|

The

Elasticity and Buoyancy of the Botswana Tax System and their Determinants -

Thuto D Botlhole

Lecturer,

Department of Economics,

University of Botswana,

Gaborone, Botswana.

E-mail: botlholetd@mopipi.bw

- Tamunopriye J Agiobenebo

Professor,

Department of Economics,

University of Port Harcourt,

Choba,

Rivers State, Nigeria.

E-mail: tjagiobenebo@yahoo.com This

study extends the theoretical, methodological and empirical developments in tax

elasticity and buoyancy estimation in several ways. First, rather than assuming

that the tax base is exogenous, it considers the very strong theoretical possibility

that it may be endogenously determined by several factors such as structural shifts

in the domestic economy; developments in the external economy; trends in regional

cooperation and integration; and tax effort and evasion. Using the Botswana tax

system as a case study, it shows that these factors are important determinants

of the tax base, and hence, tax elasticity and buoyancy. Utilizing a Vector Error

Correction Model (VECM), it reveals that the Botswana tax system is income-elastic

and buoyant; trends in regional cooperation and integration are exerting negative

influence on tax revenue via its depleting impact on Southern African Customs

Union (SACU) revenue; tax evasion is revenue-depleting, and hence, dampens the

elasticity and buoyancy of the tax system; openness of the economy has significant

influence on tax revenue yield, thus, trade liberalization and globalization have

serious implications for tax system elasticity and buoyancy; and economic diversification

resulting in dynamic structural shifts have positive effects on both the tax base

and revenue yield. It emphasizes that mineral tax revenue is buoyant and elastic

with respect to mining GDP; non-mineral income tax is buoyant and elastic with

respect to exports; customs and excise duties are neither buoyant nor elastic

with respect to imports and regional integration; and also that government tax

effort is only about 27%, a degree far below its potential. These findings carry

important policy implications. Background

At

independence in 1966, Botswana was so poor that it could not even meet its recurrent

budget needs. Consequently, both its recurrent and development budgets depended

heavily on foreign aid. But, the discovery of diamonds in 1967 and exploitation

along with copper nickel beginning in the early 1970s combined with prudent use

of the mineral rents; good economic management and accountable democratic governance

changed the equation for good such that by the mid-1990s Botswana has been designated

as a middle country by the Work Bank. However, the good fortune of the country

has also meant an elimination by substitution in the sense that foreign aid has

declined over time on account of its status as a Middle Income Country (MIC).

The implication of this is that increasingly, Botswana must depend on domestic

resources and/or loans to finance the continued growth and development of its

economy and society. Debt financed development will be at an interest cost, that

means rising cost of development with the possibility of debt trap along the way.

It follows that the most viable source of development in finance is the effective

and efficient mobilization of domestic resources. Given

this reality and the dwindling level of aid as clearly expressed in Table 1, it

is compelling that the potentials and robustness of the resource mobilization

system of Botswana, in particular, the principal mechanism of the tax system,

can be mapped and appropriately measured. In 1983, development grant accounted

for over 34% of development expenditure; it has declined albeit with fluctuations

to only 2.2% in 2002, and whereas total grants accounted for about 25.5% of total

government expenditure in the same year, it has dropped to only 2.2% in 2002.

Similarly, development grant, which was 4.9% in 1981 has declined to as low as

0.5% in 2002 albeit with oscillations. The same pattern is shown by the proportion

of total grants in Gross Domestic Product (GDP), which was 5.1% in 1981 but has

fallen to just about 0.5% in 2002. Clearly, therefore, the tax system as the major

source of government revenue must be understood in terms of key properties such

as productivity, responsiveness, buoyancy and robustness to shocks and their determinants

to facilitate informed management of the system to enable it serve its purposes

effectively and efficiently.

Table

1: Historical Behavior of GDP,

Aid and Government Expenditure in Botswana,

1981-2002* | Years | GDP | DG | TG | DE

| 1981 | 780.1 | 38.2 | 39.7 | 129.3 |

1982 | 1,029.0 | 44.6 | 47.2 | 160.4 |

1983 | 1,278.9 | 48.2 | 48.2 | 140.7 |

1984 | 1,523.5 | 34.2 | 39.5 | 209.7 |

1985 | 2,144.9 | 39.7 | 41.1 | 247.5 |

1986 | 2,809.8 | 65.8 | 67.6 | 407.4 |

1987 | 3,795.6 | 104.3 | 105.9 | 558.2 |

1988 | 5,472.0 | 108.7 | 109.7 | 797.3 |

1989 | 6,130.1 | 39.3 | 40.1 | 827.7 |

1990 | 6,995.0 | 114.1 | 117.8 | 1,090.1 |

1991 | 7,810.1 | 68.7 | 69.9 | 1,098.0 |

1992 | 9,542.6 | 98.3 | 100.1 | 1,207.0 |

1993 | 11,041.4 | 185.4 | 186.6 | 1,558.3 |

1994 | 12,261.8 | 35.3 | 75.6 | 1,377.8 |

1995 | 14,203.9 | 32.0 | 37.1 | 1,672.0 |

1996 | 17,740.3 | 74.7 | 83.0 | 2,239.6 |

1997 | 20,162.6 | 110.5 | 112.1 | 2,695.5 |

1998 | 21,523.9 | 136.4 | 137.7 | 2,934.5 |

1999 | 24,943.1 | 126.0 | 126.0 | 3,451.0 |

2000 | 34,787.2 | 64.5 | 64.5 | 3,134.6 |

2001 | 35,693.4 | 139.5 | 139.5 | 8,482.0 |

2002 | 38,688.3 | 199.1 | 200.9 | 9,098.0 |

Total | - | 1907.4 | 1,989.8 | - |

Ave | - | 86.7 | 90.4 | - |

*

All absolute values are in million Pula. | Key:

GDP = gross domestic product; DG = development grant; TG = total grant; DE = development

capital) expenditure; TE = total government expenditure |

Source:

Bank of Botswana (various issues) Annual Report and Computations by Authors. |

Table

1: Historical Behavior of GDP,

Aid and Government Expenditure in Botswana,

1981-2002* |

Years |

GDP |

TE |

DG/GDP

(%) |

DG/DE

(%) |

TG/GDP

(%) |

TG/TE

(%) |

1981 |

780.1 |

168.9 |

4.9 |

29.6 |

5.1 |

23.5 |

1982 |

1,029.00 |

207.6 |

4.3 |

27.8 |

4.6 |

22.7 |

1983 |

1,278.90 |

188.9 |

3.8 |

34.2 |

3.8 |

25.5 |

1984 |

1,523.50 |

249.2 |

2.2 |

16.3 |

2.6 |

15.9 |

1985 |

2,144.90 |

288.6 |

1.9 |

16.1 |

1.9 |

14.2 |

1986 |

2,809.80 |

475.0 |

2.3 |

16.1 |

2.4 |

14.2 |

1987 |

3,795.60 |

664.1 |

2.7 |

18.7 |

2.8 |

16.0 |

1988 |

5,472.00 |

907.0 |

2.0 |

13.6 |

2.0 |

12.1 |

1989 |

6,130.10 |

867.8 |

0.6 |

4.7 |

0.7 |

4.6 |

1990 |

6,995.00 |

1,207.9 |

1.6 |

10.5 |

1.7 |

9.8 |

1991 |

7,810.10 |

1,167.9 |

0.9 |

6.3 |

0.9 |

6.0 |

1992 |

9,542.60 |

1,307.1 |

1.0 |

8.1 |

1.0 |

7.7 |

1993 |

11,041.40 |

1,744.9 |

1.7 |

11.9 |

1.7 |

10.7 |

1994 |

12,261.80 |

1,453.4 |

0.3 |

2.6 |

0.6 |

5.2 |

1995 |

14,203.90 |

1,709.1 |

0.2 |

1.9 |

0.3 |

2.2 |

1996 |

17,740.30 |

2,322.6 |

0.4 |

3.3 |

0.5 |

3.6 |

1997 |

20,162.60 |

2,807.6 |

0.5 |

4.1 |

0.6 |

4.0 |

1998 |

21,523.90 |

3,072.2 |

0.6 |

4.6 |

0.6 |

4.5 |

1999 |

24,943.10 |

3,577.0 |

0.5 |

3.7 |

0.5 |

3.5 |

2000 |

34,787.20 |

3,199.1 |

0.2 |

2.1 |

0.2 |

2.0 |

2001 |

35,693.40 |

8,621.5 |

0.4 |

1.6 |

0.4 |

1.6 |

2002 |

38,688.30 |

9,298.9 |

0.5 |

2.2 |

0.5 |

2.2 |

Total |

- |

- |

33.7 |

240 |

35.3 |

211.6 |

Ave |

- |

- |

1.5 |

10.9 |

1.6 |

9.6 |

*

All absolute values are in million Pula. |

Key:

GDP = gross domestic product; DG = development grant; TG = total grant; DE = development

capital) expenditure; TE = total government expenditure |

Source:

Bank of Botswana (various issues) Annual Report and Computations by Authors. |

Thus,

the focus of this study is twofold, namely, the estimation of the buoyancy and

elasticity of the tax system of Botswana, and decipher their determinants. The

economy of Botswana has been expanding rapidly and dynamically, as a result, significant

structural changes have taken place with serious implications both for the tax

base and yield, hence buoyancy and elasticity of the tax system. Estimating the

buoyancy and elasticity of the major components of government tax revenue as well

as for the tax system as a whole is useful for showing the extent of the sensitivity

and robustness of the tax system to the changes that take place in the composite

value of GDP (i.e., the proxy tax base). This can provide insights as to whether

or not tax revenue is being maximized relative to the tax base and the appropriate

causes of action for improvements in achievement rates. Tax

buoyancy measures the total response of tax revenue to changes in national income,

while tax elasticity is a measure of the automatic response of revenue to changes

in income, i.e., revenue increases, excluding the effects of discretionary changes

in the tax base, rate and/or structure, [cf. Lewis and Mokgethi (1983); Thac and

Lim (1984); Mtatifikolo (1990); Osoro (1993); Matundu (1995); Ariyo (1997); Masaka

(1997); Kusi (1998); Okello (2001); Mpuchane (2001); Gassama (2004); and Graeser

(2004)]. The approach of this study is to build on Singer (1968) and Osoro (1993),

and extend the theoretical foundation and empirical methodology for estimating

tax elasticity and buoyancy using Botswana time series data to estimate the elasticity

and buoyancy of the Botswana tax system and its major sources (tax categories)

for the period 1982 to 2001 using disaggregated tax bases. Conceptual/Theoretical

