and non-performing assets significantly influence the level of profitability. The authors concluded that banks should frame suitable policies to improve the revenue generating activities and banks need to balance the non-interest income.

Kumar and Kavita (2017) explained that banks which have sound financial position, can easily implement the new regulations, but it is difficult for the financially weaker banks to determine the required capital as per the international norms. Thus, financial analysis has become the need of the hour for the banking sector to identify its financial position. In this context, evaluating the financial health of Indian bank has become compulsory to compete with the environmental changes. The study concluded that the financial position of banking sector has always been a concern for both the bankers and stakeholders because unsound financial position can lead to bankruptcy.

Hayat et al. (2017) showed that banks in Indonesia have been undergoing major challenges in the regulatory environment. The study developed a performance model to resist negative shock and maintain financial stability of banking system. The findings showed that measurement of profitability is crucial in assessing the financial health of banking institutions.

Mohamed and Soliman (2017) aimed to determine the impact of Basel III on the Egyptian banks. The study explored the impact of Basel III on small and large size banks, and low and high capitalized banks. The authors concluded that Basel III has negative impact on small banks and banks with low capital base as these weak banks are unable to comply with stringent regulations due to lack of funds and low profitability.

Rekik and Kalai (2018) analyzed the determinants of profitability in conventional banks in Tunisia as well as 13 different countries. The study covered the data from 110 banks over the period 1999-2012. The findings showed that cost efficiency does not have more impact on profitability than profit efficiency. It was concluded that profitability of banks is a significant factor as the soundness of banking institutions is directly related to the soundness of the entire economy.

Makkar and Hardeep (2018) attempted to measure the profitability of banks and identified the key factors which influence the profitability of 46 Indian commercial banks over the period of 15 years (2001-2016). Profitability of banks has been measured through ROA and some of other variables like liquid assets to total assets, current ratio, CAR, and non-performing assets to total assets were used to identify the key factors which impact the profitability of Indian banks. The findings revealed that liquidity, solvency and efficiency are the significant factors that influence the profitability of Indian commercial banks. The authors concluded that profitability of public sector banks is satisfactory as compared to the profitability of private sector banks. Moreover, the authors suggested that the banks with low ROA should focus on improving their financial performance to boost their level of profitability to comply with Basel norms.

Data and Methodology

The present study evaluates the profitability of Indian public sector banks and examines the impact of implementing Basel III capital norms on profitability of banks. The financial performance of Indian public sector banks has been evaluated by using profitability indicators: ROA and ROE.

ROA shows the percentage of how profitable a company's assets are in generating revenue. It gives an indication of the capital intensity of the company; companies that require large initial investments will generally have lower ROA. ROA over 5% is generally considered good. ROA is a profitability ratio which indicates the net profit (net income) generated on total assets. It is computed by dividing net income by average total assets.

ROA = (Profit after tax/Total assets) *100

In other words, ROA shows how effective is the management of the company in generating income from utilizing all the assets at their disposal. It is a useful ratio to evaluate the performance of different departments of a company as well as to understand management performance over time. It measures the overall efficiency of a company in generating profits from its total assets. A low ROA indicates that a bank is asset-intensive and it would need more funds to continue its operations.

ROE is a ratio relating net profit (net income) to shareholders' equity. The equity refers to share capital reserves and surplus of bank.

ROE = Profit after tax/Total equity

ROE is the significant indicator of measuring the financial health of banks. ROE from 10-20% and above is generally considered good and shows higher profitability.

In order to examine the profitability of banks, ROA and ROE of 21 public sector banks have been selected for a period of 10 years from 2007 to 2017. The study is based on secondary data collected from the annual reports of the banks. In order to analyze the impact of implementing Basel III capital regulations on the profitability of banks, descriptive and analytical approaches have been used. The analysis is carried out through descriptive statistics, histogram, chart and graphs. Further, the study uses ANOVA for testing the hypotheses. The analysis is done using MS-Excel.