Framework While

agreeing with the orthodox literature that tax elasticity and buoyancy are determined

by the tax base, rate and structure, this study goes further to argue that these

determinants of tax revenue, elasticity and buoyancy are themselves determined

both by exogenous and endogenous forces such as the developments in the external

economy, trends in regional cooperation and integration, tax effort and evasion,

and structural shifts in the domestic economy, which are the ultimate determinants

of tax yield and hence elasticity and buoyancy. For example, Ariyo (1997) in studying

the productivity of the Nigerian Tax System adopted disaggregated tax bases around

notable economic events such as the pre- and post-oil boom era, as well as the

impact of Structural Adjustment Program (SAP) on the buoyancy of Nigeria's tax

system and found that these factors significantly affected government tax revenue

and hence tax buoyancy and elasticity. These findings are suggestive of the theoretical

possibility that the tax base is subject to both exogenous and endogenous influences,

which should be accounted. Tax

elasticity and buoyancy in the literature had been estimated or measured by regressing

aggregate tax-based revenue on Gross Domestic Product (GDP)a proxy for the tax

base, and incorporating a dummy variable Singer (1968) or some other proxy to

capture the exogenous influences exerted by tax legislation on the tax net, the

tax rate and/or structure. This study reckons with the insights provided by Ariyo

(1997) to model the historical realities of Botswana accounting for besides discretionary

changes in the tax net, rate and/or structure arising from legislative innovations;

other sources of both exogenous and endogenous influences on the tax base and

yield, and hence on tax elasticity and buoyancy. For example, external developments

in open economies such as Botswana affect the tax base and hence the tax yield

both directly and indirectly. In the emerging order of increasing trade liberalization

and globalization, trade-based tax revenues are likely to be affected. Specifically,

as external trade becomes freer, trade-based tax revenues are likely to dwindle,

if they are not already doing so as exemplified by the behavior of SACU revenue.

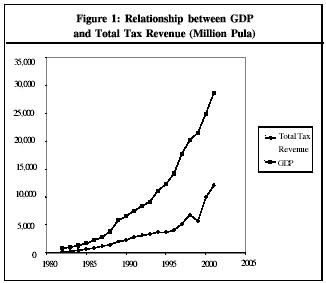

In

general, it is believed that tax revenue will move directly with the level of

economic activity in an economy. As Figure 1 shows, this belief generally holds

for the Botswana tax system. It shows the theoretically expected relationship

between GDP and total revenue except for a deep decline in 2000, which can be

explained by an exogenous shock in the relationship, which strengthens the conviction

of this study's that the factors that influence the base belong in the tax elasticity

and buoyancy functions.  For

Botswana, significant external sources of influence on the tax base and yield,

and hence the tax elasticity and buoyancy are developments in the external economy

and regional cooperation and integration arrangements such as the Southern African

Customs Union (SACU) and Southern African Development Cooperation (SADC) to which

Botswana is a member. As Southern African countries forge regional integration

(SADC), and move increasingly toward free trade, SACU revenues for each individual

country would decline and this is likely to affect tax elasticity and buoyancy.

The effect of this on tax elasticity and buoyancy can be captured by the rate

of regional integration but this is difficult to measure. It may be proxied by

a dummy variable that mirrors correctly when protocols of integration are ratified

and implemented. However, while ratifications might be discernible, observation

might not be that obvious. So in this study, the proportion of SACU revenue (SACUR)

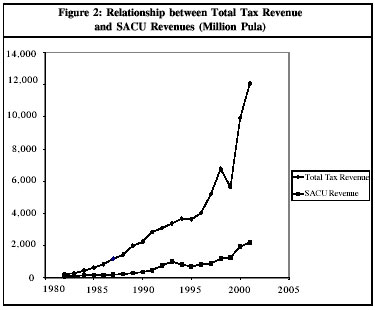

to total revenue is used as proxy.  Figure

2 shows that tax revenue and SACUR would ordinarily move together, but tax revenue

is rising faster than SACUR implying that other factors are in play. Further,

the influence of the behavior of SACUR on total revenue is visible as exemplified

by the correspondence between the dip in SACUR in the mid 1990s and the fall in

total revenue. Given this trend, the proportion of SACUR to tax revenue has been

declining. Equally,

if not more important, is the openness of the Botswana economy. In this study,

the influence of the developments in external sector on the tax base, and hence,

tax buoyancy and elasticity is captured by a measure of the openness of the Botswana

economy defined as {(X+M)/GDP}, X, M, and GDP are, respectively, exports, imports

and gross domestic product. Other

factors that have the potentials of affecting tax elasticity and buoyancy for

any given tax base, rate and structure, are tax effort and compliance. Tax effort

consists of the effectiveness of tax administration and the efficiency of tax

collection. Tax compliance is an increasing function of the willingness of taxpayers

to discharge their tax assessments or tax obligations, even though, an effective

and efficient tax administration can maximize it. Thus, for any given tax base,

rate and structure, the greater the tax effort, the greater will be the tax yield,

and hence, the larger will be the tax elasticity and buoyancy. Tax compliance

in any economy can be measured directly or indirectly by its dualtax evasion.