Results and Discussion

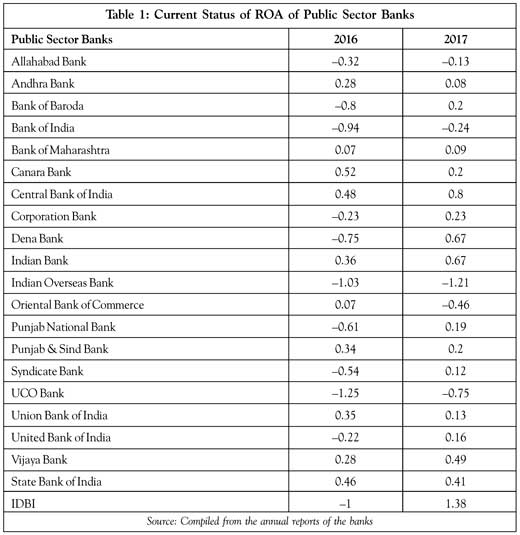

Table 1 shows that the ROA of most of the public sector banks was observed to be negative in 2016. These banks were Allahabad Bank, Bank of Baroda, Bank of India, Corporation Bank, Dena Bank, Indian Overseas Bank, Punjab National Bank, Syndicate Bank, UCO Bank, IDBI and United Bank.

A slight increase has been observed in ROA of Bank of Baroda, Bank of Maharashtra, Central Bank, Corporation Bank, Dena Bank, Indian Bank, Punjab National Bank, Syndicate Bank, United Bank, Vijaya Bank, and IDBI in 2017. Five public sector banks, namely, Allahabad Bank, Bank of India, Indian Overseas Bank, Oriental Bank of Commerce and UCO Bank, attained negative ROA even in 2017.

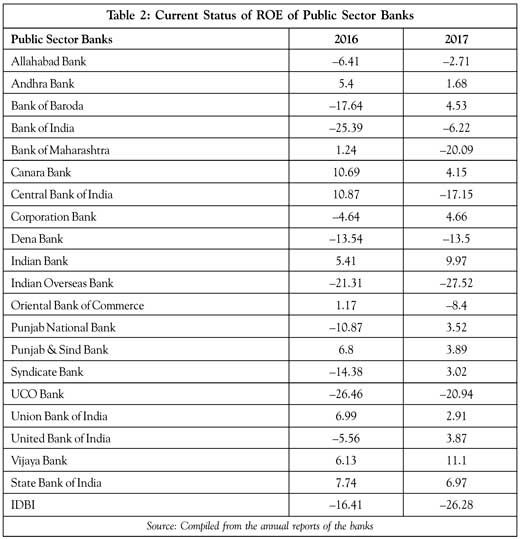

Table 2 shows the ROE of public sector banks. In 2017, Vijaya Bank recorded the highest ROE (11.1), followed by Indian Bank (9.97) and State Bank of India (6.97). The lowest ROE was recorded by Indian Overseas Bank (–27.52), followed by IDBI (–26.28) and UCO Bank (–20.94).

In 2017, nine banks, namely, Allahabad Bank, Bank of India, Bank of Maharashtra, Central Bank of India, Dena Bank, Indian Overseas Bank, Oriental Bank of Commerce, UCO Bank and IDBI, showed negative ROE (Table 2). Out of 21 public sector banks, seven Indian public sector banks, namely, Vijaya Bank, Syndicate Bank, Indian Bank, Bank of Baroda, Punjab National Bank, United Bank of India and Corporation Bank, were observed with positive and little rise in ROE, while 14 banks were found with negative and rapid decline in ROE.

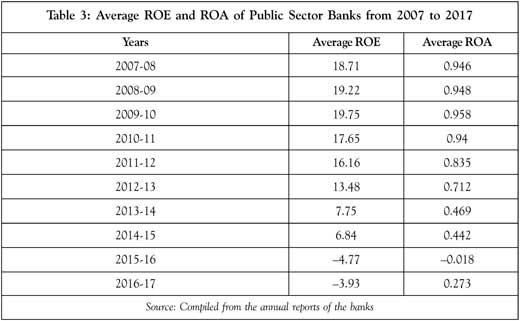

Table 3 presents the average ROE of all public sector banks for a period of 10 years. It is observed that after 2010, ROE showed a decreasing trend till 2017. ROE of all public sector banks reached a very worst stage as it touched the negative level. Before 2013, ROE was at a good level, but later it continued to decline sharply.