Since tax compliance and evasion rates are functions of the willingness of taxpayers

to pay their assessments and the capacity of the tax authorities to collect the

taxes for any given level of a tax base the willingness to pay and the ability

to collect will jointly determine the actual yield. Estimates of evasion rates

are used to capture the effects of noncompliance and/or the effectiveness of tax

administration on the tax yield, and hence, the tax elasticity and buoyancy equations.

The proportion of actual tax revenue to potential tax revenue could have been

used as proxy for tax evasion, but because of lack of data, the proportion of

tax arrears to tax revenue is used as proxy. Hence, these rates are proxied by

the ratio of tax arrears to tax revenue. Estimates of evasion rates are used to

capture the effects of noncompliance and/or the effectiveness of tax administration

on the tax yield and hence the tax elasticity and buoyancy equations. In

addition, this study also recognizes the possible influences of endogenous mechanisms

within the domestic economy as it dynamically evolves through time that manifest

in structural changes. A real economy is a living entity that responds to a wide

variety of impulses that externally manifest in structural changes, which affect

the tax base and hence tax elasticity and buoyancy. For the purposes of this study,

structural shift in the Botswana economy is proxied by the ratio of non-mineral

GDP to total GDP and is used to capture the effects of structural shifts on the

tax base, and hence, on tax elasticity and buoyancy. Other possible candidates

as proxies are the ratios of non-mineral tax revenue to mineral tax revenue; non-mineral

tax revenue to total tax revenue and non-mineral tax revenue to GDP. These, however,

mirror more of the effects of structural shifts than the causes whereas the focus

of this study is on the causes. Therefore the proportion of non-mineral GDP to

GDP is chosen over them.  All

else remaining at par, tax revenue is an increasing function of the tax base,

rate and structure, therefore, any factors that determine these will determine

tax revenue, and hence, tax elasticity and tax buoyancy. As argued earlier, for

any given tax base, rate and structure, the actual tax revenue is determined by

the input of tax effort, i.e., the effectiveness and efficiency with which tax

revenue is extracted. Tax rate and structure, however, can be changed by discretionary

policy choices and measures, and to the extent that they are changed they will

affect tax revenue for any given base; and hence, tax elasticity and buoyancy.

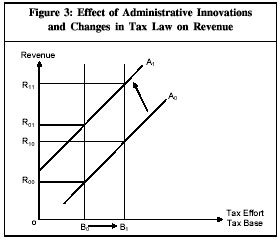

During the period under study, there have been considerable changes in tax legislation

coupled with different administrative innovations aimed at achieving increasing

effectiveness and efficiency in tax administration. Figure 3 illustrates how these

innovations will affect the revenue yield. In

Figure 3, tax effort and base are measured on the horizontal axis while tax revenue

is measured on the vertical axis, where B0 and A0 represent

the initial tax base and effort, respectively that combine to yield R00

in revenue. Given this initial tax base, innovations in tax legislation that improve

the tax net, rate and structure and/or the effectiveness and efficiency of tax

administration shifts the tax effort curve up to A1 and tax revenue

increases to R01. Similarly, given the initial level of tax effort,

an increase in the tax base to B1 increases tax revenue but only to

R10. Thus, Figure 3 seems to suggest that improvements in tax effort

might even be more important in mining more revenue out of the same base than

growth in the base without improvements in tax effort, which is intuitive, plausible

and sensible, since irrespective of the size of the tax base, zero tax effort

would yield zero revenue. Of course, improvements in tax effort and growth in

the tax base provide the best of the worlds for growth in tax revenue as these

improvements are self-reinforcing such that revenue increases to R11.

The

theory in sum, therefore, is that the buoyancy and elasticity of the Botswana

tax system are explained by the level of economic activity proxied by GDP, openness

of the Botswana economy, trends in regional cooperation and integration, tax effort

and evasion, and structural shifts in the domestic economy as well as innovations

in tax legislation and/or policy variables that affect the tax base, rate and/or

structure. Model

Specification Based

on the above theory, the relationships between tax elasticity and buoyancy and

their determinants are defined, respectively as Where

TR= Tax Revenue; Y = GDP proxy for the level of economic activity; X1 = (X+M)/GDP

proxy for openness variable; X2 = (TA/TR) proxy for tax effort and evasion; X3

= (SACUR/TR) proxy for regional cooperation and integration; X4 = (NMGDP/GDP)

proxy for structural shifts in the economy; Di are dummy variables taking the

value of 1 for each year in which there is a discretionary change in tax policy

during the period 1982-2001, and a value of zero (0) otherwise, ai and bj are

the slope coefficients. In the case of the dummy variables, the summation takes

account of the possibility of multiple tax changes during a specified period.

u is a random error term. X = Exports; M = Imports; TA

= Tax Arrears – proxy for tax effort and evasion; SACUR = SACU Revenue –

proxy for regional cooperation and integration; and NMGDP = Non-mineral GDP.Equation

(2) is the model for estimating the elasticity of a tax system, since it is necessary

to isolate the effect of discretionary changes in tax policy on tax revenue. For

this Singer’s (1968) Dummy Variable Technique (DVT) is adopted. It introduces

a dummy variable into the model to account for the effect of each discretionary

change in the tax rate, bases and structures during the period of study. Thus,

equation (1) is an extension of Osoro (1993) while equation (2) is extension of

Osoro (1993) and Singer (1968) combined. Empirical

Analysis Secondary

data in quarterly time series for the period 1982 to 2001 were obtained from the

Department of Taxes, several issues of the Annual Reports of the Bank of Botswana

(BoB), various issues of Statistical Bulletins published by the Central Statistics

Office (CSO),National Development Plans and Budget speeches published by the Ministry

of Finance and Development Planning (MFDP) for estimating the models. The

data were subjected to diagnostic tests using the general Augmented Dickey-Fuller

tests (ADF), which showed that all the variables in level form at the logarithmic

scale were non-stationary, and also that X1 (proxy for openness) and X3 (proxy

for regional cooperation and integration) were integrated of order two I (2),

while the rest of the variables were integrated of order one, I (1). As a corrective

mechanism, first and second differences were applied. To test for Cointegration,

the Johansen Cointegration Procedure was adopted in order to get insight as the

existence long-run equilibrium relationship between the variables in both the

aggregate and tax categories models. This is accomplished by the specification

of vector error correction models, which allow for a wide range of short dynamics

while the long-run behaviors of the endogenous variables converge to their cointegrating

relationships.These transformations in the data and the error correction modelling

means that equations (1a) and (2a) are modified accordingly for purposes of measuring

the relationships.

Results

of Empirical TestsThe

Aggregate Model

Table

2 reports on the results of estimating the aggregate model of the Botswana tax

system adopted by this study and compares the results with those of estimating

the orthodox model exemplified by Osoro (1993).

Table

2: Estimation Results of the Model Used in this Study |

Thuto-Agiobenebo

Model | Variables | Coefficients | Sum

of Coefficients | t-Statistics | Prob |

C | 0.006739 | 0.006739 | 1.177962 | 0.2433 |

DLTR_1 | 0.690228 | 0.690228 | 8.825414* | 0.000 |

DLY | 1.582698 | - | 3.987343* | 0.0002 |

DLY_1 | 1.423773 | 3.006471 | -3.513350* | 0.0008 |

DLX1 | -0.38916 | - | -4.329683* | 0.0001 |

DLX1_1 | 0.189957 | -0.1992 | 1.851131*** | 0.0689 |

DLX2 | -0.31202 | - | -10.40310* | 0.000 |

DLX2_1 | 0.223442 | -0.08858 | 6.002063* | 0.000 |

DLX3 | -0.36553 | - | -4.379309* | 0.000 |

DLX3_1 | 0.225916 | -0.14021 | 2.520860** | 0.0143 |

DLX4 | 1.053781 | - | 2.129197** | 0.0372 |

DLX4_1 | -0.93901 | 0.114775 | -2.003098** | 0.0495 |

ECT_1 | -0.1131 | -0.1131 | -3.909857* | 0.0002 |

Notes:

The asterisks *, ** and *** denote significance at the 1, 5 and 10% levels |

Sample

period: 1982 to 2001 (Quarterly 80 sample observations) |

Adjusted R2

= 0.9058 | DW=2.0457 |

Diagnostic

tests | Normality

Test: 11.47551 (0.00322) | Breusch-Godfrey

Serial Correlation LM Test: 0.137486 (0.871820) | ARCH

Test: 0.301974 (0.584348) | Ramsey

RESET Test: 1.179350 (0.281761) |

Table

2: Estimation Results of the Model Used in this Study |

| Osoro's

Model | Variables | Co-efficients | t-Statistics | Prob |

C | 0.004803 | 0.482415 | 0.631 |

DLTR_1 | - | - | - |

DLY | 1.00238 | 5.17726*** | 0.000 |

DLY_1 | - | - | - |

DLX1 | - | - | - |

DLX1_1 | - | - | - |

DLX2 | - | - | - |

DLX2_1 | - | - | - |

DLX3 | - | - | - |

DLX3_1 | - | - | - |

DLX4 | - | - | - |

DLX4_1 | - | - | - |

ECT_1 | -0.01293 | -0.20118 | 0.8411 |

Sample

period: 1982 to 2001 | Adjusted

R2 = 0.254257 | DW=0.656713 |

Diagnostic

tests | Normality

JB = 9.004868 [0.0011082] | Breusch-Godfrey

Serial Correlation LM Test: 31.99543 (0.000000) | ARCH

Test: 119.9762 (0.000000) | Ramsey

RESET Test: 21.46693 (0.000016) | ***significance

at 1% level | The

adjusted R2 for the model adopted in this study is 0.9058, implying that about

91% of the variation in tax revenue is explained by the model. The F-statistics

strongly rejects the null hypothesis that the regression coefficients are jointly

equal to zero. This means that all the explanatory variables in the model are

important determinants of tax revenue in Botswana. The Durban Watson (DW) statistic

of 2.0457 indicates that the regression model does not suffer from problems of

autocorrelation. In addition, the results of the Ramsey Reset test show that the

model is correctly specified and the Normality test indicates that errors are

normally distributed.

The

coefficient of the error correction term gives the speed of adjustment of each

variable towards its long run equilibrium value, while the sign of the coefficient

gives the direction of adjustment towards equilibrium. The fact that the sign

of the coefficient is negative implies the variables convergence towards their

long run equilibrium values and relationships. Results from the model used in

this study show that the coefficient is -0.113098 (see Table 2), which is significant

at the 1% or higher level but implies a rather low speed of adjustment; since

only 11% of the previous errors in the tax revenue are corrected for in the current

period. The

results reported in Table 2 show that not only all the variables in the model

have the theoretically expected signs but are also have significant at 10% or

higher levels. The openness, regional cooperation and integration, tax effort

and evasion, and level of economic activity variables are all significant at 5%

level of significance, while the structural shift variable is significant at the

1% or higher level. The lagged value of the dependent variable, TR, incorporates

the delayed and persistent effects of the independent variables on the dependent

variable and is therefore included to capture the policy lags in the variables.