Between 2007 and 2010, banks earned ROA of 0.946, 0.948 and 0.958 which is higher than the other years. Banks performed most effectively in 2010. Between 2011 and 2017, downward trend in ROA was observed which indicates that banks were not performing at satisfactory level. Moreover, there was a sharp decline in ROA and ROE of public sector banks and banks earned negative ROA in 2016 and negative ROE in 2016 and 2017.

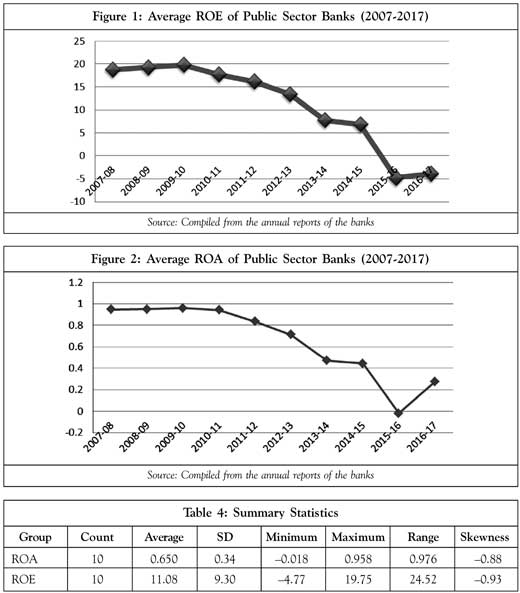

As highlighted in Figure 1, ROE of all public sector banks showed a decreasing trend throughout the period of the study. After 2013, ROE declined very sharply and it reached a negative level in 2016 and 2017. This reflects the poor financial position of public sector banks.

ROA of public sector banks also continued to fall from 2007 to 2014. As shown in Figure 2, a slight increase in ROA was observed in 2015, but again it continued to decline till 2016. Over the last 10 years, ROA of public sector banks has decreased sharply.

Table 4 presents the summary statistics for ROA and ROE of public sector banks for the period of 10 years (2007-2017).

Impact of Implementation of Basel III Norms on Profitability

As the implementation of Basel III norms is a challenging task for Indian public sector banks, these stringent regulations would definitely influence the financial performance of banks. In this regard, the impact of implementation of Basel III capital norms on the profitability of banks has been measured. It is necessary to identify at what level Basel III norms are affecting the profitability of Indian public sector banks. Has there been any change in the profitability of the public sector banks due to implementation of Basel III in Indian banking sector. The 10-year period from 2007 to 2017 was categorized into two sub-periods of five years:

pre-Basel III (2007-2012) and post-Basel III (2013-2017) periods.

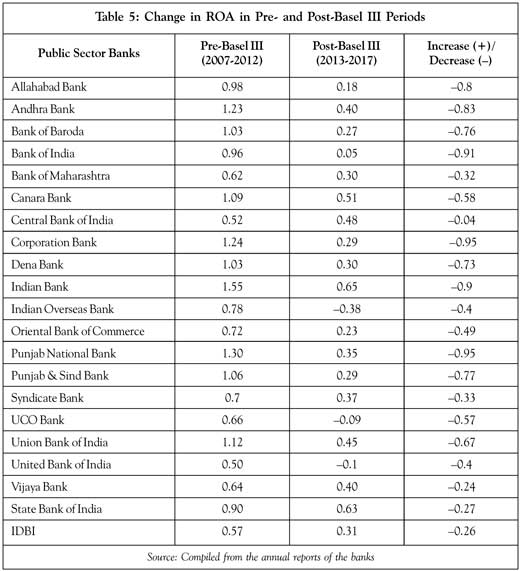

The profitability indicators are ROA and ROE which show the overall financial strength of banks. Therefore, changes in these indicators during pre-Basel III and post-Basel III reveal the positive and negative change in the profitability of banks. Table 5 presents the extent of change in profitability ratios (ROA, ROE) in pre-Basel III (2008-2012) and post-Basel III (2013-2017) periods.

It is observed that ROA of all public sector banks decreased rapidly during the period 2013-2017. All public sector banks showed negative change in ROA which reveals that the Basel III norms impacted the profitability of Indian public banks negatively because after implementation of capital regulations, progressive decline in ROA was observed.