The coefficient of this variable is positive and highly significant at the 1%

or higher level. Thus, all the variables are significant determinants of total

tax revenue, and hence, tax elasticity and buoyancy in Botswana. The

sign of the openness variable deserves some elaboration. The sum of the coefficients

of the current and lagged values of this variable is negative. This means that

on average the openness of the Botswana economy is tax revenue depleting and will

adversely affect both tax elasticity and buoyancy. Theoretically speaking, the

sign of this variable is indeterminate. Exports are expected to have positive

effects on the level of economic activity and hence on the tax base, but imports

can go either direction depending on the prevailing tax policies and regimes.

Further, the Botswana economy is heavily dependent on imports and more so for

consumption of goods, which represent serious leakages out of the system that

constrict the tax base. In addition, the evidence, may in part capturing the indirect

adverse effects of increasing regional cooperation and integration on SACU revenue

and its higher implications for tax revenue in Botswana. In sum, the results show

that the negative effects of imports on the base, and hence, tax revenue outweigh

the positive effects of exports. Indeed,

the results of the model adopted in this study are rich in insights. For example,

the effects of the institutional mechanism governing the administration and disbursement

of SACU revenue to member countries are discernible. Since revenue disbursements

are not contemporaneous, the withholding of current SACU revenue collections is

tax revenue depleting for member countries including Botswana, which is offset

when the revenue is finally received. Thus, the coefficients of X3 in the current

period is negative while that of the lagged valued is positive. On average, however,

there is a negative relationship between the proportion of SACU revenue to GDP

and total tax revenue over the period of study implying that the negative effects

outweigh beneficial effects of SACU. This is in consistent with the expected outcome

(hypothesis) that as Southern African countries forge regional integration and

move increasingly toward freer trade, SACU revenues for each individual country

would decline and thus lead to a decline in total tax revenue. In addition, the

economy of Botswana is open and is therefore responsive to trade liberalization

and globalization trends. These reduce imports and exports duties as sources of

government revenue, thus, for the same tax base, with increasing openness, less

tax revenue will be realized as shown by the overall negative coefficient (-0.1992)

of X1. This result is different from the one from a study by Mpuchane (2001),

which reported that the openness of the Botswana economy is insignificant and

does not have any impact on the performance of the tax system of Botswana. Similarly,

while tax evasion is revenue depleting, efforts to collect tax in arrears partially

offsets its effects on tax revenue. Thus, the coefficient of the current value

of tax evasion is negative; the coefficient of its lagged value is positive. But

again, the collection of tax arrears notwithstanding, tax evasion is revenue depleting

as the sum of the coefficients is negative. It follows that tax administration

and follow up problems affect tax yield, and hence elasticity and buoyancy negatively.

It is also evident from the results that while structural shifts (innovations)

impact positively on tax revenue, and hence, tax elasticity and buoyancy, structural

rigidities have adverse effects given that the coefficient of the current value

of the structural shift variable X4 is positive and that of the lagged value is

negative. Happily, the positive effects outweigh the negative effects since the

sum of the coefficients is positive. Returning

to the comparison with the results of Osoro (1993), it is self-evident that the

orthodox model is inferior and seriously miss-specified. The model clearly violates

the important assumptions of the classical linear model that there is no autocorrelation

among the disturbance terms ui, and that the regression model is correctly specified.

Hence this study extends the theoretical, methodological and empirical developments

in the estimation of tax elasticity and buoyancy. Tax

Buoyancy and Elasticity Table

3 reports on the results of estimating the buoyancy of the Botswana tax system

by aggregate and categories. The buoyancy coefficient of the total tax system

is 1.982, which is significance at the 5% level indicating a responsive tax system.

The regression results indicate that GDP, tax effort and evasion explain about

94% of variations in tax revenue.

Table

3: Tax Buoyancy by Aggregate and Categories | Categories | Buoyancy

Coefficient | t-statistic | R2 | DW-Statistic |

Total

Tax Revenue | 1.982 | 7.795 | 0.948 | 1.91 |

Mineral

Revenue | 2.274 | 9.534 | 0.682 | 1.69 |

Customs

and Excise Duties | 0.74 | 2.099 | 0.558 | 1.43 |

Non-Mineral

Income Tax | 1.504 | 4.443 | 0.676 | 1.77 |

Mineral

revenue is buoyant with a coefficient of 2.274, which is significant at the 1%

level, showing that it is an important determinant of tax revenue in Botswana.

About 68% of the behavior of mineral revenue is explained by mining GDP and the

openness of the economy. The buoyancy coefficient of customs and excise duties

is below unity (0.740) implies that customs and excise duties are not buoyant.

This can be attributed to the influence of regional integration, whereby movement

toward freer trade, causes a decline in SACU revenues for Botswana. Also, the

industrial base of the Botswana economy is very narrow and its contribution to

GDP is even on the decline. The t-statistic (2.099) is lower than the critical

value, this leads us to the decision to accept the null hypothesis and conclude

that customs and excise duties are not buoyant. A

buoyancy coefficient of 1.504 means that non-mineral income taxes are buoyant

as expected and is significant at the 10% level. The R2 shows that 68% of the

variation in non-mineral income tax is explained by exports, imports, manufacturing

output and structural shifts in the economy. Table

4 reports on the results of estimating the elasticity of the Botswana tax system

by aggregate and categories. A measurement of the tax elasticity requires that

data on tax revenues be adjusted to eliminate the effects of discretionary tax

measures. Over the study period however, no changes in tax legislation known to

these s took place for mineral revenue and customs and excise duties. As

a result, their elasticity coefficients are assumed to be the same with the values

of their buoyancy coefficients. Thus, from Table 3, the customs and excise duties

are inelastic with a coefficient below unity (0.740), while mineral revenue is

highly elastic with a coefficient above unity (2.274).

Table

4: Tax Elasticity by Aggregate and Categories | Categories | Buoyancy

Coefficient | t-statistic | R2 | DW-Statistic |

Total

tax Revenue | 1.56 | 8.17 | 0.973 | 1.91 |

Mineral

revenue | 1.385 | 4.96 | 0.692 | 1.83 |

With

an elasticity coefficient of about 1.56, which is significant at the 1% level,

the Botswana tax system is income elastic. An R2 of 0.973 indicates that the tax

base adequately explains variation in the tax revenue. The

elasticity coefficient of Non-mineral income tax is 1.385, which is significant

at the 5% level, indicating that it is elastic. The R2 indicates that the tax

base explained about 69% of the variation in non-mineral income tax. As

shown in Tables 3 and 4, the tax system as a whole had a buoyancy of 1.982, which

is higher compared with an elasticity of 1.56. This difference indicates that

discretionary changes improved the revenue performance of the tax system. Performance

of the tax system depends not only on the amount collected, but also on several

other factors, such as: tax effort, effectiveness and efficiency of tax administration,

tax evasion and avoidance, compliance burden, transparency and accountability,

efficiency and allocation effects of taxes in the economy. Others include lack

of taxpayer education, cultural variables, operational inadequacies of the tax

administration in Botswana, inadequacies and loopholes in the law among others.

These additional variables that are not part of the formal modelling are identified

by key informants who responded to a structured questionnaire that solicited the

perceptions of key stakeholders on the performance of the Botswana tax system. Tax

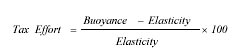

effort by the Botswana Government Government

Tax Effort is Defined as:

That

is, it computed as the percentage difference between the size of buoyancy and

elasticity coefficient relative to the elasticity coefficient of the total tax

system. This computation is intended to test whether or not the Government of

Botswana has exerted enough effort to realize its tax potential. The computation

of the tax effort shows a government tax effort is only 27%, which is far below

its potential. Thac and Lim (1984) obtained a tax effort coefficient of 40% for

Papua New Guinea. Summary

and Conclusion This

study estimated the elasticity and buoyancy of the Botswana tax system along with

those of its major sources or tax categories for the period 1982 to 2001 using

quarterly data, and also tested some key novel propositions that tax elasticities

and buoyancies are affected by developments in the international economy proxied

by the degree of openness variable, trends in regional cooperation and integration

proxied by the proportion of SACU revenue in total revenue of Botswana which is

affected by the development of SADC and structural shifts as the economy of Botswana

evolves dynamically through time proxied by non-mining GDP to GDP. The study used

a Vector Error Correction Model (VECM) to estimate the relationship. The innovations

introduced into the tax elasticity and buoyancy estimation theory and methodology

add to the richness of the results available to address the composite question

of how elastic and buoyant is the Botswana tax system and the individual taxes

and what their determinants are. The econometric results obtained in this study

show that for the open economy, developments in the international economy, trends

in regional cooperation and integration and structural shifts are significant

determinants of the tax bases and hence tax elasticities and their buoyancies.

Further, for any given tax base, tax evasion depletes the tax yield (receipts),

and hence, tax elasticities and their buoyancies. Policy

Implications Although

the results from this study showed that the overall tax system for the period

1982-2001 is buoyant and elastic, buoyancy coefficients and elasticity indexes

for the tax sources relative to their respective tax bases are not sufficiently

high. Government should therefore undertake more discretionary measures in order

to improve the revenue performance of the Botswana tax system, and more importantly,

step up efforts to diversify the economy. The evidence is strong that Botswana

can extract significantly more revenue from its tax base if only it can step up

tax effort and minimize tax evasion and avoidance. Although

the revenues from SACU account for a significant amount of government revenue,

they have been declining over the years due to increasing free trade amongmember

countries, the Government of Botswana therefore faces the challenge of diversifying

its revenue sources by identifying new and viable sources of revenue to sustain

its development efforts. In this regard, government introduced Value Added Tax

(VAT) in 2002, which is still at experimental stages. The Government therefore

has to move quickly to improve the general understanding of VAT and how it can

best be operated in the VATED companies, as well as increase the transparency

of the system and the accountability of the operators. To achieve these, government

must move to minimize the compliance burden of the operators, in particular, small

and medium sized operators. High compliance costs and a complicated tax system

could cause disincentives among tax payers and lead to evasion, therefore, the

compliance burden for taxpayers, particularly self employed individuals and small

businesses should be investigated, mapped, measured and minimized. Also, initiatives

should be taken to make the tax system as less complicated as possible. In addition,

there is a vast potential to expand the VAT net and government should explore

and exploit this vigorously. In

order to reduce the cost of tax administration, reforms aimed at improving the

effectiveness and efficiency of tax assessment and the collection of outstanding

taxes need to be undertaken. The cost of tax administration in Botswana is too

high, the acceptable norm is said to be between 1 to 2%, in Botswana it is 42%. Limitations

of the Study and Recommendations for Further Study Botswana

like most developing countries is faced with the problem of lack of well-documented,

up-to-date database. As a result, data for some variables could not be attained.