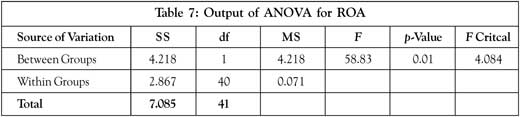

Table 6 presents the summary statistics of ROA of public sector banks over the two sub-periods of Basel III. ANOVA test was applied to examine whether there are significant differences in ROA of banks over two sub-periods of Basel III. The following null hypothesis was tested:

-

H01: There are no significant differences between the ROA of public sector banks over the two sub-periods of Basel III.

Table 7 shows that the computed F-value is more than the table value (58.83 > 4.084) which results in rejection of the null hypothesis H01 which implies that there are significant differences in ROA of public sector banks over the two sub-periods: pre-Basel III and post-Basel III.

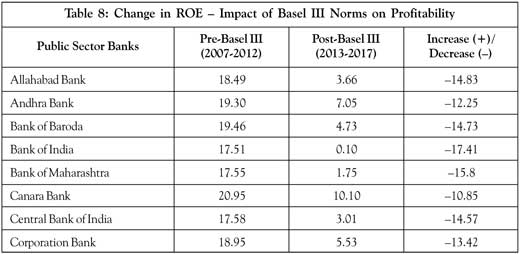

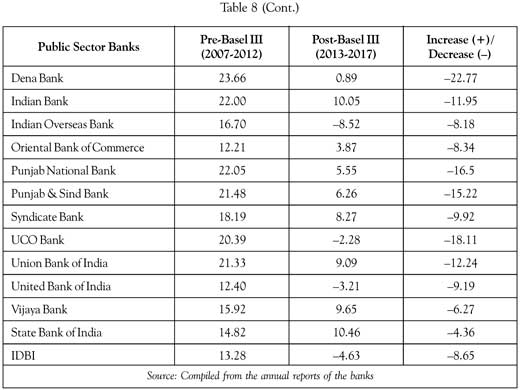

Table 8 shows that the change in ROE of all public sector banks from pre- to post-Basel III period showed negative values. Compared to the pre-Basel III period (2007-2017), ROE of public sector banks in post-Basel III period (2013-2017) declined progressively. The negative change in ROE reflects the negative impact of implementing Basel III on profitability. ROE fell sharply revealing that the Basel III norms impacted the profitability of Indian public sector banks negatively.

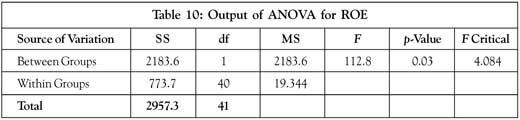

Table 9 presents the summary statistics of ROE of public sector banks over the two sub-periods of Basel III. ANOVA was applied to test the following hypothesis:

-

H02: There are no significant differences between the ROE of public sector banks over the two sub-periods of Basel III.

Table 10 shows that the computed F-value is larger than the table value (112.8 > 4.084) which results in the rejection of the null hypothesis H02 indicating that there are significant differences in ROE of public sector banks over two sub-periods: pre-Basel III and post-Basel III.

Conclusion

The present study examined the profitability of public sector banks and the impact of implementing Basel III capital norms on profitability. Based on the findings, it is concluded that Indian public sector banks are not financially stronger and stable as low ROA and ROE are recorded by all banks during post-Basel III period. Thus, negative impact of implementing Basel III capital norms on the profitability of banks is evident from progressive deterioration in ROE and ROA during the period 2013-2017. This indicates that after the implementation of Basel III capital norms, the financial performance of banks has deteriorated. This is due to increase in capital requirement which poses additional financial burden on banks as they need to hold significantly more funds to comply with Basel capital regulations which have adverse impact on the profitability. Moreover, other components of Basel III norms would necessitate the banks to change their funding preferences which can lead to higher funding cost. It is assumed that when a bank consistently records a lower than average ROA and ROE, it is considered as financially weaker because lower profitability cannot support greater future growth.

Limitations: The present study is limited to Indian public sector banks only. The financial performance of banks had shown a declining trend in terms of ROA and ROE ever since the implementation of Basel III. Therefore, we have concluded that introduction of Basel III has deteriorated the profitability of banks. Nevertheless, common sense dictates that the asset quality also had an impact on the profitability of the banks. This factor has however not been assessed. 1/15750.

References

- Adam M (2014), "Evaluating the Financial Performance of Banks Using Financial Ratios: A Case Study of Erbil Bank for Investment and Finance", European Journal of Accounting Auditing and Finance Research, Vol. 2, No. 6, pp. 162-177.