The data generated is from 1982-2001, due to inconsistencies; data for more recent

years was not used and this has affected the currentness of the study. For example,

the proportion of actual tax revenue to potential tax revenue could have been

used as proxy for tax evasion, but because of lack of data, the proportion of

tax arrears to tax revenue was used as proxy. So, as more and better data become

available, the model can be tested again. The

model used in this study did not capture the effects of very important macroeconomic

policies that affect tax revenue. According to Tanzi (1991), there are three main

macroeconomic policies that may affect tax revenue negatively are; overvaluation

of the national currency, import substitution and trade restrictions. However,

import substitution and trade restrictions cause elimination by substitution,

so it cannot be taken for granted that they necessarily reduce tax revenues. The

actual outcome depends on the relative tax yield of protected domestic activities

and trade duties. After all, the former will yield triple sources of tax revenue,

namely; income tax, company tax and excise duties. Therefore, for further research,

these macroeconomic policies can be incorporated into the elasticity and buoyancy

equations to analyze their effect on the performance of the Botswana tax system.

Although

this study estimated tax effort by the Botswana government, a detailed investigation

of policies that make the tax system ineffective and inefficient (and vice versa)

should be carried out to decipher their implications. Furthermore, further research

on how controls for both changes in tax rates and rules affect government’s

efforts to maximize tax revenue should be undertaken. Another

possible area for future research is the effect of the introduction of broad-based

Value Added Tax (VAT) to replace sales tax in 2002, on total tax revenue, and

consequently tax elasticity and buoyancy.In 2002, SACU reviewed and changed exogenously

the revenue sharing formula among its members, the effects of this on SACU revenue

could not be accounted for by this study because of the use of quarterly data

which cut the period of study to 2001, which automatically excluded the period

of the revenue formula innovation from the period of this study. So, future studies

on the buoyancy and elasticity of the Botswana tax system should try to account

for the possible effects of the change in revenue formula, since it exemplifies

policy innovation or exogenous change in tax legislation and/or administration. References 1.

Ariyo A (1997), “Productivity of the Nigerian Tax System”, Africa Economic

Research Consortium, Research Paper, No. 67. 2.

Bank of Botswana (Various Issues), Annual Reports, Gaborone, Botswana. 3.

Budget Speeches (Various Issues), Ministry of Finance and Development Planning,

Gaborone, Botswana. 4.

Central Statistics Office (Various Issues), Statistical Bulletins, Gaborone, Botswana. 5.

Department of Taxes (1982-2002), Commissioner’s Reports, Gaborone, Botswana.

6.Gassama H N (2004), Elasticity and Buoyancy of the Tax System in Liberia, Unpublished

MA Dissertation Submitted to the University of Botswana, Gaborone. 7.

Greaser (2004), “Determination of Elasticities of Revenue Growth to Changes

in GDP", US treasury, Office of Technical Assistance. 8.

Kusi K N (1998), “Tax Reform and Revenue Productivity in Ghana”, African

Economic Research Consortium, Research Paper No. 74. 9.

Lewis S R and Mokgethi D N (1983); Botswana’s Economy Since Independence,

(Tata McGraw-Hill Publishing Company Limited, New Delhi) 10.

Masaka G N (1997), The Determinants of Tax Revenue in Botswana, Unpublished BA

Dissertation Submitted to the University of Botswana, Gaborone. 11.

Matundu 0 (1995), Evaluation of the revenue performance of the Namibian Tax System,

(unpublished MA Dissertation submitted to the University of Botswana, Gaborone) 12.

Mpuchane (2001), The Elasticity of the Tax System of Botswana, Unpublished BA

Dissertation Submitted to the University of Botswana, Gaborone. 13.

Mtatifikolo F P (1990), “An Economic Analysis of Tanzania’s Tax Performance

Experiences Since the 1973 Tax Act”, Eastern Africa Economic Review. 14.

National Development Plans (Various Issues), Ministry of Finance and Development

Planning, Gaborone, Botswana. 15.

Okello A K (2001), “An Analysis of Excise Taxation in Kenya”, An African

Economic Policy, Paper No. 73. 16.

Osoro (1993), “Revenue Productivity of the Tax System in Tanzania”,

Journal of African Economics, No.3. 17.

Singer N M (1968), “The Use of Dummy Variables in Establishing the Income

Elasticity of State Income Tax Revenues”, National Tax Journal, Vol. 21,

June, pp. 200-04. 18.

Tanzi V (1991), “Public Finance in Developing Countries”, Edward Elgar

Publishing Limited, United Kingdom. 19.

Thac D C and Lim D (1984), “Papua New Guinea’s Tax Performance, 1965-1997”,

World Development, Vol. 12, No. 4, pp. 451-459. Reference

# 42J-2006-12-03-01. |