- Alper D and Anbar A (2011), "Bank Specific and Macroeconomic Determinants of Commercial Bank Profitability: Empirical Evidence from Turkey", Business and Economics Research Journal, Vol. 2, No. 2, pp. 139-152.

- Brindadevi V (2013), "A Study on Profitability Analysis of Private Sector Banks in India", IOSR Journal of Business and Management, Vol. 13, No. 4, pp. 45-50.

- Hallunovi A (2017), "Determinants of Profitability According to Groups of Banks in Albania", ILIRIA International Review, Vol. 7, No. 1, pp. 36-48.

- Hayat D S, Angraeni L and Bakhtiar T (2017), "Efficiency Analysis of Bank Branches: Production and Profitability Approaches (Case Study of Bank EFG Syariah)", International Journal of Science and Research, Vol. 6, No. 2, pp. 2078-2083.

- Islam M A (2014), "An Analysis of the Financial Performance of National Bank Limited Using Financial Ratio", Journal of Behavioural Economics, Finance, Entrepreneurship, Accounting and Transport, Vol. 2, No. 5, pp. 121-129.

- Islam Ariful and Hasan Rana Rezwanul (2017), "Determinants of Bank Profitability for the Selected Private Commercial Banks in Bangladesh: A Panel Data Analysis", Banks and Bank Systems, Vol. 12, No. 3, pp. 179-192.

- Kalhoefer C and Salem R (2008), "Profitability Analysis in the Egyptian Banking Sector", Working Paper No. 7, German University in Cairo, Egypt.

- Kumar Krishan and Kavita (2017), "An Analysis of the Financial Performance of Indian Commercial Banks", The IUP Journal of Bank Management, Vol. XVII, No. 1, pp. 1-20.

- Kumbirai M and Webb R (2010), "A Financial Ratio Analysis of Commercial Banks Performance in South Africa", African Review of Economics and Finance, Vol. 2, No. 1, pp. 30-53.

- Maiti A and Jana S K (2017), "Determinants of Profitability of Banks in India: A Panel Data Analysis", Scholars Journal of Economics, Business and Management, Vol. 4, No. 7, pp. 436-445.

- Makkar A and Hardeep (2018), "Key Factors Influencing Profitability of Indian Commercial Banks", International Journal of Academic Research and Development, Vol. 3, No. 1, pp. 373-378.

- Mehta A and Bhavani G (2017), "What Determines Banks' Profitability? Evidence from Emerging Markets: The Case of the UAE Banking Sector", Accounting and Finance Research, Vol. 6, No. 1, pp. 77-88.

- Menicucci E and Paolucci G (2016), "Factors Affecting Bank Profitability in Europe: An Empirical Investigation", African Journal of Business Management, Vol. 10, No. 17, pp. 410-420.

- Mensah Mawutor J K and Fred A (2015), "Assessment of Efficiency and Profitability of Listed Banks in Ghana", Accounting and Finance Research, Vol. 4, No. 1, pp. 164-172.

- Mohamed Zaky A H and Soliman M M (2017), "The Impact of Announcement of Basel III on the Banking System Performance: An Empirical Research on Egyptian Banking Sector", The Business and Management Review, Vol. 9, No. 2, pp. 165-175.

- Nuhiu A, Hoti A and Bekatshi M (2017), "Determinants of Commercial Banks Profitability Through Analysis of Financial Performance Indicators: Evidence from Kosovo", Business: Theory and Practice, Vol. 18, pp. 160-170, available at https://btp.press.vgtu.lt/articles.php?id=14805

- Rekik M and Kalai M (2018), "Determinants of Bank's Profitability and Efficiency: Empirical Evidence from a Sample of Banking Systems", Journal of Banking and Financial Economics, Vol. 1, No. 9, pp. 5-23.

- Roman A and Danuletiu A E (2013), "An Empirical Analysis of the Determinants of Bank Profitability in Romania", Annales Universitatis Apulensis Series Oeconomica, Vol. 15, No. 2, pp. 580-593.

- Titko J, Skvarciany V and Jureviciene D (2015), "Drivers of Bank Profitability: Case of Latvia and Lithuania", Intellectual Economics, Vol. 9, No. 2, pp. 120-129.